Goldman Sachs decided Friday night was a good time to tell the world how bearish they are ahead of the Q1 2016 earnings season.

In lieu of comments read from the perch of the Benzinga Pro news desk, we determined it would be of value to all our readers for us to highlight some of the recent notable comments from analysts regarding Q1 earnings expectations along with some focus point comments on Financials and Credit markets.

To lead off, we'll continue with David Kostin's view on Q1 earnings.

The three reasons Kostin is bearish:

- Consensus expectations for flat Y/Y EPS growth looks to be the best case. Kostin expects EPS growth to decline 9 percent, led by Financials XLF and Energy XLE.

- Historically, companies lower EPS guidance for the subsequent quarter which drives down revisions to FY EPS guidance, meaning stock prices have to be revised lower to account for the weaker performance guidance.

- The only demand source for shares is corporate buybacks. Kostin notes more than 75 percent of S&P 500 constituents are unable to execute discretionary buybacks until early May.

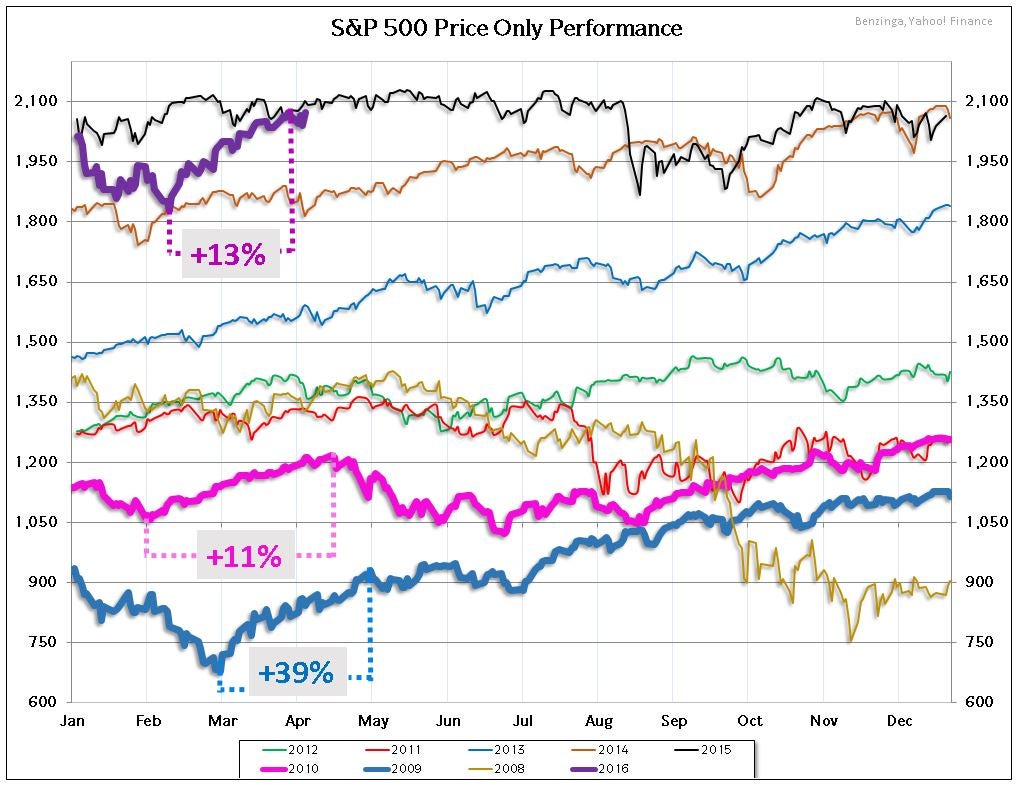

Equity Market, Where Are We Now?

