Bandera Partners Issues Letter to Luby's Stockholders

Bandera Partners LLC, a significant shareholder of Luby's Inc. LUB, announced that it has issued a public letter to Luby's stockholders. The full text of the letter follows.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20190103005646/en/

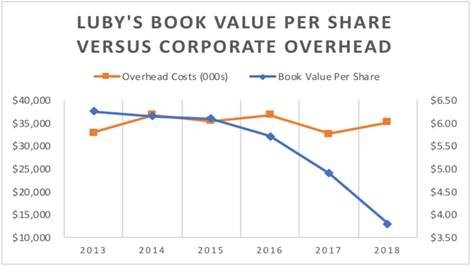

Luby's Book Value Per Share Versus Corporate Overhead (Graphic: Business Wire)

January 3, 2019

Dear Fellow Luby's Stockholders:

Bandera Partners owns approximately 9.8% of Luby's, Inc. ("Luby's" or the "Company") Common Stock, making us the largest stockholder other than Christopher and Harris Pappas, who together own 36.8%. We are dedicated to maximizing value for all Luby's stockholders, and we believe the only way to accomplish this is by infusing the Board of Directors with our highly qualified nominees, who will advocate for your interests as owners of the Company. THE OPPORTUNITY FOR CHANGE IS NOW!

Under the leadership of Christopher and Harris Pappas and the incumbent Board of Directors, Luby's has:

- Drastically underperformed its peers and the broader stock market. Luby's stock price has declined by a whopping 84% in the five years prior to our sending nomination notice to the Company in November 2018.

- Failed to sufficiently reduce its bloated overhead expenses, even as the Company's revenue and number of restaurants have shrunk.

- Rewarded the Board with $5.6 million in Director compensation since FY 2013.

- Recently, incurred $60 million of very expensive debt with an interest rate over 10% per year!

Even as Luby's stock has plummeted in value and stockholders have lost money, the Board of Directors has rewarded itself and management with extraordinarily high pay. Luby's top three executives, CEO Christopher Pappas, CFO Scott Gray (a former Pappas Restaurants employee), and former COO Peter Tropoli (whose stepfather serves on the Board of Directors), have been paid $12.7 million since FY 2013, including a staggering $2.4 million this past year while the company was floundering. Do you think spending $18.3 million on Board and management compensation since FY 2013, which is equal to over 50% of Luby's current market capitalization, was a good use of your capital?

DISASTROUS STOCK PERFORMANCE

For the five-year period leading up to November 15th, 2018, the day Bandera filed notice it was nominating directors to Luby's Board, Luby's stock was DOWN 84% while the S&P 500 was UP 65%, Darden Restaurants was UP 157%, Denny's was UP 144% and Cracker Barrel was UP 87%. Here is a table of Luby's performance, so you can draw your own conclusions about whether you would rather have our nominees or management's as four of the directors representing you for the next year.

| Share Price Performance | |||||||||||||||

| 1-Year | 2-Year | 3-Year | 5-Year | 10-Year | |||||||||||

| Cracker Barrel Old Country Store, Inc. | 14.7% | 21.9% | 46.9% | 87.3% | 1429.8% | ||||||||||

| Darden Restaurants, Inc. | 39.8% | 60.1% | 120.6% | 156.8% | 765.0% | ||||||||||

| Denny's Corporation | 35.4% | 39.6% | 75.2% | 143.7% | 993.5% | ||||||||||

| Average of Similar Competitors | 30.0% | 40.5% | 80.9% | 129.3% | 1062.8% | ||||||||||

| S&P 500 Index | 8.5% | 29.9% | 40.1% | 64.5% | 263.7% | ||||||||||

| Luby's, Inc. | -52.4% | -70.8% | -74.8% | -83.9% | -69.1% | ||||||||||

|

Source: Bloomberg |

|||||||||||||||

TIME IS RUNNING OUT

We strongly believe that time is running out, and that immediate change is needed to prevent even more value destruction for stockholders. Luby's has lost $73 million over the last five years, and book value has plummeted as the Company has sold real estate and incurred debt. Despite steep losses and a shrinking restaurant base, Luby's has not reduced its bloated overhead costs. Corporate overhead GREW from $33 million in FY 2013 to $35 million last year. Below is a chart showing Luby's decline in book value versus corporate overhead costs.

