Groundfloor is open to non-accredited investors and private individuals looking for active real estate alternative investment. More than 250,000 investors have invested over $1.3 billion into Groundfloor as of March 2024.

Individuals with small portfolios will also like the low $10 minimum and 0 investor fees. Most loans are lent to real estate entrepreneurs looking to flip homes or build new ones on vacant land. While there is a risk of borrowers defaulting on their loans, Groundfloor puts itself into a first lien position to mitigate as much risk as possible. In fact, even if a borrower defaults on a Groundfloor loan, it doesn’t necessarily mean you lose your investment. More often than not, you still get a return, albeit not as high as the original estimate. The average return rate for defaulted loans from Groundfloor is 6%, which is still higher than money markets.

- Charges the lowest minimums in the industry ($10)

- $0 investor fees

- Open to non-accredited investors

- Mobile app that allows investors to participate in deals starting from just $1

- Offers shares in its own notes as well as shares in convertible debt notes

- Offers no bankruptcy protection

- High rate of an uncured default

- Open to Non-Accredited?: Yes

Groundfloor Ratings at a Glance

Most people realize that investing in real estate to generate passive income is a good idea. However, relatively few investors do it. Ask them why, and you will likely hear a combination of “I’m not an accredited investor” or “I don’t have $25,000 to buy into a deal” or “I can’t lock money up for years.”

On the other side of the equation, if you were to ask real estate developers and home flippers what keeps them from closing more deals, you’ll get a combination of these responses: “The high vacancy rate means the bank won’t lend on it” or “The property is not fit for occupancy” or “The bank says I’m over-leveraged.”

That’s where Groundfloor comes in. This unique investment platform seeks to bridge the gap between investors and capital by offering high-yield, secured fraction real estate loans with small contributions from both accredited and non-accredited investors. Not only does Groundfloor welcome non-accredited investors, it's got buy-ins as low as $10. It even has a mobile app where investors can buy into deals for as low as $1.

So, to sum it up, Groundfloor offers investors a chance to fund loans with short turn-around times and high dividends. All of this begs the question, is it too good to be true?

How Does Groundfloor Work?

Groundfloor’s business model is fractional real estate debt investments. Groundfloor acts as a lender to developers in need of short-term funding to complete renovation or new construction projects. Developers and builders who are having difficulty accessing capital — or want shorter terms than a traditional loan — can apply for a real estate project from Groundfloor. Then Groundfloor’s team analyzes the subject property and works with the would-be borrower to make sure the property meets Groundfloor’s requirements and the borrower has a proper budget for the proposed loan.

Groundfloor’s loan business model has tremendous appeal for both investors and borrowers. First of all, most investors can’t even buy into secured offerings like real estate loans without accreditation. Secondly, the few such opportunities available to non-accredited investors have holding periods of several years. Groundfloor can turn around profits for investors in a matter of months. On the investor side, the opportunity to get access to funding without having to commit to a long-term loan is equally enticing.

Most investors are accustomed to paying fees and just accept them as a necessary evil of investing. They would, of course, like those fees to be as low as possible, but they expect to pay them. It should come as a relief to investors that Groundfloor has zero investor fees. That’s right. Zero. Groundfloor fees are paid by borrowers or assumed as a cost of doing business by Groundfloor. In either case, it doesn’t pass fees on to investors, which is a huge value add. It doesn’t get any better than zero. The 5 star rating is well earned here.

Groundfloor is astoundingly easy to use. Sign up is simple, and so is funding the investment account. As noted above, Groundfloor accepts both accredited and non-accredited investors; however, it uses a verification process for those claiming accredited status.

Groundfloor has a mobile-first approach to make real estate investing as simple as possible. With the Auto Investor account, your funds will automatically invest across a wide range of available loans. This instant diversification can help you see repayments as little as seven days.

All in all, it’s an incredibly user-friendly platform that both investors and borrowers will have no trouble navigating.

An investment platform that seeks to ingratiate itself to non-accredited investors needs to have a strong commitment to investor education. After all, if potential investors can’t get answers to simple questions like “How does this work?”, the likelihood of signing up and investing is basically zero. Groundfloor realizes this need, and its investor education platform is a strong one.