It's certainly not 2009 but the post-January rebound we've seen in the S&P has analogues in recent history:

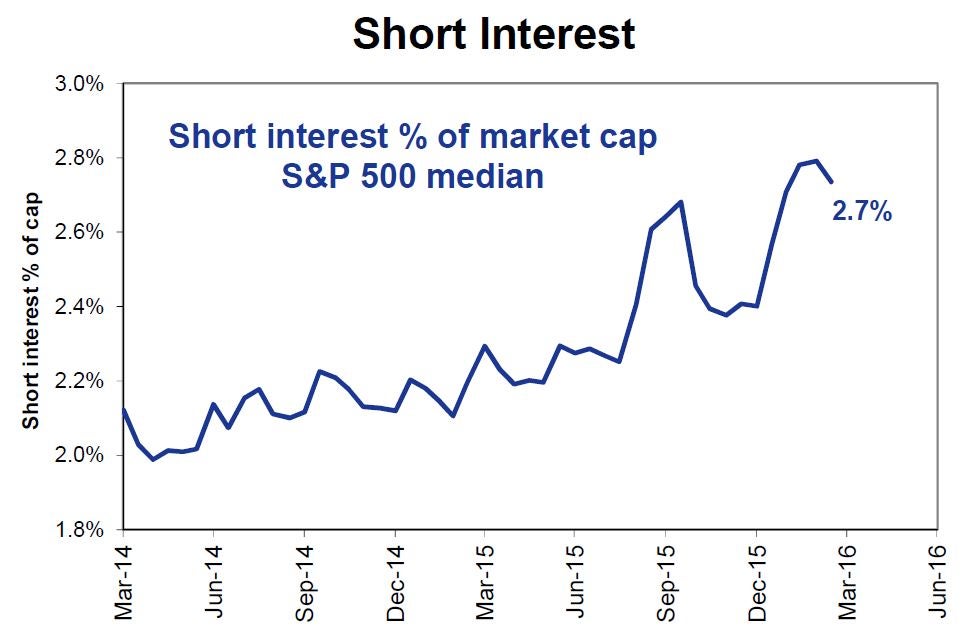

Going back to Kostin, he shares a chart pointing to an increasing short-interest as a percent of the median market capitalization of S&P 500 companies:

