This article is part of an ongoing series about the importance of end-of-life planning at all ages. Check out the previous installment of this series here.

When thinking about the important elements of being financially secure, many people immediately recognize the necessity of a savings plan, retirement funds, emergency cash and robust credit. However, end-of-life planning and life insurance play a critical role in how your financial security will play out for the entirety of your lifespan.

As you age, financial security does not remain stagnant; it changes with life events, broad economic trends and personal gumption. Being financially secure in early adulthood does not look the same as being financially secure in retirement. However, there are steps that can be taken to ensure that your financial situation will mature as you age, changing and adapting to all of life’s uncertainties.

One aspect of this strategy is end-of-life planning, and inevitably, life insurance is crucial to this plan. Particularly for Millennials, who are just in the beginning stages of financial independence and on the arduous, decades-long journey of financial readiness, understanding how important this component is to overall financial health cannot be understated.

Benzinga spoke with Adam Paoli, financial strategist at the Heartland Group (Penn Mutual Insurance Company’s Chicago agency) about the role life insurance plays in the greater financial picture.

Benzinga: What Are The Initial Steps Millennials Need To Take When Considering Life Insurance Options?

Adam Paoli: There are two initial questions that must be explored: How much and what type?

The first is by far the most important, as the primary purpose of life insurance is to protect the insured’s income earnings capability via the death benefit. In the event of a catastrophic illness, the type of coverage becomes irrelevant. They should speak with a professional to help them not only calculate their current need, but more significantly to understand their current value and protect that full value of their income earning potential— much as they seek full protection of every other asset they insure […] homes, jewelry, etc.

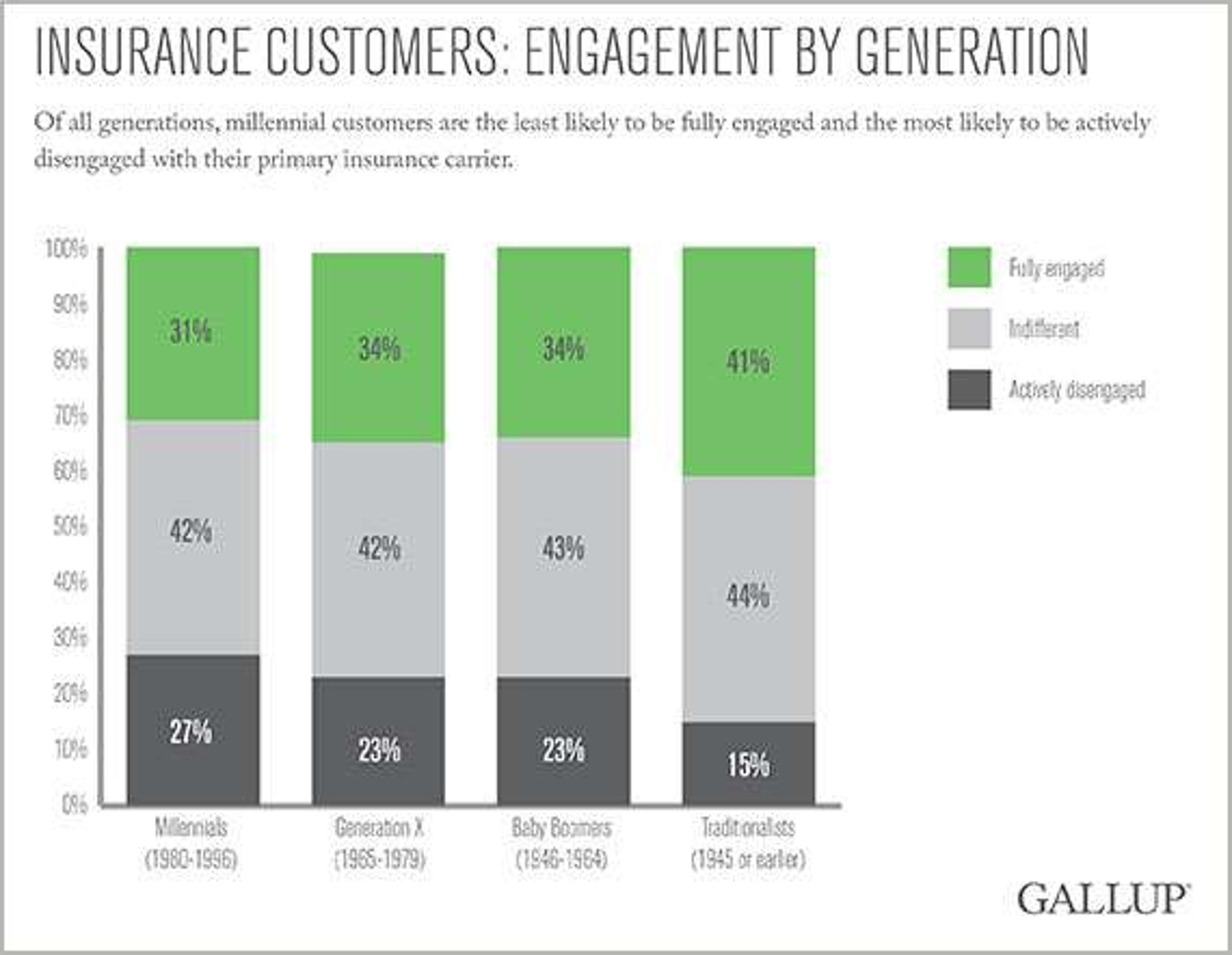

Source: Gallup

Next, they need to understand the different types of life insurance plans. Simply categorized by temporary and permanent plans, Millennials are well served to become educated on each, including available riders, so they not only acquire the correct amount of coverage, but also make the best financial decision and pay the least amount of trust cost over their lifetime [emphasis].

How Does Life Insurance Fit Within The Retirement Planning Umbrella?

Adam Paoli: Life insurance can take several roles to assist Millennials in planning for their retirement. Many advisors spend time on the significant tax benefits that cash value policies enjoy (similar taxation to Roth IRAs), and as most Millennials are concerned about the potential of future increases in federal income taxation of their lifetime, this can be very important.

But, more important may be the role that guaranteed cash value contracts have to enhance an individual’s ability to take income during retirement. Recent research shows that having three to five years’ worth of retirement income in guaranteed cash value contract may allow an individual to substantially increase retirement withdrawal rates: By not having to pull from their retirement asset accounts in down markets, their portfolio may have more time to recover and, as a result, may allow for investors to withdraw higher annual retirement income rates over the long term.

Source: LIAM And Aflac

What Advice Do You Have For Millennials When They Have A Completely Blank Slate?

Adam Paoli: Many Millennials tend to focus more on where their money is being placed rather than how much is being saved. Although we are proponents of diversification* of assets classes, taxes and investment vehicles, we spend a good amount of our time with ‘blank slate’ clients stressing the importance of building strong systematic [emphasis] savings levels [aside: Systematic in that they are automated, happening without manually decision making. For example, direct deposit to savings from checking].

We stress having good cash reserves and becoming excellent monthly savers. Once that habit is established, they will be better prepared for cash flow planning conversations to direct their monthly savings to wealth creation.

*”Diversification does not guarantee a positive return or eliminate the possibility of loss. Past performance is no guarantee of future returns,” Paoli added at the end of the conversation.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.