Right now, in the midst of low volume and low volatility, it is a great time to talk about markets.

Traders should take a look at margin account data, data that represents the actions of those who are borrowing capital to enhance returns.

Most traders know very well that volatility recently has dropped and hedge funds are being squeezed for returns, so it makes sense for them to take on more leverage to perform better and continue to be paid to outperform the market, something HFs have struggled to do since 2011.

Disconnected Reality

Currently, brokerages enjoy the interest they are collecting from their margin borrowers.

There's nothing wrong with that, outside of the skewed price representation as those who buy with credit are less judicious. This practice introduces irrationality as euphoria is driven by generating positive alpha in the short-term while mismanaging longer-term wealth creation through investment into asset classes that aren’t something tangible (A Snapshot Of What Happened In 2008).

In recent financial history, traders started to impose math upon the world instead of derive it from the world.

When this happens, the “assets” created are nothing more than a second-cousin, twice-removed from the purpose of finance, valuing a public corporation’s direct equity shares or direct loan/bond certificates on earnings capability and creditworthiness.

As was noted this week, Goldman Sachs believes that equity assets are currently driven by P/E multiples and not direct corporate earnings.

This can be seen as troubling and an indicator of euphoria.

When in dire straits, a majority of investors become more calculating about how to part with capital, what to invest in and what to trade this “tool” for.

So if euphoria is present and prices are not only over-valued, but also inflated (thanks to non-judicious investment along with easy and cheap money), what will happen when there's a correction and suddenly the market becomes more analytical, more discerning about capital deployment, more judicious in its decision making?

The fall is always faster than the climb.

Randomly Walking Without A Clue

With leverage and debt, at least in finance, debt isn’t something that manifests and then removes itself.

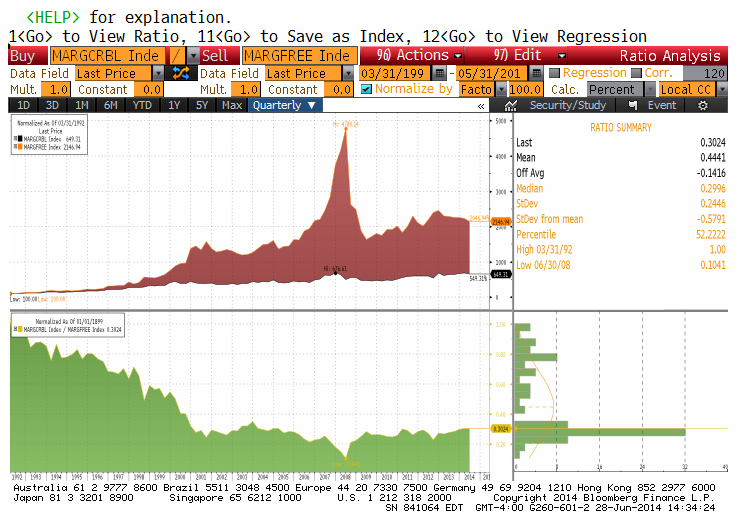

Just look at the disconnect around the 1999 Dotcom bubble in the image below. Investors observe how debt explodes above equity from that point on.

Debt allows set inflated prices. Prices will remain “skewed” because the base amount of debt priced into the system increases. Markets are entering uncharted territories again. The Fed will be removing its monthly purchases from the equation and the viability of this “recovery” will be challenged in 2015.

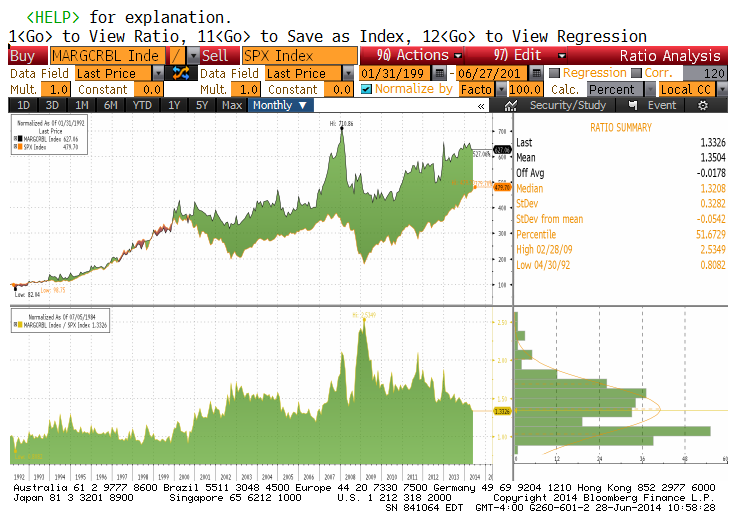

(Figure 1) NYSE Free Credit Balances In Cash Accounts And S&P 500

(Figure 2) NYSE Free Credit Balances: Margin Accounts Minus Cash Accounts

Is The New Normal More Like Original Irrationality?

