Why is one office REIT projected to prosper in a rising rate environment?

On July 13, Goldman Sachs Global Investment Research analyst Brad Burke and his team published a research note updating ratings and price targets for the office REIT sector, with a focus on three of its biggest players:

- Boston Properties, Inc. BXP $19 billion cap, 2.1 percent yield; Buy.

- SL Green Realty Corp SLG $11.4 billion cap, 2.4 percent yield; Sell.

- Vornado Realty Trust VNO $18.3 billion cap, 2.6 percent yield; Hold.

In addition, Goldman has lowered the entire office REIT sector to Neutral from Attractive.

Burke's updated thesis is that growth will be harder to achieve moving forward, and uses and sources of capital will be the main differentiator between the REITs in his coverage universe.

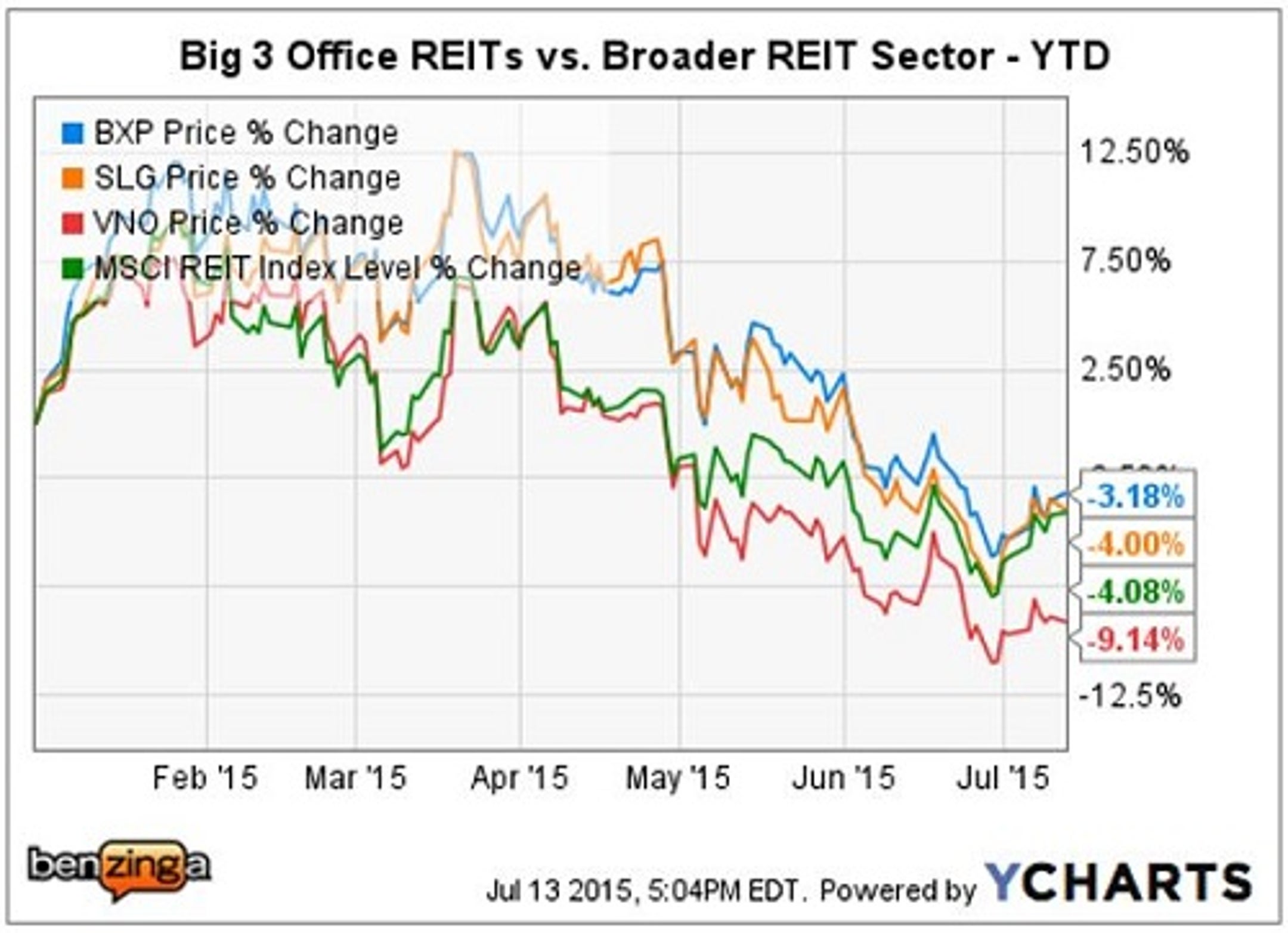

Tale Of The Tape - Past Year

New REIT Paradigm In A Rising Rate Environment

Burke observed that, "The market has rewarded acquisition-driven growth, funded with low-cost short duration debt. REITs that have built cash, sold mature assets, and reduced debt have under-performed."

He expects growth moving forward to be driven by:

- Low-cost capital from free cash flow, debt or cash on the balance sheet.

- Higher yielding development opportunities will trump acquisitions made at low cap rates.

- Organic growth from rent escalators and roll-over of below market rents.

- REITs limiting exposure to floating rate debt, and reducing the spread on mezzanine loans.

Goldman's previous bullish view on CBD office REITs, "was largely predicated on the belief that accelerating liquidity would cause meaningful cap rate compression and, therefore, an expansion of office REIT multiples."

