By Shira Gonen

A strong earnings report from Ambarella Inc AMBA was overshadowed by weak guidance, causing one analyst to remain on the sidelines until the company provides more updates on a turnaround plan. On the other hand, last week's investor meeting with LinkedIn Corp LNKD caused another analyst to believe the stock will recover, pointing to strong sales, expected growth initiatives, and a valuable market opportunity.

Ambarella Inc

Analyst Marc Estigarribia of Chardan Capital weighed in on Ambarella following the company's Q4:16 earnings last week. The company posted higher then consensus revenues of $67.97 million and lower than consensus earnings per share of $0.64, 4 cents lower than estimates, marking the first decline in 18 quarters. The company also issued weak guidance of $55 to $57 million in sales, down 21% from the midpoint of the same quarter of last year, projecting low exposure to GoPro, its biggest customer, until they release new products. Similarly, the company expects sales for wearables to comprise of only ~15% of total revenue for next quarter. With demand low for GoPro, Ambarella CEO stated the company would issue weak guidance until they had more accurate demand levels for wearable sports cameras.

Related to guidance, the analyst believes management will most likely have to decrease its FY2017 guidance due to a lack of "any material catalyst until at least 3Q17." He cites slow growth and a decrease in margins "without any clear vision for a positive reverse trend reset." Although the analyst notes that strong sales growth and FCF makes the company a "proven video chip technology is well-positioned to capture niche-market leadership in video compression and low power consumption," he remains on the sidelines until the company "executes on its future growth plan-run rate," in the second half of 2017.

The analyst states lack of turnaround information from its main customer GoPro, who has a large inventory expected to last at least until April. He also notes a "softer than expected update" on GoPro products which give customers the option to not have to purchase new chips or cameras. According to the analyst, Ambarella's drone segment will experience the most short-term success, with long term success for its Auto (OEM) segment.

The analyst maintains his Hold rating and lowers his price target to $50 due to "near term uncertainty."

According to TipRanks' statistics, out of the 11 analysts who have rated the company in the last 3 months, 5 gave a Buy rating while 6 remain on the sidelines.

LinkedIn Corp

Analyst Youseff Squali of Cantor Fitzgerald weighed in on LinkedIn following an investor meeting, citing a few reasons for his bullishness despite weak guidance from its earnings call earlier last month. Here's why the analyst is bullish on the stock.

- "Talent Solutions' field sales are healthy." – Squali states that in Q4:15, field sales comprised around 75% of the company's Talent Solutions (recruiting tool) revenue, while management guided ~25% revenue growth for FY:16. The guidance reflects ~20% customer growth and slight pricing growth. The analyst notes that although the company will omit Corporate Solutions customers from reports, the company has sustained growth in ARPU and users.

- "Recruiter offering for SMBs expected in 2017." – "The analyst notes growth deceleration from online sales due to contract changes affecting visibility, pricing leverage, and difficult subscriber comparisons. In order to get the company back on track, management plans to release a new SKU to target small business recruiters, which represent a significant revenue opportunity, as the company's current Talent Solutions products only cater to large corporate recruiters and individuals. The company will price the product between $1k and 9k per month with an expected release in 2017."

- "The total opportunity remains unchanged." – The analyst is bullish on the company's products, markets and opportunities despite weak guidance including a 900bps reduction in 2016 revenues and expected decline in EBITDA growth. The analyst highlights the company's 780 million international knowledge worker base and total market demand of $27 billion for its Talent Solutions segment. He also points to favorable trends in North America though predicts that the EMEA and APAC regions will suffer from negative FX and oil trends. However, he believes the recent pullback in shares represents a compelling entry point.

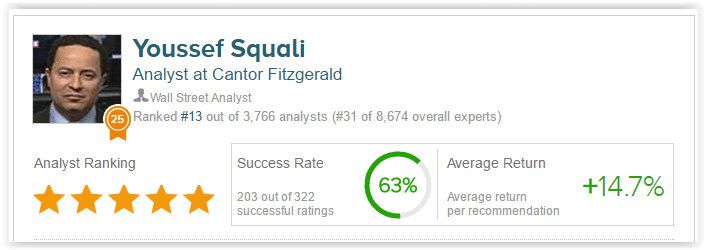

The analyst maintained a Buy rating and $210 price target on the stock. Youssef Squali is ranked #132 out of 3,766 analysts on TipRanks. He has a 63% success rate recommending stocks with an average return of 14.7% per rating.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.