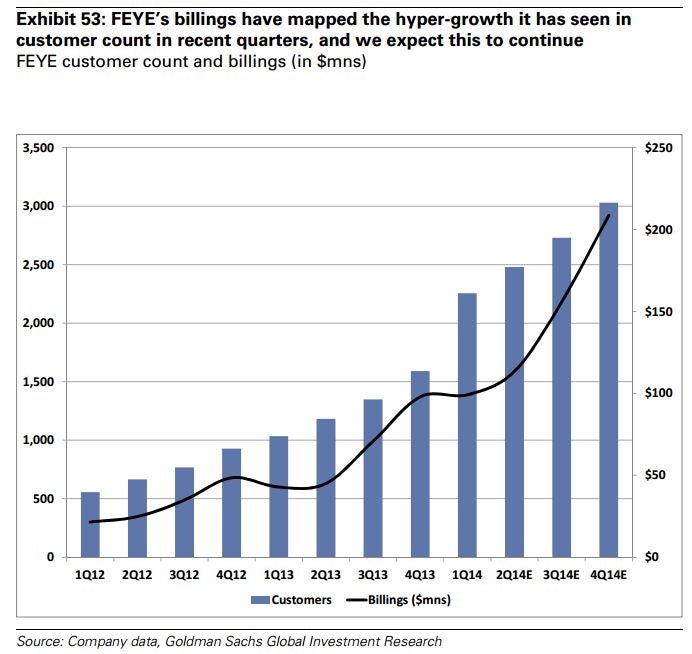

FireEye FEYE was highlighted in a security sector from Goldman Sachs GS on Wednesday. The cyber-threat defender was initiated with a Buy rating from Goldman with a price target of $42. The company is expected to benefit from much of the same environment as Palo Alto Networks PAWN. Specifically though FireEye’s ability to double its customer base in the past year while investing in Sales and Marketing marks a focus point for investors analyzing FireEye’s ability to capture market share in the global market.

Aside from increased attempts from global businesses to bolster cyber security measures, Goldman identifies “several growth tailwinds which should drive stock upside”. Those tailwinds include: “the continued prevalence of APTs and large-scale data breaches and customers’ subsequent desire to avoid them via newer technologies, as validated by our recent IT survey results, (2) a growing product pipeline and cross-selling opportunities via recently acquired Mandiant, which should re-accelerate growth in 2Q14, and (3) despite operating margins and FCF being significantly pressured during this hyper-growth phase, we expect FCF burn levels to trough this year, before an above consensus ramp in 2015“.

Companies are not able to proactively protect themselves with inhouse software as well as might be expected. Only 33 percent of businesses were able to detect breaches on their own, down from 37 percent in 2012 according to Mandiant, a cyber-security firm who hit the map with a report on China’s direct involvement with cyber espionage in 2013. Risk Based Security found that in 2013 over 70 percent of breaches came from outside the target business.

As cyber-security continues to be a major concern for globally businesses going forward, firms like FireEye may do so well on their own that an acquisition would eventually become unwarranted. If FireEye can ramp and integrate its sales force in the near-term and control the efficient of execution missteps, the company could succeed enough to become a staple on it’s own merit in the security sector.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.