The US had to revise its GDP this week and recorded a 2.9 percent loss in product and the markets maintained their upward push.

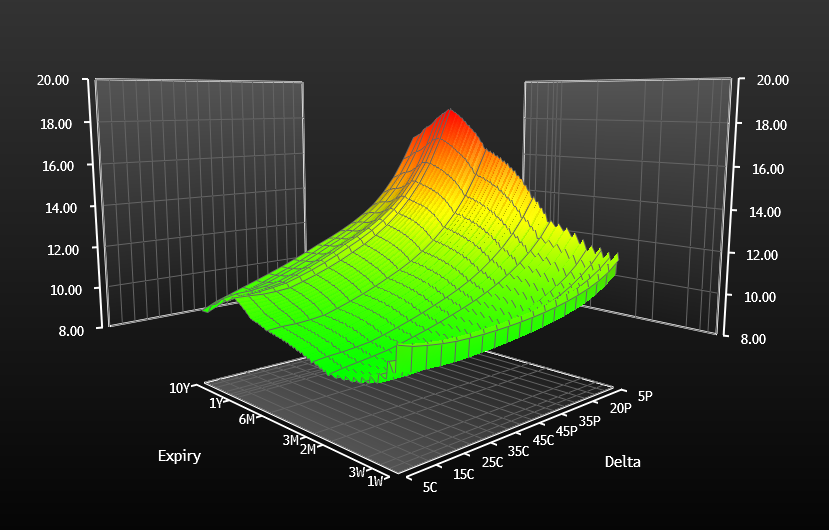

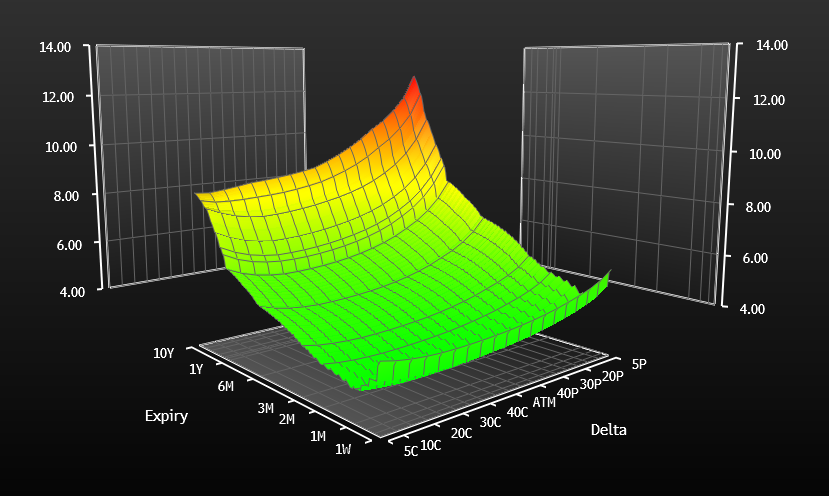

The hubris of the quality of this “recovery” is also evident in the EUR/USD volatility smiles.

Compared with two years ago, the current shape implies that relative to bears, there are a lot of bulls.

Given the size of the players in the FX markets, it would be reasonable to deduce from the shape of the curves that globally, the big money players are feeling more comfortable about not just the short term but also the longer term.

EUR/USD Volatility Smile 2012 on Top and 2014 on Bottom (data: Bloomberg)

Conclusion

Many of us have learned from the hubris of 2007 and we are right back there again.

Anyone else seeing multiple Dotcom commercials on TV again? Credit is high, housing is hot (San Francisco just recently fell below the 20 percent annual housing price appreciation mark for the first time in 14 months), and hubris is back even though the US economy had contracted by 2.9 percent in Q1 2014.

When the Fed raises the Federal Funds rate, the make of up of this value-skew, easy credit, excess liquidity and Fed removed risk recovery the structural make up will fail and markets will be back to the beginning, having done nothing for the longer-term creation of wealth through markets.

One thing about credit and structured finance is that contracts are involved and tangible wealth creation is available through a tactic known as “litigation arbitrage,” a topic to be covered another time.

Loading...

Loading...

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Posted In:

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in