As with most platforms, a “Learn” tab appears at the top of the landing page. Scrolling the mouse over that tab reveals 3 sections: Frequently Asked Questions (FAQs), Support, Blog and Education Hub. Clicking on the blog will take users to the “Foundations” blog, which has over 100 different blog posts investors can choose from. Topics covered include the following:

- Company news and updates

- Facts, figures and analyses

- Groundfloor 101-basic breakdown of the site and how it works

- Borrower and project highlights

One of the best sections is the Groundfloor Investment Wizard, which is a great simulation that allows investors to estimate how their investments could grow based on a “conservative,” “moderate” and “dynamic” investment strategy. Needless to say the “dynamic” strategy is the one with the most potential risk and reward. However, the real jewel here is the opportunity for investors to get an idea of how they can grow their money with Groundfloor.

The FAQs section of the learning tab is equally well thought out. It’s particularly nice that this section opens with a search bar that allows potential investors to just type in their individual inquiry. This feature saves from having to scroll through dozens and dozens of answers unrelated to the question. Another strong point of the FAQs page is the way questions are grouped into several categories, which include:

- How to invest self-directed IRAs in Groundfloor

- Current lending guidelines

- Company information

- Investor breakdown on how Groundfloor works

- Account settings with basic information about setting up the Groundfloor account

Perhaps the only thing keeping this from being a 5-star section is the lack of video lessons. With that said, it’s hard to imagine a question an investor could have that’s not answered in the investor education section. In cases where that does happen, Groundfloor has a live chat option with an actual person and not a bot, which is also a huge plus for new investors.

Although funding real estate project loans is Groundfloor’s main focus, it’s not the limit of its offerings. Groundfloor also sells shares in its own notes and shares in convertible debt notes. These stock sales typically happen every other year.

When it comes to the core of its business model — real estate project loans with low buy-ins — Groundfloor has an impressive array of offerings in markets all over the country. Some have terms as short as 4 months, which gives investors room to grow wealth without locking their money up for extended periods of time. Add that to the fact that the minimum buy-in for these loans is only $10, and it becomes easy to give Groundfloor a 4.5 star rating for its offerings.

Having offerings with short hold periods and low buy-ins is all well and good, but it means nothing if they don’t grow wealth for investors. Groundfloor has a solid track record with an average 10% return on its investment offerings. Bear in mind that this is an average rate of return on all its loans, and past performance is no guarantee of future success. Every individual offering has a different risk grade and expected return, and risk of loss is always present. However, the solid return ratio speaks volumes about the quality of Groundfloor’s offerings.

