Activist investors say in a letter to the Board of Directors that specialty retailer's performance lags peers, company requires "dramatic change"

BEVERLY HILLS, Calif., Feb. 27, 2018 /PRNewswire/ -- Legion Partners, LLC and 4010 Partners, LP today released a letter calling on the Board of Directors of Genesco, Inc. GCO to implement a series of immediate reforms and explore strategic alternatives.

Together, Legion and 4010 own more than 5% of the specialty retailer's outstanding shares. The activist investors claim Genesco – whose brands include Johnston & Murphy, Lids, Schuh and Journeys – underperform its peer group and that "good-faith efforts to work constructively with the Company to find a better solution for shareholders have not been taken seriously."

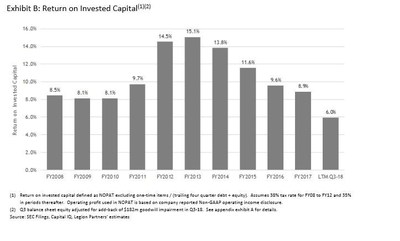

"Dramatic change is required at Genesco," said Legion Managing Director Christopher S. Kiper. "Genesco's return on invested capital has declined from 15% in FY2013 to 6% in the most recent 12-month period. Despite the precipitous deterioration in returns and underperformance of the Company's stock price, we have seen little willingness to re-think the status quo under current leadership."

Specifically, Legion and 4010 believe the Genesco board should:

- Expand its strategic review to complete an objective evaluation of all strategic alternatives;

- Perform a comprehensive operational review;

- Reform its corporate governance and implement changes to long-term incentive plans to better align management with shareholders.

The full text of the letter follows:

February 26, 2017

Sent via FedEx and Email

Board of Directors

Genesco, Inc.

1415 Murfreesboro Road

Nashville, TN 37217

Members of the Board:

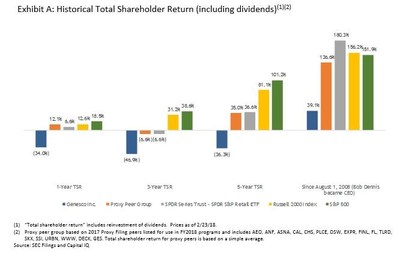

As holders of 5.3% of the outstanding shares of Genesco, Inc. ("Genesco" or the "Company"), Legion Partners LLC and 4010 Partners, LP (and affiliates, collectively "we" or the "Group") are writing to express our disappointment with the Company's February 13, 2018 release announcing the conclusion of a strategic review which resulted in a decision to sell the Lids Sports Group. Although we agree that Lids does not fit well with Genesco's other businesses and should ultimately be separated, we believe it is incumbent upon the board to complete a more comprehensive evaluation of all strategic alternatives to enhance shareholder value given the poor track record of execution by management and the long-term underperformance of the Company's share price.1

We are deeply concerned by what appears to be a rushed and superficial response to our suggestion that the board conduct a thorough strategic review. The board's decision to initiate a sale of Lids, its worst performing division, appears to be a defensive measure designed to divert attention from other potentially more attractive options that must be evaluated in a rigorous strategic review, including price discovery for all business units. There are multiple alternatives to improve long-term shareholder value, but the status quo of continuing to operate this disparate set of assets with such a poor record of value creation is unacceptable.

Based on our conversations with management and external investment bankers, Johnston & Murphy ("J&M") and Schuh offer limited synergy with the core Journey's operations and would attract broad strategic interest at premium valuations compared to the value implied by Genesco's current trading price. In addition, we believe that the opportunity for Journeys, J&M, Lids and Schuh to optimize their growth strategies and improve profitability would be enhanced through separate ownership. We are also concerned by the timing of the decision to sell Lids given its poor current performance. We believe there are several initiatives that can be readily implemented at Lids to improve the business before marketing it and that this would be a more prudent course of action to fully realize Lids' value.

Dramatic change is required at Genesco. Genesco's return on invested capital has declined from 15% in FY2013 to 6% in the most recent 12 month period.2 Despite the precipitous deterioration in returns and underperformance of the Company's stock price3, we have seen little willingness to re-think the status quo under current leadership. We believe the best path forward for shareholders includes the following actions:

(1) The board should immediately expand the strategic review to complete an objective evaluation of all strategic alternatives. Our analysis suggests that Genesco trades at a significant discount to the value of its individual assets. Each segment has a unique growth, return and risk profile which is not optimized under the current structure. Given these characteristics and the opportunity to substantially increase shareholder value through a separation of certain businesses, it leads us to the conclusion that the status quo is not a responsible course of action. As a result, several units should be evaluated for sale, with the understanding that quality assets are likely most transactable and have the potential to be most accretive to shareholder value;

(2) Management should announce specific targeted actions to improve return on invested capital, including a comprehensive cost reduction program, the closure of a significant number of unproductive stores, initiatives to improve inventory turnover at all divisions, a commitment to further reduce capital spending, and a revised capital allocation framework which demonstrates better discipline and prioritizes return of cash flow to shareholders over additional M&A or brick and mortar investments; and,

(3) The board should institute best-in-class corporate governance and implement changes to long-term incentive plans to better align management with shareholders. The roles of Chairman and CEO should be immediately separated to ensure an arms-length relationship between fiduciaries of shareholders' interests and management. In addition, revisions to incentive programs should be made to focus the reward to management on enhancing ROIC, pursuing divestitures that are accretive to shareholder value, and increasing long-term value for shareholders.

Unfortunately, the board's recent actions make it clear that our good-faith efforts to work constructively with the Company to find a better solution for shareholders have not been taken seriously. We find it unlikely that the Company would have been able to conclude a full review of strategic alternatives in less than four weeks since our Group met with management on January 19, 2018 and suggested initiating such a process. We also do not believe that the decision to sell Lids at this time could possibly be a logical first step to a full and complete strategic review process. We view the board's response as an effort to preserve the status quo and keep the Company's retail empire intact, rather than a thoughtful evaluation of the actions that would result in the best outcome for shareholders.

We'd like to schedule a call as soon as possible with Genesco's Lead Independent Director James Bradford and any subset of the independent board members to discuss our analysis and recommendations in greater detail. We remain open to working together productively toward substantially improving shareholder value in order to avoid the significant corporate expense and distraction created by a proxy fight.

Sincerely,

/s/ Christopher S. Kiper /s/ Ted White

Enclosures

cc: Steve Wolosky, Olshan Frome Wolosky LLP

1 See Exhibit A: Genesco's Total Shareholder Return has underperformed the proxy peer set (used for FY2018 as disclosed in the 2017 Proxy Filing) over 1-year, 3-year, and 5-year time periods.

2 See Exhibit B: Historical return on invested capital since Bob Dennis became CEO.

3 See Exhibit A: Since Bob Dennis became CEO on August 1, 2008, Genesco's Total Shareholder Return was 39.1% as compared to the proxy peer set (used for FY2018 as disclosed in the 2017 Proxy Filing) of 136.6%.

(1)(2)")

(2)")

View original content with multimedia:http://www.prnewswire.com/news-releases/legion-partners-and-4010-partners-call-on-genesco-board-to-examine-strategic-alternatives-implement-reforms-300604552.html

SOURCE Legion Partners, LLC

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.