Invest in high yield bonds today with Interactive Brokers as your trusted brokerage.

An often-cited maxim in investing is "higher risk = higher returns." Most risks are compensated. For example, investing in small-cap stocks can sometimes reward investors with greater long-term returns in exchange for enduring higher volatility.

This maxim is especially true when it comes to high-yield bonds, which are some of the riskiest fixed-income securities available to investors. Despite their lower credit ratings, high-yield bonds can offer enticingly strong yields that dwarf those from Treasury bonds, municipal bonds, regular corporate bonds or even real estate investment trusts (REITs).

This guide will explain everything there is to know about investing in high-yield bonds, how they work and why incorporating them into your portfolio could potentially make your investment strategy more effective.

How Do High-Yield Bonds Work?

Most companies issue fixed-income securities called corporate bonds to fund capital projects. By selling bonds, companies can raise capital without diluting shareholders by selling equity. By selling a corporate bond, the company is essentially taking loans from investors in return for paying a fixed semi-annual coupon and the principal at maturity.

High-yield (also known as "junk bond") bonds are a special type of corporate bond with lower than investment-grade credit ratings. This designation usually refers to a rating of below BBB or Baa by Standard & Poors and Moody's, respectively. A rating of BBB or Baa is considered the minimum required for a corporate bond to qualify as investment grade.

Bonds that fall below BBB or Baa are below investment grade and have a higher risk of default. There is a very real chance that the issuer of these bonds may be late or default on interest or principal payments. To compensate for that increased risk, these bonds must pay higher coupon rates to entice investors.

Companies with poor creditworthiness or a limited, unproven history of operations may only be able to issue bonds at a high coupon rate to attract investors. Otherwise, investors wouldn’t be willing to take on the risk of a bond with poor credit ratings or backed by new, untested companies with shaky financials.

Some high-yield bonds are called "fallen angels" and are the result of previously investment-grade bonds being downgraded. This situation often occurs when the issuer suffers a financial crisis or scandal that causes its credit rating to suffer. For example, a company with investment-grade corporate bonds that is convicted of fraud might see those bonds downgraded to junk status.

Advantages of High-Yield Bonds

Despite their risks, high-yield bonds have a number of advantages that can make them good portfolio holdings for some investors. These include:

Higher Yields

High-yield bonds must pay a greater coupon rate to compensate investors for the increased credit risk they pose. Their yields tend to be much higher compared to investment-grade corporate bonds or U.S. government Treasuries of similar maturity. These yields can be beneficial to investors looking for increased income potential.