- $10 Minimum

- 10% Actual Returns to Date

- $54.6 Million Total Interest Earned

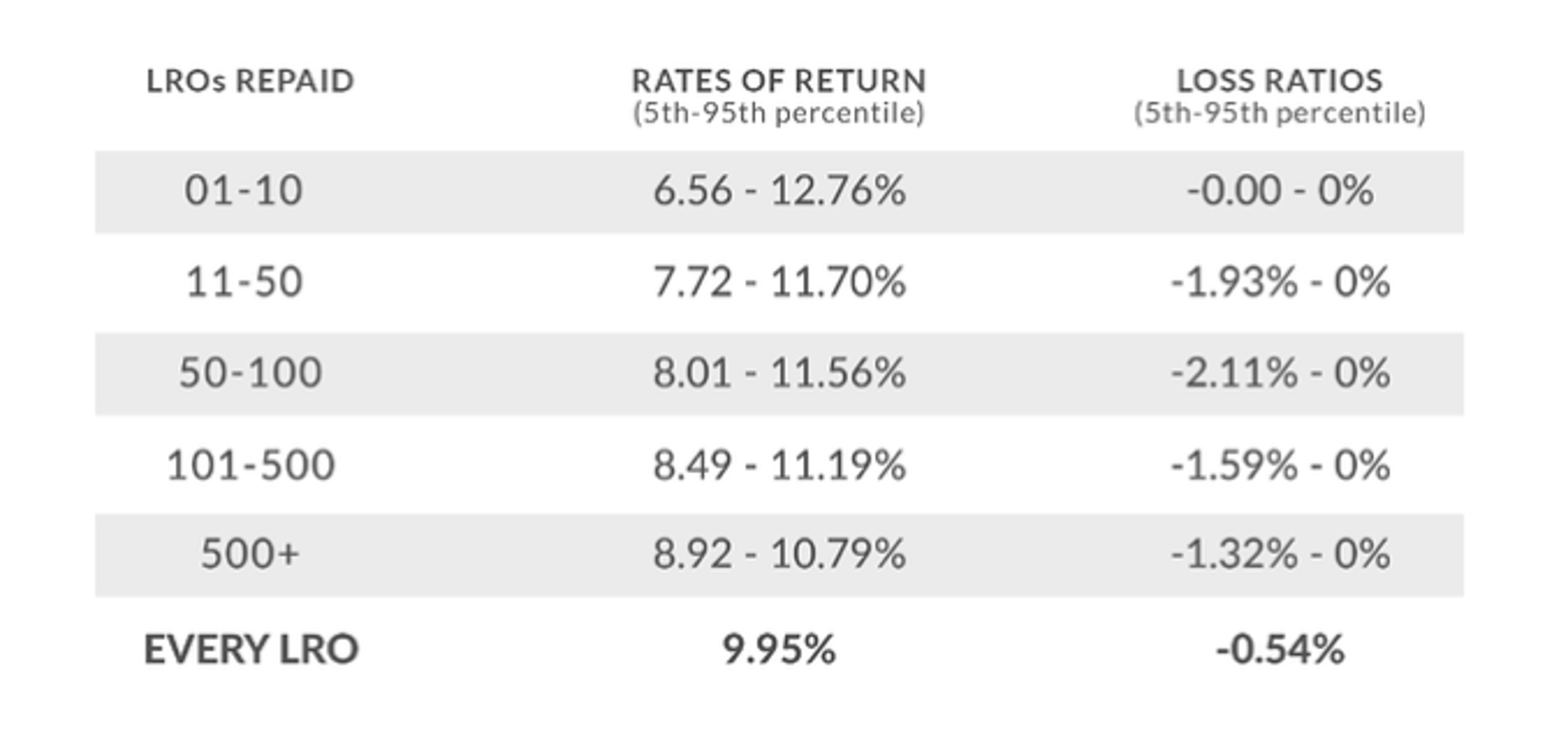

Groundfloor regularly publishes a Diversification Analysis, a report showing the loss ratio and rate of return based on the number of different loans an investor has in their investment portfolio. Based on the data, diversification across multiple loans has historically resulted in greater overall returns and a lower loss ratio.

Groundfloor isn’t a typical online platform that marries you to a desktop computer. While you can use a desktop or mobile browser, it has a mobile-first approach as we mentioned earlier. You can easily set up an account and set up your first one-time or recurring transfer in a few clicks.

The Groundfloor mobile app, which is available for iOS and Android, lets you see a complete overview of your entire Groundfloor portfolio, including your accrued interest, details of your returns, your average realized returns, and more. It also offers multi-factor authentication so you can feel confident knowing your account is more secure.

Groundfloor offers low buy-ins, short hold periods and high yields for non-accredited investors on offerings that are secured by actual real estate. That just about says it all. When it comes to opening the world of real estate investing up to the everyday investor, Groundfloor knocks it out of the park. It’s a well designed platform with a rock-solid business model and a strong performance history. Any investor looking to dip their toes into real estate investing would be well advised to experiment in Groundfloor’s pool. It probably won’t be long before they dive in head first.

Frequently Asked Questions

What is Groundfloor?

Groundfloor is a real estate investing platform that allows individual investors to participate in real estate projects. It is a fractional real estate debt crowdfunding platform that connects real estate developers with investors who are looking to invest in real estate projects. Groundfloor offers opportunities for investors to invest in loans that are secured by real estate, providing them with the potential for returns through interest payments. Investors can browse and choose from a variety of real estate projects listed on the platform, with different levels of risk and potential returns. Groundfloor aims to make real estate investing more accessible and transparent for individual investors.

How often does Groundfloor pay?

Groundfloor payments usually come in monthly, but you can see repayments in as little as seven days.

Can I trust Groundfloor?

Yes, Groundfloor is a safe way to invest in real estate.

User Reviews

Ron Thompson

High potential, but not platform and processes not ready for serious investment. Issues include meaningless loan maturity dates - 85%+ have lengthy extensions, little transparency and information regarding loan status, and high rate of loan default.