“Growth potential as strong as the coffee,” one analyst noted even after Starbucks Corporation (NASDAQ:SBUX)'s disappointing third-quarter earnings call.

But, that did not stop the majority of Wall Street analysts from slashing their ratings and price targets on Starbucks, as it remains difficult to get a clear picture of where the coffee maker is heading in the near future.

A Closer Look At The Rating Changes

- Stephens: Maintains Market Weight, $58 price target.

- UBS: Maintains Buy, lowered pt from $70 to $67.

- BMO Capital Markets: Maintains Outperform, lowered pt to $64.

- Stifel: Downgraded from Buy to Hold, lowered pt from $66 to $58.

- Nomura/Instinet: Maintains Buy, lowered price target from $70 to $67.

China Remains Strong Growth Opportunity

Since the earnings call, numerous analysts have been highlighting slight concern regarding the company's future as management announced it would be closing all of its Teavana locations. However, despite this news, China remains a strong bullish thesis point.

Stephens analyst Will Slabaugh highlighted how “China was again a standout in the CAP segment — we expect this to continue going forward following the Company’s acquisition of all licensed stores in China.” However, he went on to say that while he likes Starbucks’ long-term opportunity and brand, he is still waiting for a better entry point.

Additionally, both Nomura analyst Mark Kalinowski and BMO analyst Andrew Strelzik noted the strong and highly-touted growth prospects in China as a key factor behind their Buy ratings.

Better-Positioned Than Most To Handle Decelerating Industry Trends

According To UBS analyst Dennis Geiger, Starbucks is in a good position to handle “a challenging macro environment remaining the biggest sss headwind, we remain encouraged that tangible sales initiatives support continued share gains and at least the lower end of +MSD comps.”

Four key drivers, he pointed out include: food and beverage innovation, digital development, operational enhancements and the My Starbucks Rewards loyalty program.

Taking A Closer Look At Comps

Strelzik highlighted how 5 percent U.S. comps were actually a pleasant surprise, but this number proved to be unsustainable.

“The return to sub-5% comps and lowered EPS outlook likely will reinforce investor concern that Starbucks’ long-term algorithm should be revised lower. Management did nothing to tamp down the concern as it mentioned several times that any potential updates to the long-term algorithm would be provided in conjunction with FY4Q earnings release,” Strelzik said.

But, he did highlight how 5 percent U.S. comps is actually a relatively strong number to its broad restaurant/retail competitive set. “As a result of the consistency and given SBUX’s reasonable relative valuation, we believe additional downside to the stock is somewhat limited, but greater confidence in renewed comp momentum likely will be needed for the stock to begin moving higher,” Strelzik concluded.

Disappointing Guidance Forecast

Starbucks lowered its fiscal year 2017 guidance to $2.05–$2.06 and its global comp outlook to +3–4 percent, which led analysts to lower their future comp expectations.

This lower guidance number was a primary reason behind Stifel Managing Director Mark Astrachan’s downgrade who noted how lower guidance highlights a continued deceleration in comparable-store sales growth.

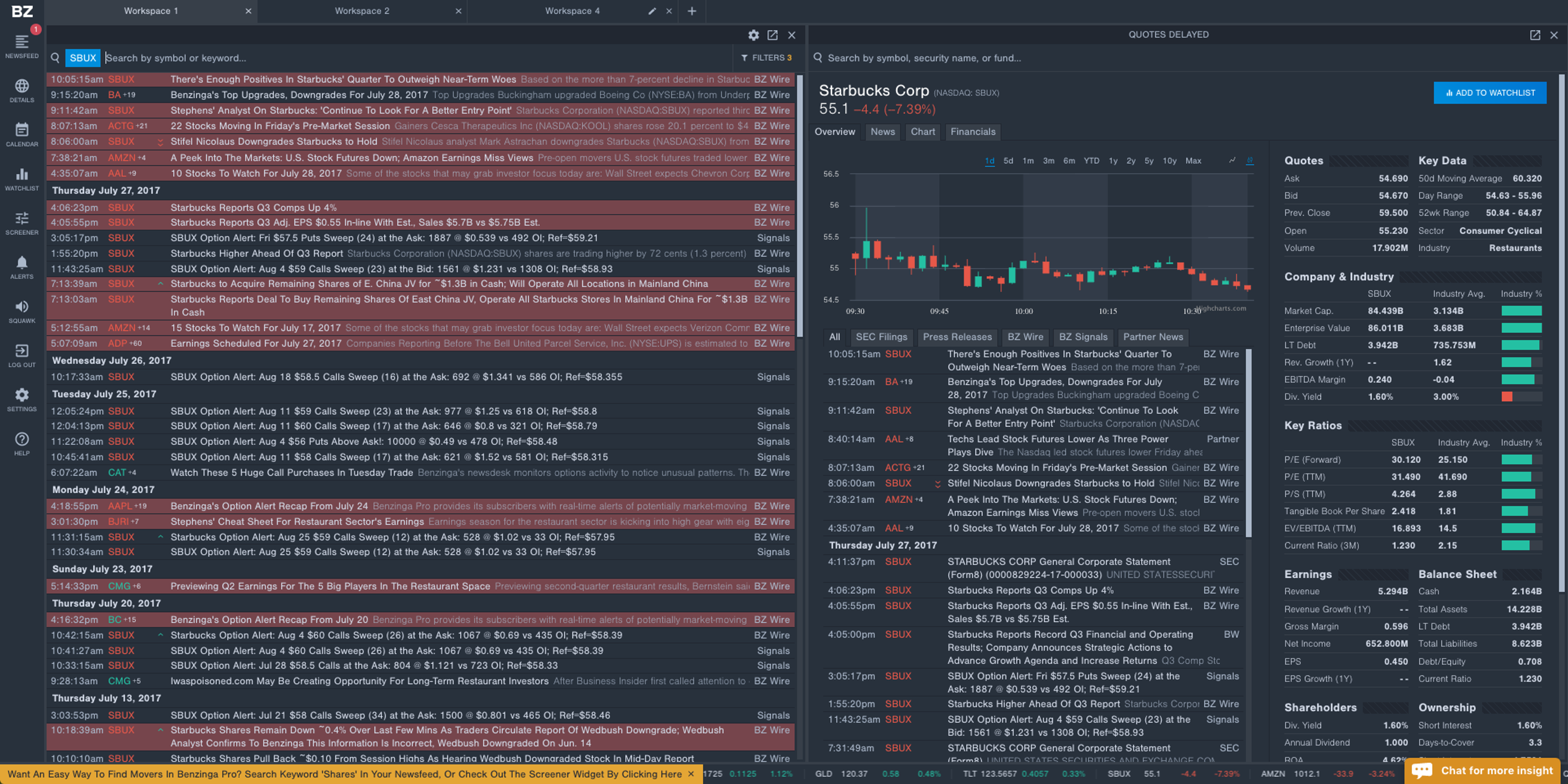

At time of writing, shares of Starbucks were trading down 7.9 percent, at $54.78. To take a deeper look at Starbucks' Q3 earnings report and to read the latest financial news, visit Benzinga Pro.

© 2026 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

To add Benzinga News as your preferred source on Google, click here.