Historically Strong Long-Term Returns

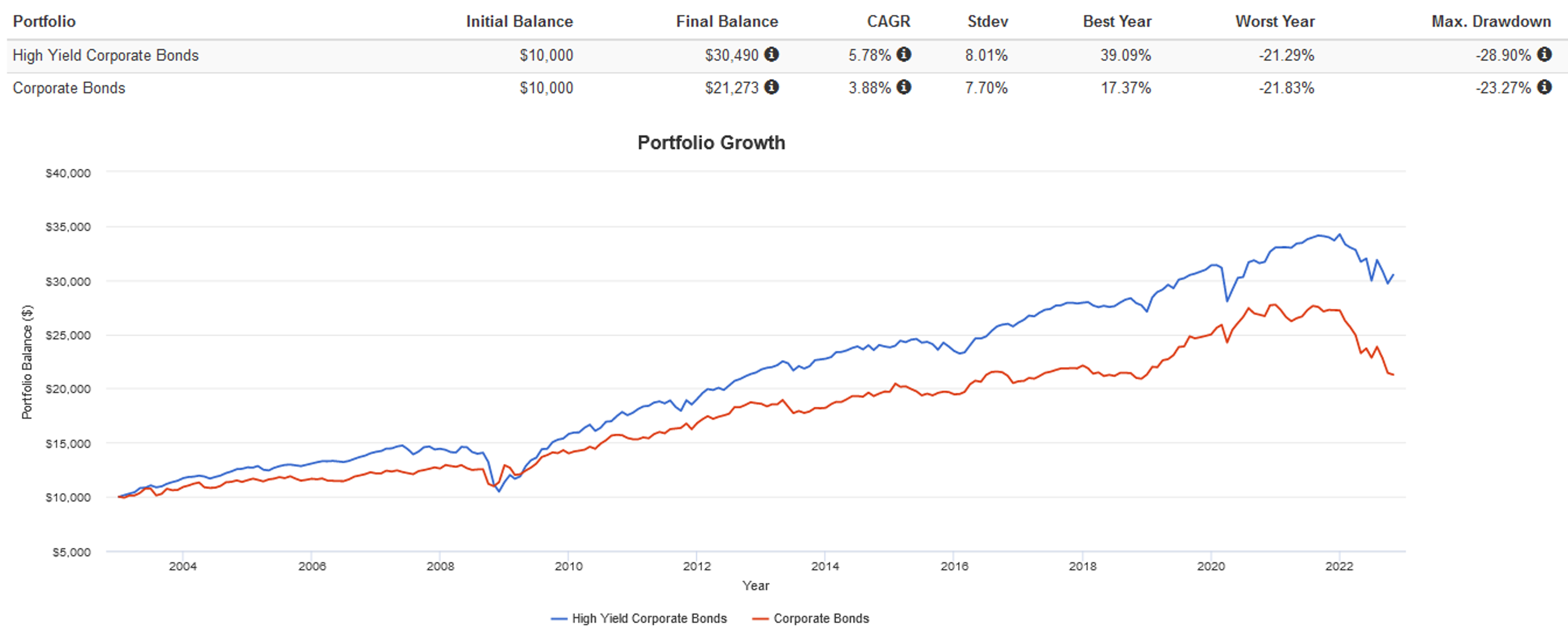

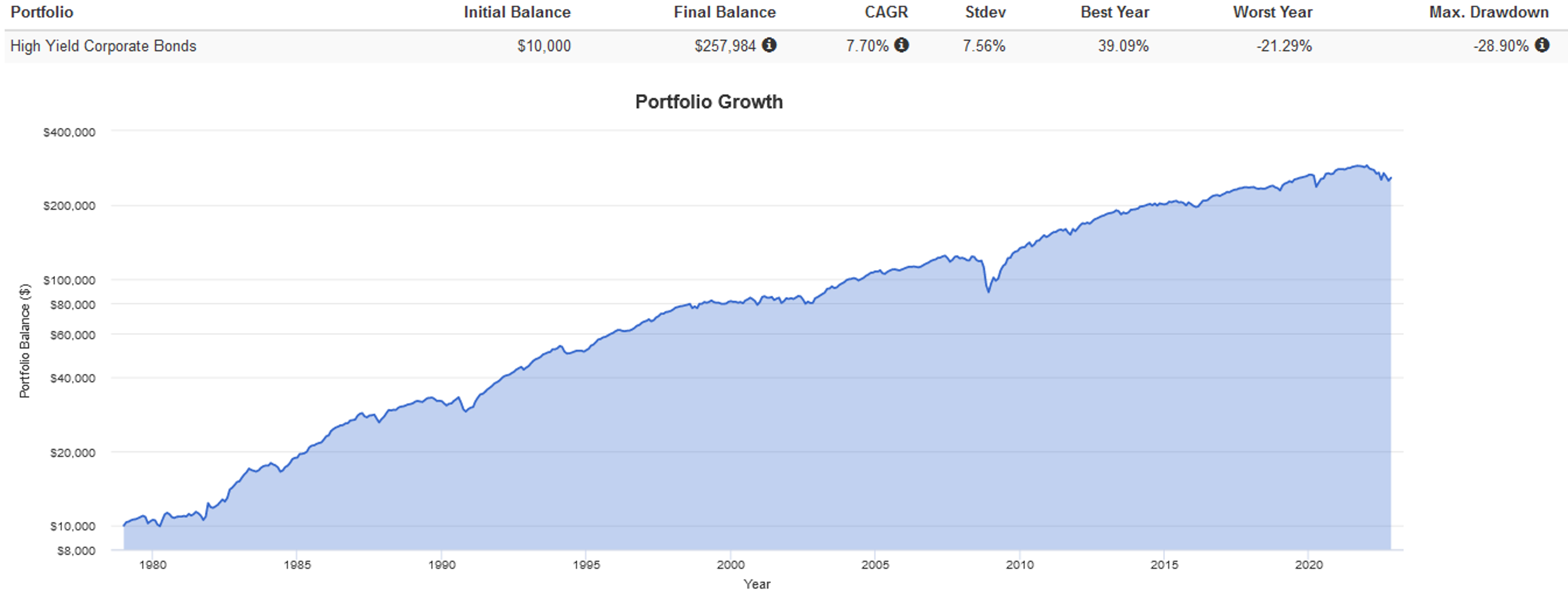

From 2003 to the present, with all coupons reinvested, high-yield bonds as an asset class outperformed corporate bonds as an asset class. High-yield bonds also outperformed in terms of various one to 15-year rolling periods. From 1979 to the present, high-yield bonds returned an annualized 7.70%, which was the highest out of all fixed-income assets and came close to the returns offered by global equities.

Source: Portfolio Visualizer

Source: Portfolio Visualizer

Source: Portfolio Visualizer

Portfolio Diversification

High-yield bonds possess positive expected returns, decent volatility and a lower correlation with stocks, which makes them a potential candidate to diversify a portfolio. From 1979 to the present, high-yield bonds as an asset class posted a 0.62 monthly correlation with the total U.S. stock market, which can provide diversification benefits. High-yield bonds can also move independently of other bonds like U.S. Treasuries, so adding them to a fixed-income allocation can also improve risk and return.

Source: Portfolio Visualizer

Lower Interest Rate Risk

One way to increase yields with bonds is to hold longer-maturity bonds. However, the longer the maturity of a bond, the more sensitive it is to changes in interest rates. Because bond prices are inversely related to interest rates, rising rates can severely hurt long-term bonds. In contrast, high-yield bonds can deliver greater yields without having to increase maturities. All else being equal, a high-yield bond with a maturity of 10 years can have a yield higher than a Treasury bond with a maturity of 30 years.

Risks Involved with High-Yield Bonds

Despite their advantages, high-yield bonds pose a number of risks that might not make them suitable holdings for all investors. Some risks involved with high-yield bonds include:

Low Credit Rating

The issuers of high-yield bonds typically face concerns around their cashflows, leverage or balance sheets. When markets and economies become stressed, they can default on their bonds, with high-yield ones often incurring the first losses. The low credit rating reflects this increased probability of default.