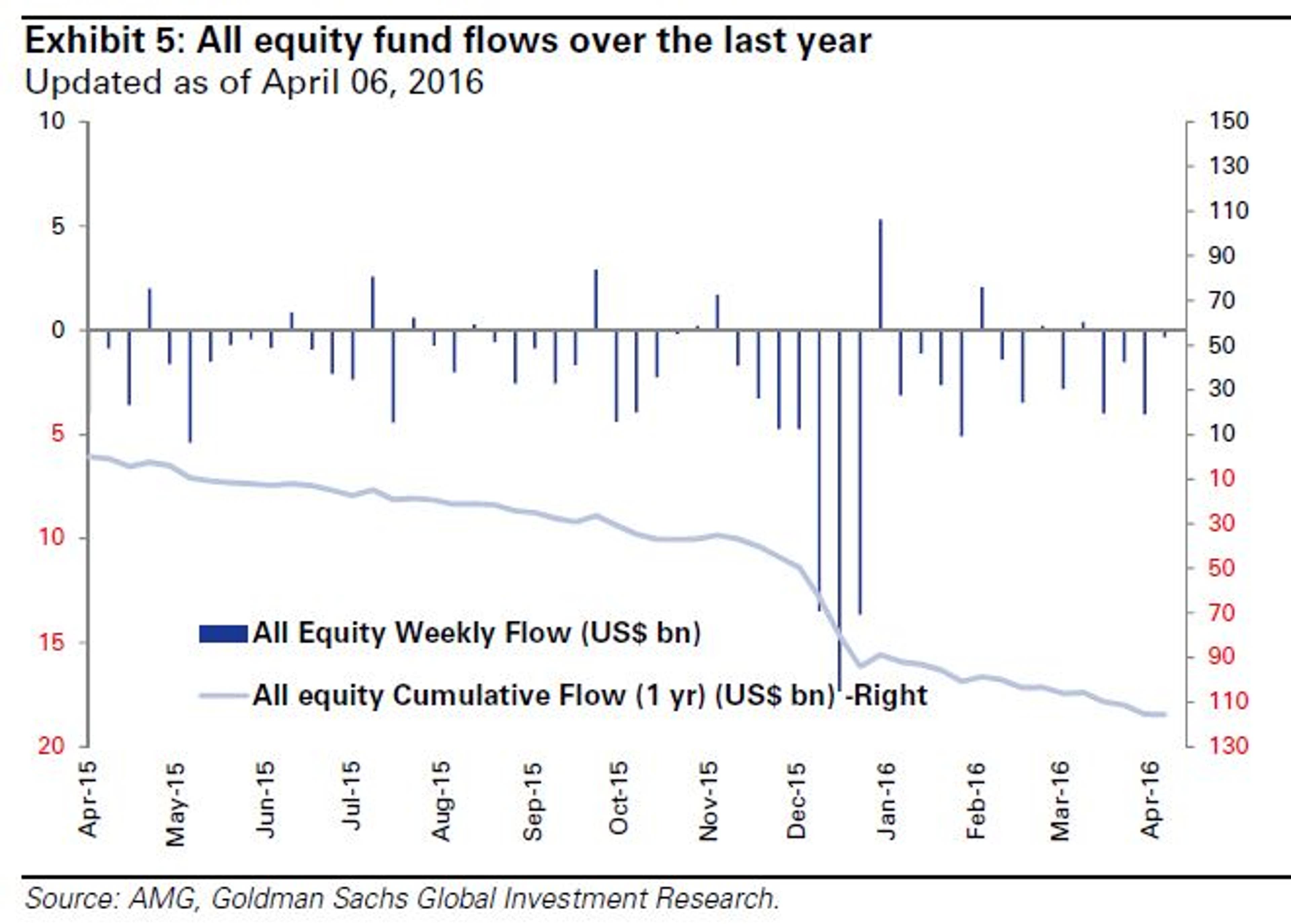

It's relatively easy to get bearish in the near-term. US equity fund flows continue to bleed out according to Goldman Sachs analyst Peter Callahan:

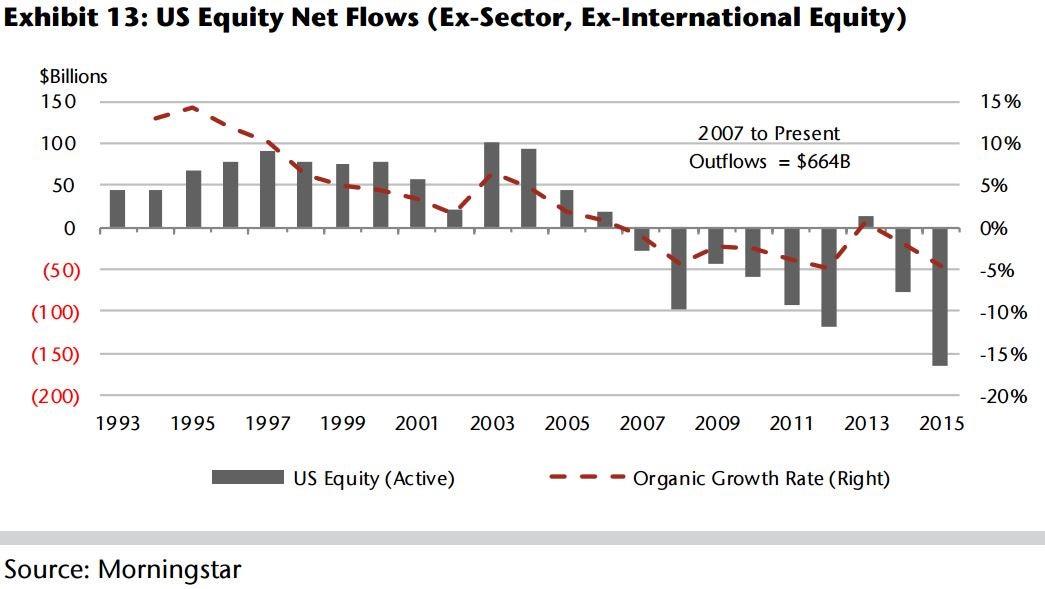

Jefferies' Daniel Fannon called attention to record outflows in actively managed domestic equity funds, a trend he expects to continue. From 2006 to 2015, net redemptions totaled $648 billion:

The clear favorite from Fannon in the managed asset space is Buy rated Legg Mason LM which he expects will grow FY 2016 EPS by 90 percent Y/Y and will grow FY 2017 EPS by 79 percent Y/Y. Legg Mason reports on April 29th, premarket.

