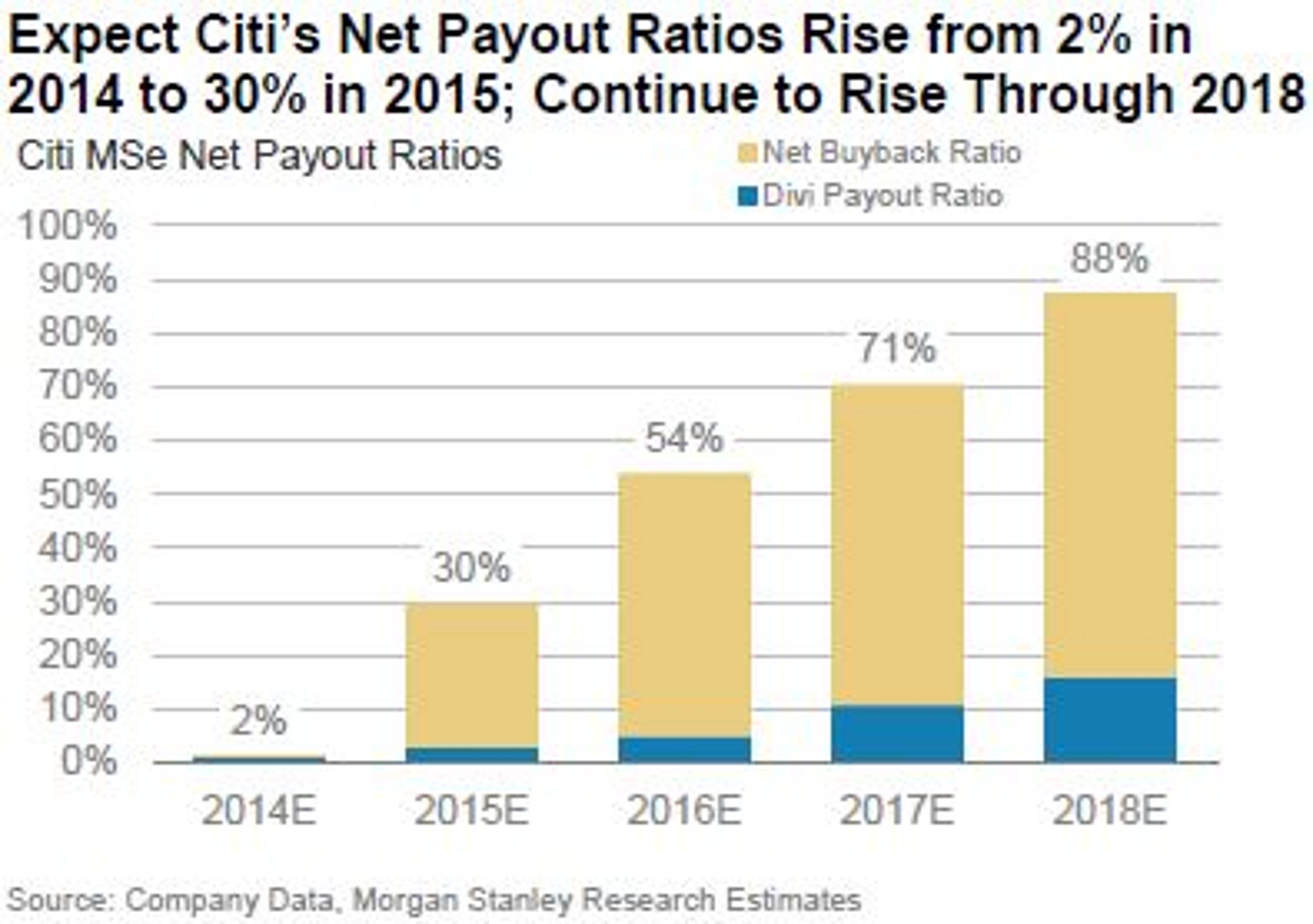

A recent Morgan Stanley report offered some insight into what analysts believe Citigroup Inc (NYSE: C)'s capital return plan will be in 2015. After an embarrassing rejection of its plan by the Federal Reserve in 2014, the analysis indicates Citigroup could be well-positioned to institute aggressive share buyback and dividend programs next year.

Analysts see four key reasons Citigroup should be free to return money to shareholders in 2015.

After a rocky 2014, Morgan Stanley analyst Betsy Graseck sees big things for the bank in 2015. “We expect a 4 cent dividend hike to 5 cents/quarter and $4.4 billion in buybacks in 2015," she said.

Morgan Stanley’s base case price target for Citigroup stock is $63, a more than 15 percent upside from current levels.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.