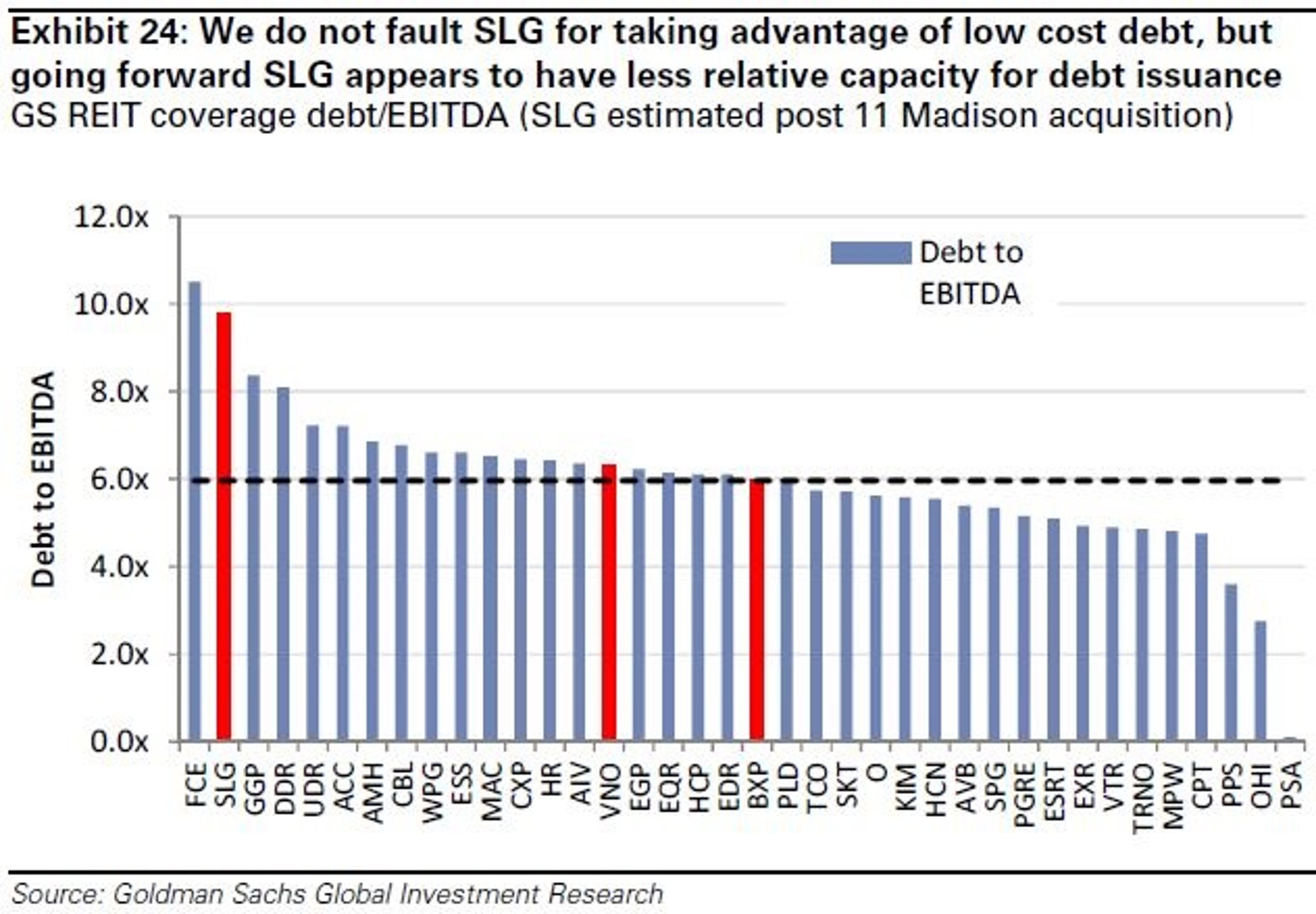

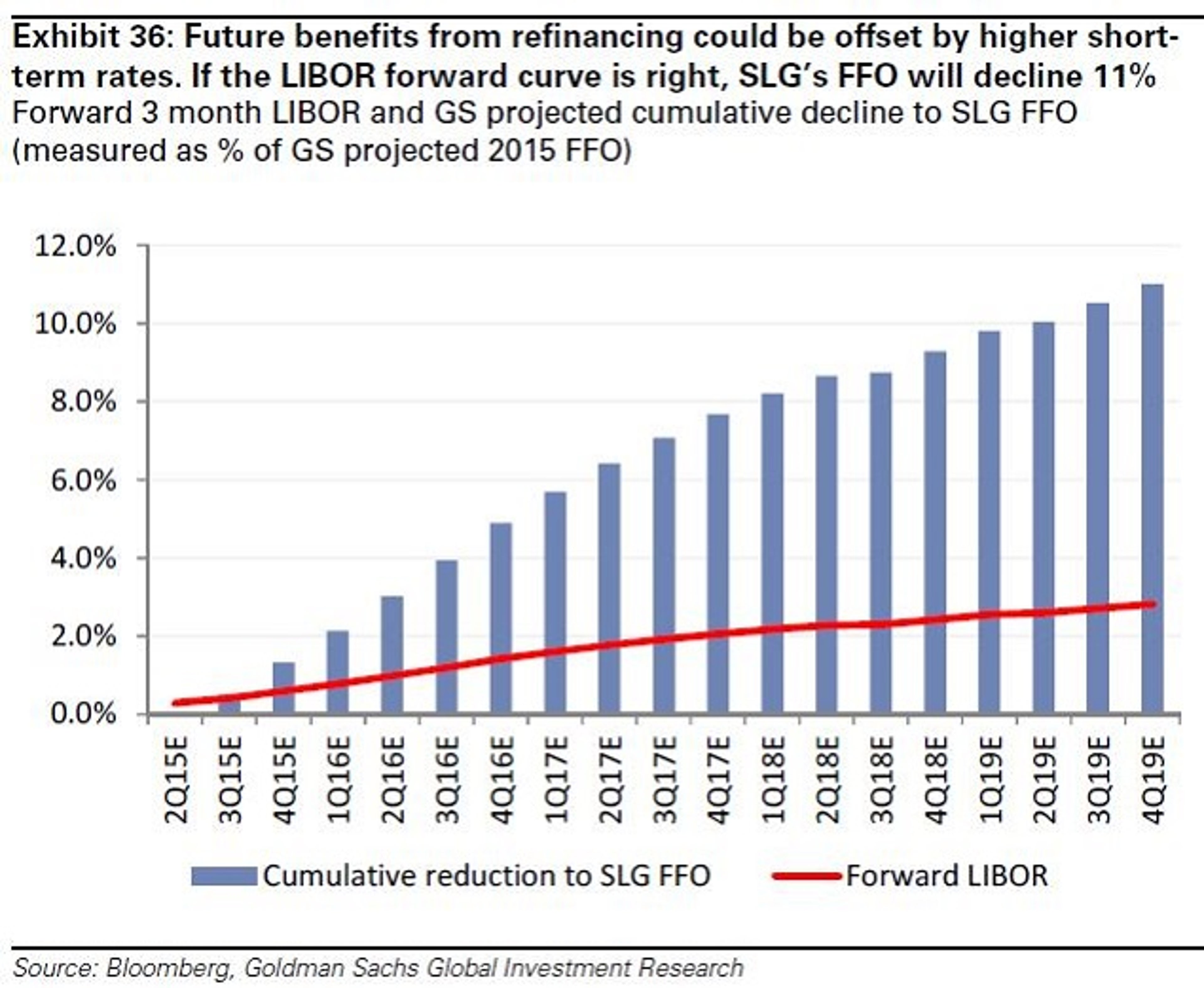

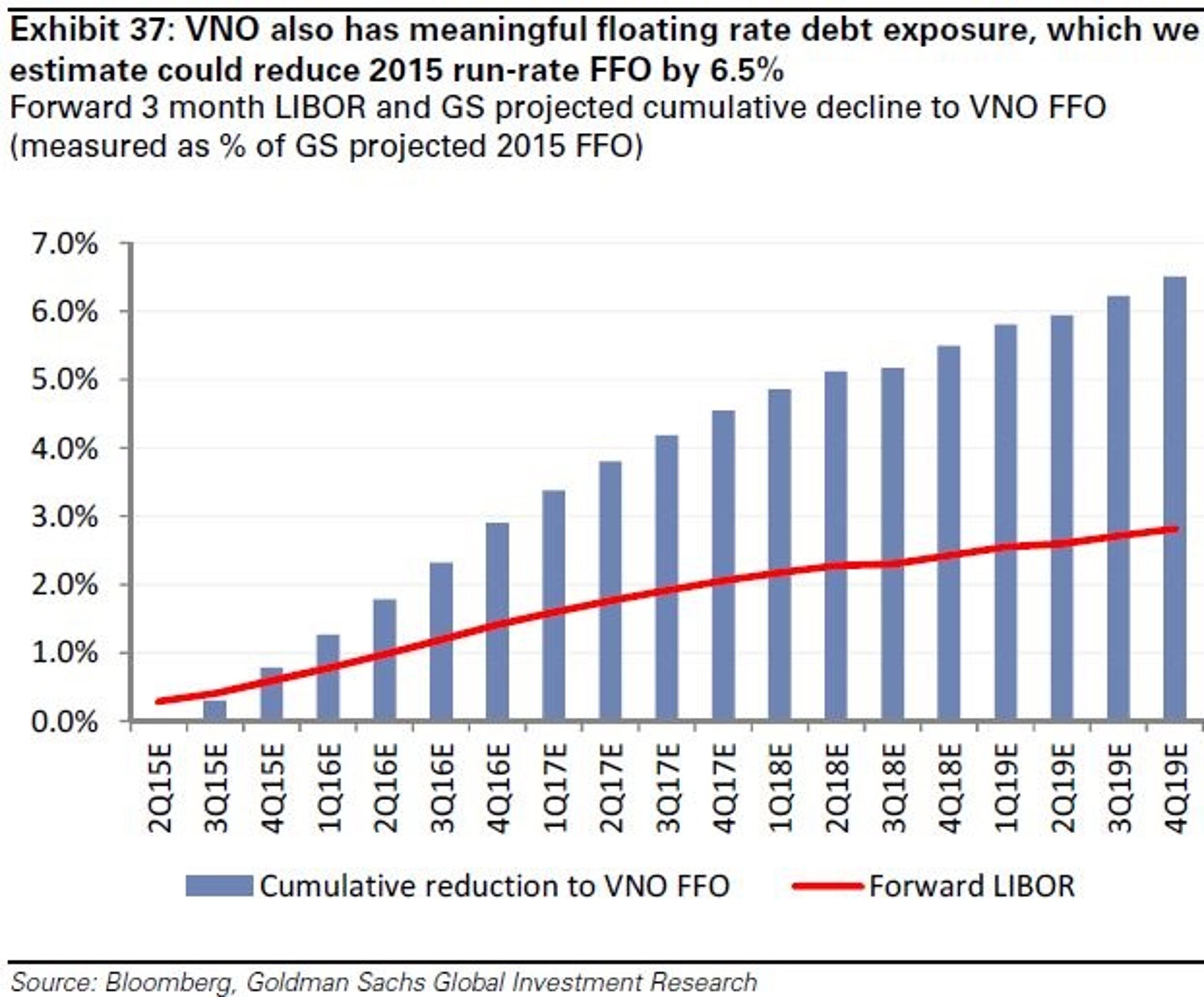

Contrasting Balance Sheet Strategies

The three charts below illustrate the divergence in strategies, which has contributed to the past outperformance by SL Green vs Boston Properties:

Boston Properties

Goldman's Boston Properties Buy case reflects, no floating rate liabilities, plenty of dry powder and CBD development projects where it can be put to work generating attractive ~7 percent going in cash cap rates.

Goldman expects BXP to: 1) Beat consensus FFO estimates, e.g. GS 2016E FFO is 3.7 percent higher; 2) Add more development projects to its existing pipeline; and 3) Another special dividend, (~$500 million), is likely to be announced in 4Q/15 or 1Q/16.

