CMA

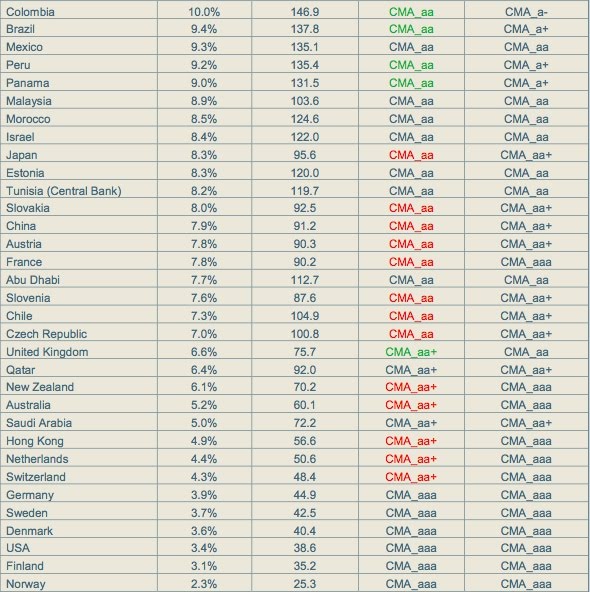

This list states the implied probability of default (CPD) of government debt, its CDS prices and ratings derived from these figures.

, a company monitoring Credit Default Swap (CDS) prices, has issued its latest quarterly report on government risk defaults. While Norway and Finland came out best again, the USA jumped to #3 from #10. All 3 are considered happy debtors by investors, who pay between 26 and 40 basis points (bp) for derivative default insurance with a 5-year maturity.

It is an entirely different affair at the other end of the list, where political uncertainty and inaction have added to the indebted countries' financial calamities.

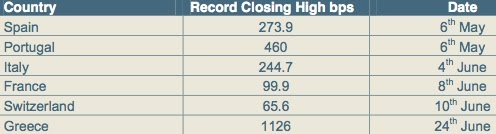

Venezuela's top position as worst government risk where insurance premiums range from 1,300 bp to 2,700 bp remains also unchanged. Attention correctly focused on the Eurozone and CEE countries which saw their position deteriorating most, the table below shows.

TABLE: Panicking investors drove Eurozone members debt insurance costs the highest in Q2 2010. Click to enlarge.

Find a complete list of global government - it is not sovereign - debt default risk after the jump.

Towards the end of the second quarter Greece temporarily overtook Venezuela as the sovereign with the highest default probability and has been the worst performer this quarter globally.

Many Eurozone sovereigns reached all time closing highs during this quarter:

This list states the implied probability of default (CPD) of government debt, its CDS prices and ratings derived from these figures.

Click to enlarge.You can download the whole report here.

Loading...

Loading...

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Posted In:

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in