Market Risk

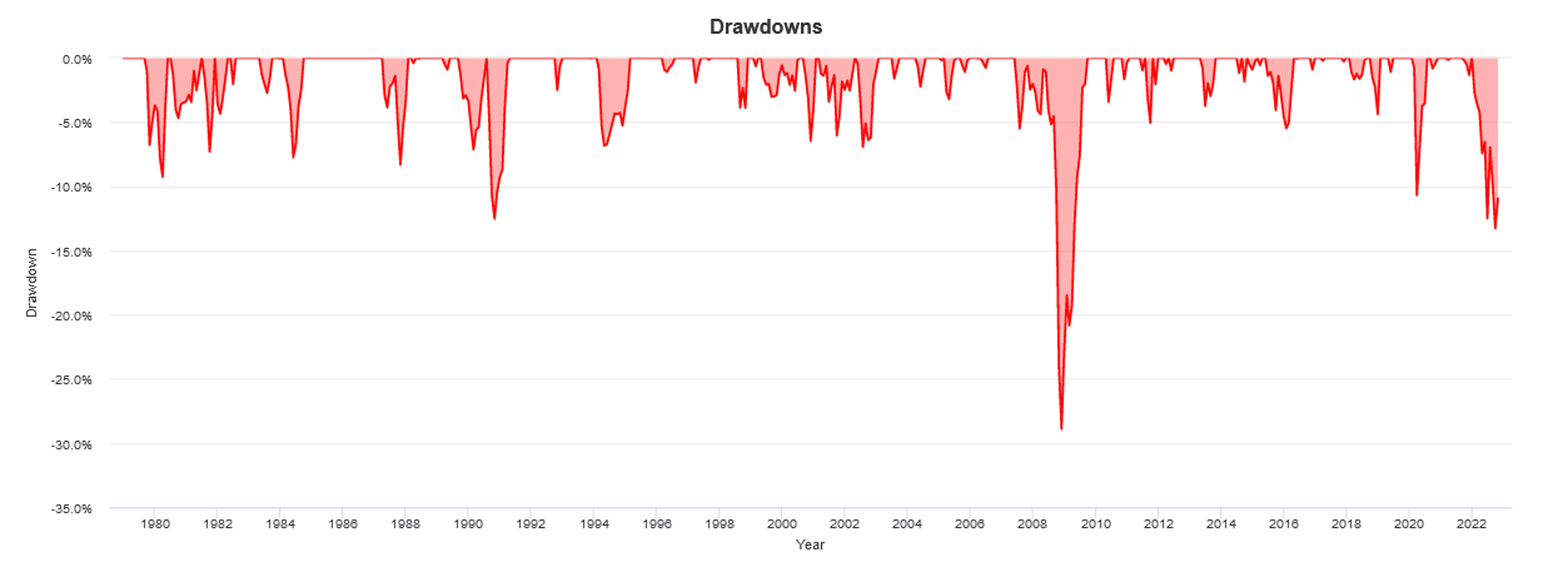

High-yield bonds can become increasingly correlated with equities during times of economic and market crisis. High-yield bonds suffered deep, prolonged losses during Black Monday 1987, the 1998 Russian Debt Default, the 2000 Dot-Com Crash, the 2008 Great Financial Crisis, and the 2020 COVID-19 Crash.

Source: Portfolio Visualizer

Source: Portfolio Visualizer

Source: Portfolio Visualizer

Tax Inefficiency

The income from high-yield bonds is taxable at both the federal and state level, unlike Treasury and municipal bonds that can have exemptions. Therefore, they aren’t the most tax-efficient assets when held in a non-taxable brokerage account. Their high income can lead to a comparatively high tax bill, especially for those in a high-income bracket.

Compare High Yield Bond Brokers

High-yield bonds can be researched and compared via various platforms. Investors looking for further insights and reviews of high-yield bonds can use Benzinga to compare the available options for buying high-yield bonds. Here is a list of brokers that support high-yield bond purchases.

- Best For:Most Available BondsVIEW PROS & CONS:Securely through Interactive Brokers’ website

Frequently Asked Questions

Are high-yield bonds a good investment?

The question of whether high-yield bonds are a good investment depends on an investor’s objectives, risk tolerance and time horizon. Generally, high-yield bonds are best suited for investors seeking enhanced income potential and who are comfortable with taking on equity-like risk. High-yield bonds have historically fallen as much as stocks have during market crashes and economic crises, and investors must be prepared to deal with high volatility. Because of their relative tax inefficiency and high yields, they’re also best held in a tax-sheltered brokerage account like a Roth IRA.

How do high-yield bonds work?

High-yield bonds work like any other bond. An investor who purchases a high-yield bond is basically making a loan to the issuing company for a length of time, and the company promises to pay a semi-annual coupon at a fixed annual interest rate and the principal back at maturity. The difference is that a high-yield bond has a greater default risk. There is a higher chance that the issuer of the bond may not pay the coupons or principal on time or in full. Because the credit risk is higher, the issuer of the high-yield bond must pay a much greater interest rate to entice investors and compensate them for the higher risk they’re assuming.

What is the safest bond to buy?

The safest bond to buy is typically considered to be a U.S. Treasury bond. These bonds are backed by the full faith and credit of the U.S. government, making them highly secure investments. Additionally, U.S. Treasury bonds are considered to have low default risk and are often used as a benchmark for other bonds.

About Tony Dong

Tony Dong, MSc, CETF®, is a seasoned investment writer and financial analyst with a wealth of expertise in ETF and mutual fund analysis. With a background in risk management, Tony graduated from Columbia University in 2023, showcasing his commitment to continuous learning and professional development. His insightful contributions have been featured in reputable publications such as U.S. News & World Report, USA Today, Benzinga, The Motley Fool, and TheStreet. Tony’s dedication to providing valuable insights into the world of investing has earned him recognition as a trusted source in the finance industry. Through his writing, he aims to empower investors with the knowledge and tools needed to make informed financial decisions.