SL Green

Goldman's $105 12-month target price "implies 8% downside vs. the average 9% upside for the remainder of [REITs under] coverage."

Goldman expects:

- The Fed's increase bias for short-term interest rates represents a headwind.

- Compressing spreads on new debt and preferred share issuance.

- Limited leases coming due in Manhattan vs suburbs will lower same store growth.

- Future acquisitions will struggle to be accretive to FFO.

Additionally, "If SLG were to continue to originate debt and preferred equity investments around its current average yield of 10.3%, absent an increase in the riskiness of these investments, it would make [Goldman] more positive."

Notably, Goldman believes that the purchase of 11 Madison by SL Green -- a mature building with little upside in the leases -- underscores the low likelihood of a "rent spike" in NYC at this point in the CRE cycle.

Vornado

Notably, "With VNO now indicating its portfolio transition is largely complete and with the REIT now guiding to flat EBITDA in Washington, DC, [Goldman] believe[s] a Neutral rating is appropriate in the context of [its] more modest expectations for CBD office."

Goldman views Vornado, "as having a number of possible catalysts to drive growth, such as: reducing cash levels, selling or spinning portfolios that remain under-appreciated by the market (notably NYC street retail and Washington, DC), better articulating a long-term management succession plan, and identifying/quantifying high-return uses of capital within VNO's massive Penn Plaza portfolio."

However, the Goldman base case assumes "those arrows will remain in the quiver."

Bottom Line

Growth in FFO will drive higher office REIT valuations moving forward, not multiple expansions and cap rate compression for CBD office assets.

Burke warned investors, "What got you here won't get you there."

Investor Takeaway

Boston Properties is best positioned of the big three to deliver for investors between now and 2019; while SL Green's past outperformance was driven in large part by low cost floating rate debt and pursuing a logical strategy of being fully invested.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|