Financial Sector Expectations

Nomura's Bill Carcache expects negative EPS revisions to be the driver for banking underperformance. Carcache says banks are feeling pressure to increase reserves as the inflection point in energy-related credit losses as yet to manifest.

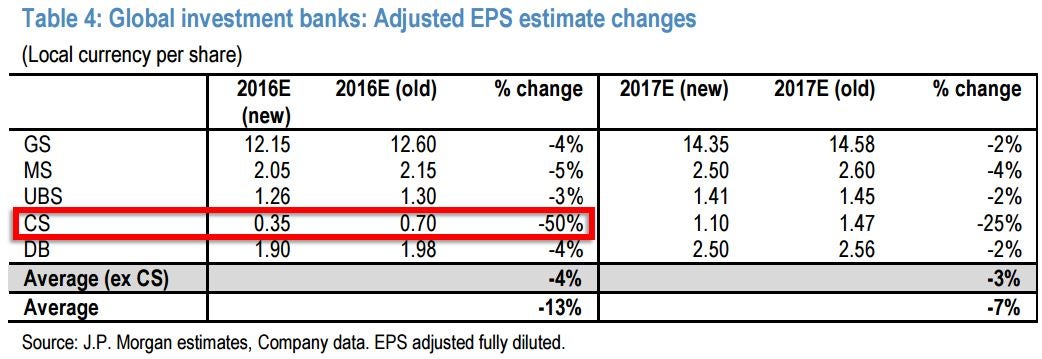

JP Morgan's Kian Abouhossein is bearish on investment banks. In a recent note, the analyst cut FY 2016 EPS estimates for the group. We've highlighted the extreme bearish view on Credit Suisse CS in the table below which Abouhossein explains is predicated upon the Credit Suisse's "unambitious cost targets" and a "backdrop of EPS consensus cuts leading to an unattractive risk-reward profile."

Aboushossein has a Neutral rating on Credit Suisse. Credit Suisse reports on May 10th, premarket.

For what it's worth, Credit Suisse rates JP Morgan JPM at Ourperform with a $75 and has the bank on the Credit Suisse US Focus List. The analyst, Susan Katzke, expects JP Morgan to report Q1 2016 EPS of $1.35 in her most recent note on the bank. JP Morgan is scheduled to report Wednesday, premarket.

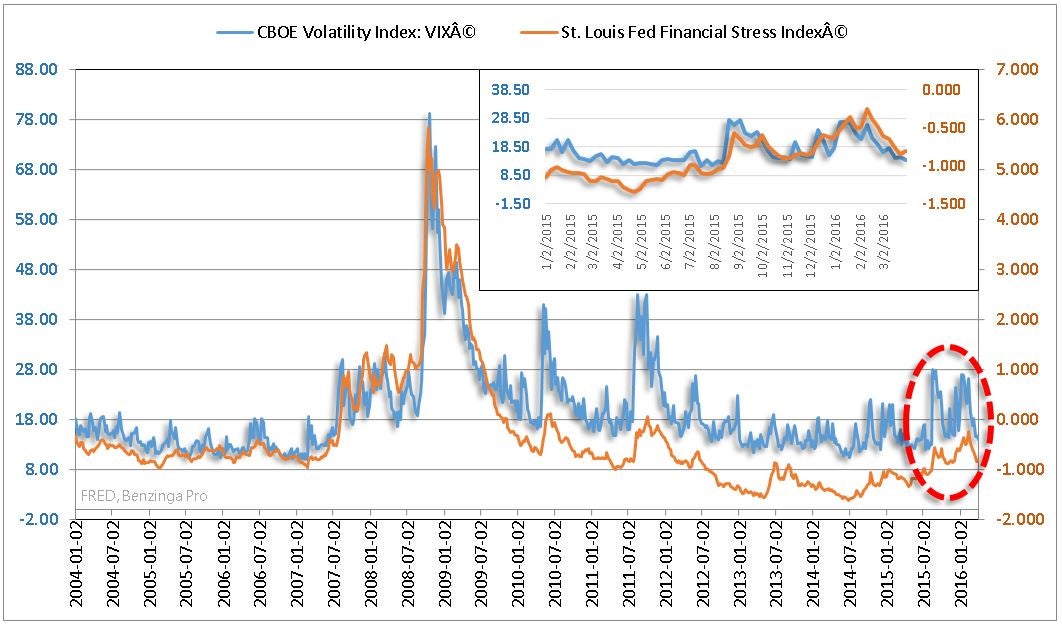

As a tangent to financials is the Financial Stress Index. Comparing CBOE Volatility Index and St. Louis Fed's Financial Stress Index yields evidence of a slighly elevated level of concern among investors:

Credit Market Expectations

The world continues to look for an equilibrium in the energy complex in the midst of a contracting credit market and efforts to boost prices with unfounded, yet-to-be-put-in-writing, production freeze comments.