Stockholders have a right to be furious that a shrinking company generating losses is not seriously cutting costs. In October, Luby's replaced its Chief Operating Officer, Peter Tropoli. Instead of parting ways, Luby's transitioned Tropoli to a lesser role, General Counsel, with a hefty $350,000 per year salary. According to Luby's website and SEC filings, the Company already employed two senior legal officers in 2018 and leased an executive suite in Massachusetts for "additional legal personnel." How is this appropriate for a $36 million market capitalization company that is selling off its assets to keep the business afloat!? If our slate of qualified nominees is elected, one of our first actions will be to ask the Board of Directors to lead by example by slashing its own Board fees by over 50%.

SHRINKING REAL ESTATE VALUE

Luby's has significantly underperformed its restaurant industry peers despite owning most of its operating properties. Public Texas county appraisals value Luby's properties at almost $160 million, or about $3.94 per share net of all debt. But under the direction and supervision of the incumbent Board, Luby's continues to liquidate its valuable real estate to fund investments into its underperforming business. Since FY 2008, capital expenditures have totaled $235 million dollars. The return on this investment has been atrocious, and to pay down the debt Luby's has accumulated in the process, the company has sold $88 million in assets since FY 2008. The Company's portfolio of properties is the most valuable asset stockholders own. Under the incumbent Board's leadership, it is disappearing.

Each of your Luby's shares represents $3.94 in coveted Texas real estate. But as of the close of trading November 15th, the day we notified the company we were nominating a slate of directors, the market valued Luby's shares at only $1.20. In other words, the market estimated that in the hands of the Pappases and the incumbent Board of Directors, Luby's $3.94 per share in real estate was worth only $1.20. We believe the only way to close this valuation gap is to remove the Pappases from the Board of Directors and infuse it with new members.

LUBY'S ONLY PLAN: MORE OF THE SAME

On December 24th, 2018, Luby's sent a letter to stockholders explaining that it is aggressively executing a plan to increase profitability. We have heard this story before!

In 2007, when Luby's stock price was $10.25: "Your Board and management team have a strategic growth plan for Luby's designed to create profitable growth and long-term shareholder value."

In 2008, when Luby's stock price was $7.00: "We remain confident that our long-term strategic plan . . . will enhance shareholder value."

In 2009, when Luby's stock price was $4.12: "We believe that the focused execution of our near-term and long-term plans will enhance shareholder value."

2010: "The actions we've taken better position the Company for enhanced long-term shareholder value."

2011: "We have plans in place to grow each of our brands . . . We see opportunities to improve shareholder value as we grow our brands."

2012: "We have positioned the company for new unit growth . . . Our goal remains to enhance shareholder value by growing sales, operating cash flow and profitability."

2013: "Our future is promising . . . we are working hard to drive increased customer traffic and sales while managing costs to drive profitability and enhance shareholder value."

2014: "With a laser focus on executing at the highest levels . . . and prudently investing in our brands, we will enhance shareholder value."

2015: "We believe our company and brand portfolio . . . is well positioned for sustainable growth and enhanced shareholder value going forward."

2016: "We believe that we are well-positioned to enhance shareholder value over the long term."

2017: "We believe these crucial aspects of our business to achieve operational excellence of our brands will lead to growth in profitability and enhanced shareholder value."

Year after painful year, Luby's Board tells you that it is on the cusp of turning around the business with its strategic plan. These plans have NEVER created value for stockholders! Instead, Luby's is forced to sell valuable real estate to fund the business. Luby's promise in its recent proxy solicitation letter to "invest appropriately in the right assets with better return characteristics to ultimately improve our overall financial results," should send shudders down the spine of every stockholder. The Pappas brothers and the incumbent Board have already invested hundreds of millions of dollars into Luby's with disastrous "return characteristics." Why should stockholders expect anything but a similar result?

