With the merger and acquisition market really heating up as of late, the Street has been sending mixed signals to the shareholders of the acquirers.

In several instances, the street has looked kindly on the move and rallied the share price of the company being acquired as well as the share price of the acquirer.

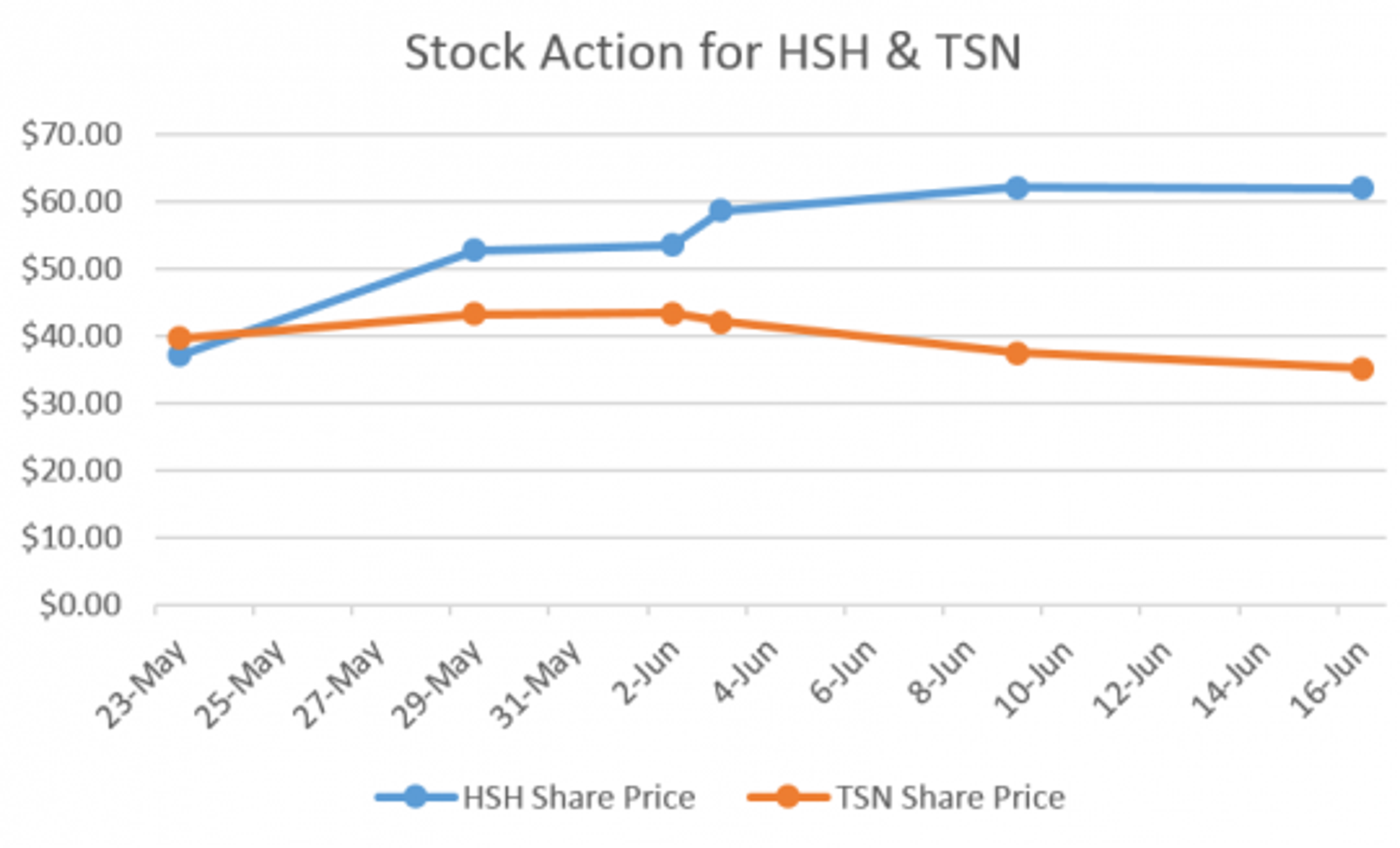

However, this is certainly not the case with respect to the Tyson Foods TSN acquisition of Hillshire Brands HSH after a prolonged bidding war. In the end, Tyson ended up purchasing Hillshire at nearly a 70 percent premium to its May 23 closing price ($37.02).

History of buying competitors

Growing by acquisitions is nothing new to the company. In 2001, it acquired IBP Inc, which at the time was the largest beef packer and number two pork processor in the US, for $3.2 billion in stock and cash.

Over the next several years, Tyson has made numerous acquisitions in the food industry including Hudson Foods Company, Washington Creamery, Prospect Farms, Wilson Foods, Honeybear Foods as well as several others.

The company has not only targeted other public companies, but private companies as well. In June 2013, Tyson acquired the assets of Circle Foods. Also, in January 2014, it acquired the assets of Bosco's Pizza. Of course, these acquisitions were much smaller in size and with few competing bids they likely added to the bottom line for the company fairly quickly.

Tyson Shifts its Focus

In contrast, the takeover of Hillshire was only completed after a prolonged bidding war with Pilgrim's PPC. In a complicated series of moves, involving Pinnacle Foods originally being bid for by Hillshire, Tyson announced a cash offer for Hillshire on May 29 for $6.13 billion or $50.00 per share.

Hillshire, which had already appreciated from $37.00 to $45.00 from the possible synergies of the Pinnacle Foods acquisition, added another $8.00 to close at $52.79 on May 29. Obviously the street believed the $50.00 price would not be sufficient and it traded at nearly a $3.00 premium to the Tyson offer.

Only two days later, Pilgrim's upped the ante by offering $55.00 for the company. Still, the Street was not satisfied with the proposed offer as Hillshire shares closed at $58.65 on June 3. Finally, on June 9 Tyson ended the bidding war for Hillshire and offered to pay $63.00 per share.

Not only did the Street force Tyson to buy the top in Hillshire, it has also put a long-term top in its share price. After just missing its all time high ($44.24) on May 29, reaching $44.00, the issue has swooned to the $35.00 level in only twelve trading sessions.

The higher the company bid for Hillshire shares, the lower its own share price went. Even after the bid was finalized on June 9, as Tyson went from $40.12 to $37.50 in that session, it has shed another 2.5 points, and is threatening to breach the $35.00 level for the first time since December 2013 in Monday's session.

Long-term implications for Tyson share price

When it takes an issue nearly seven months to rally from $31.45 to $44.24 and it gives much of it back in a few weeks, one thing is for certain, it is not going back to $44.24 anytime soon.

Long-term and or institutional investors have exited the issue. This is supported by the spikes in volume that took place as the deal was finalized on June 9 and 10. Perhaps these investors believe the company overpaid heavily for its latest acquisition and that it may take longer and be more costly than the company estimates to integrate the two companies.

Also, all the “buy the dippers” that were waiting for a pullback in Tyson are now under water and if the $35.00 level is breached, it may initiate another wave of selling. The selling may come from these shorter-term players hitting the exit button or an exodus by institutions that were waiting for a rebound to sell their shares. Of course, any rebound in the issue will have both parties competing for bids and both may fall prey to High Frequency Traders who will ferret out any sizable offers and attempt to trade ahead of those orders.

Every merger and acquisition has its own set of circumstances that will dictate the future price movement of the acquirer. However, investors should take note that if a bidding war ensues for a company, the winner of the bidding war can actually turn out to be the loser. As in the case of Tyson Foods, the street is saying that the company may have just overpaid.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.