A source involved in the trading of energy paper contracts and the management of physcial inventory in Canada told Benzinga back in February that a major lender to Junior names had been requesting companies issue equity offerings to repay loans, immediately.

A separate source based in Asia who trades similar short-term energy contracts and also manages a physical warehouse of inventory told Benzinga of the issues witnessed with companies in regards to fund raising from the High Yield debt market.

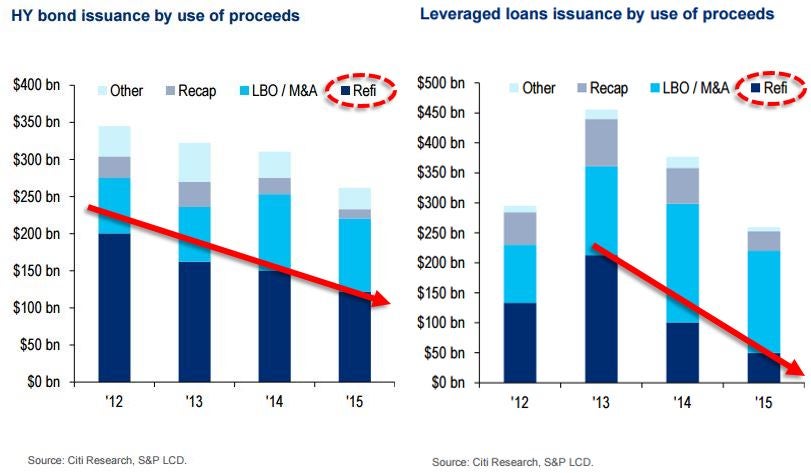

Funding problems come as no surprise in lieu of a January note by Citigroup's Credit Strategist Stephen Antczak which called attention to the decline in use of HY Bonds and Leveraged-loans used to refinance:

Antczak's reasoning for the decline is simple: "the biggest risk for credit in the near-to-intermediate term is mark-to-market risk" or, said another way, rapidly deteriorating valuations risk pressuring short-term lending further.

Moody's Analytics' John Lonski says many corporations remain willing to take on additional financial risk in an effort to stoke shareholder returns. Lonski wrote on April 7th "...amid subpar economic growth, such risk taking only increases the likelihood of a gamble gone wrong

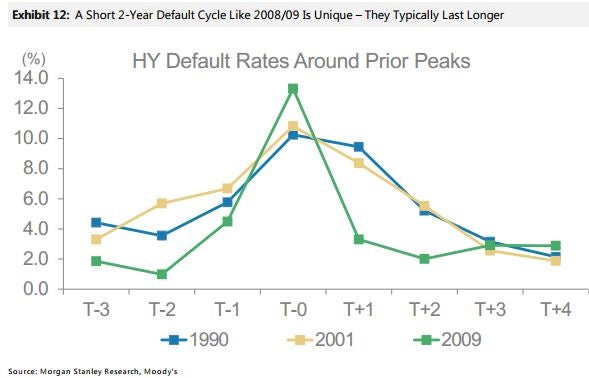

When it comes to default cycles, Morgan Stanley's Adam Richmond cautioned that recoveries typically take 3-4 years as opposed to the 2 years it took for HY Default Cycle to run it's course in 2008. When it comes to a recession in a low rate period, Richmond noted "if a recession hits while rates are still low, the lack of available central bank tools could mean a longer period of low growth

JP Morgan shares Morgan Stanley's view on low growth, saying "Investors and policy makers are starting to notice [worsening global productivity] and are adjusting to a now much lower long-term growth environment, even absent a recession. For central banks, this mean low interest for a long time, even as they are running out of ammo here".

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.