Luby's letter to you in December 2018: "We are already in the process of monetizing underperforming restaurant locations, which will allow us to strengthen our core operations."

2017: "Proceeds from the closure and sale of excess properties can be redeployed into future investments with superior return characteristics."

2016: "We are committed to making capital investments with suitable return characteristics"

2009: "After thoroughly evaluating each of our stores' near and long-term potential, we are closing 25 stores. This strategic initiative is designed to stabilize and strengthen our core operations."

Luby's incumbent Board states that by continuing management's strategy of "re-directing funds" into Luby's and Fuddruckers, the two restaurant concepts can thrive. We have already witnessed millions of dollars generated from property sales get re-directed into Luby's and Fuddruckers. This capital has been lost forever. Luby's accuses Bandera of being liquidators, but the incumbent board has been slowly liquidating the Company for years, with no benefit accruing to you and other owners of the Company. The only thing the Pappas brothers' "aggressive plan" offers is more of the same.

LUBY'S NEEDS IMPROVED, MORE INDEPENDENT OVERSIGHT

We have assembled a slate of highly qualified nominees to bring new accountability to Luby's Board of Directors, and to help drive a capital allocation strategy that can create shareholder value rather than continue to destroy it year after year after year. Our slate of nominees includes:

Senator Phil Gramm – An economics professor at Texas A&M before serving 24 years in the US Congress. Since leaving public service he has worked in investment banking and private equity.

Stacy Hock – An accomplished philanthropist, policy activist, and business owner. She is a Texas gubernatorial appointee as Vice Chair of the Texas Commission on Next Generation Assessments and Accountability.

Savneet Singh – An entrepreneur who has launched various finance, software and real estate businesses. He is Interim CEO and President of Par Technology, a $320 million public company that is one of the world's largest providers of restaurant point-of-sale technology.

Jeff Gramm – A fund manager who has served on five public company boards of directors, including a restaurant company, Morgan's Foods, that created tremendous shareholder value through an opportunistic sale of the business.

These independent-minded leaders are the perfect group of directors to bring accountability and change to an ineffective Board that badly needs refreshment. Luby's December 24th letter to stockholders not only stated that our nominees were not qualified to justify replacing any of the Company's underperforming directors, it questioned whether any of our nominees were "suited to sit on any public company board." Do you want to take advice from Luby's incumbent directors, who have destroyed millions of dollars of shareholder value, about who is fit to serve on the Board of Directors? This is your opportunity to decide for yourself. If we are elected, our first and only priority will be creating shareholder value for you.

Our GOLD proxy targets four Luby's directors for removal: Christopher Pappas, Harris Pappas, Pappas Restaurants General Counsel Frank Markantonis, and Luby's Chairman Gaspir Mir, III. We believe removing the Pappas Restaurants affiliated directors, as well as the incumbent Chairman, will best position the new Board for success and a fresh start in evaluating strategic options for Luby's.

EVERY SINGLE VOTE COUNTS AND WE ABSOLUTELY NEED YOURS

Christopher and Harris Pappas, and the incumbent Luby's Board own more than 38% of the outstanding stock. In order for us to overhaul Luby's underperforming Board, we need your vote. The stakes here are high, and Luby's is going to tremendous lengths to ensure that the Pappas brothers do not suffer the humiliation of being voted off their own Board despite owning such a huge percentage of the stock.

Luby's has already engaged in nasty personal attacks to distract you from the incumbent Board's terrible performance as stewards of your capital. Our message is simple. Bandera was a supportive Luby's shareholder for over ten years. We responsibly engaged with the company to try to improve the Board of Directors, and to avoid a costly and distracting proxy fight. When the Company refused to engage in substantive negotiations with us, we decided to take this important decision to you, the owners of the Company. If you are as fed up as we are with the performance of Luby's and its incumbent Board of Directors, please force change by voting the GOLD proxy immediately, even if you previously gave your vote to the Company.

About Bandera Partners

Bandera Partners is a value-oriented hedge fund based in New York.

View source version on businesswire.com: https://www.businesswire.com/news/home/20190103005646/en/

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.