Semiconductors are in most things you use on a daily basis. They’re in your smartphone, your blender, your thermostat… even those silly greeting cards that play music when you open them. If they aren’t in the things you use, they were in the things that made the things you use.

That’s why we’ve been following the semiconductor sector very closely. Specifically, semiconductors are a leading economic indicator strongly correlated to production and factory orders. That correlation continues to increase over time.

What makes semis great leading indicators? Unique among other factory components, semiconductors’ key characteristics include:

Short shelf life: Rapid obsolescence forces a made-to-order environment which in turn creates incredible downstream visibility to end-user demand.

Concentrated production: Strong visibility to regional and industrial trends because of the oligopolistic nature of the business.

Upstream role in production: The semiconductor life cycle begins months before final production.

Universal common denominator: If a semiconductor isn’t in it, a semiconductor is in the machine making it.

The Post-China Boom Macro Economy

With China’s increases in spending on communications infrastructure, semiconductors have been riding a wave. As billions of dollars are put to work to support networking, billions have also been made in smartphone and tablet sales.

However, semiconductors want to avoid the boom/bust cycle hitting the other commodity beneficiaries of China’s infrastructure investments. Notable are the 50 percent+ drop in iron ore and the 20 percent drop in copper prices in the last year.

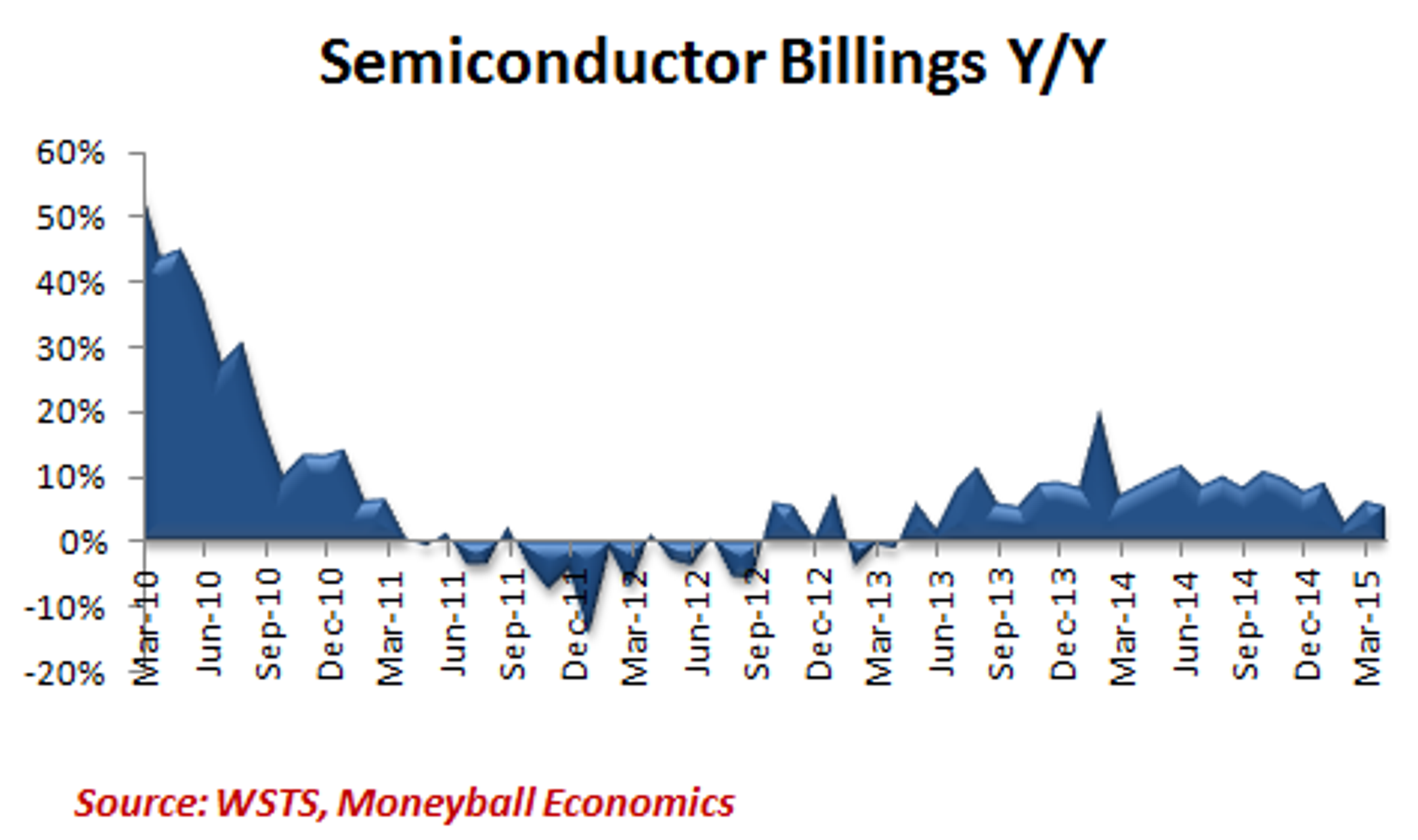

Demand for silicon has never been better…

…but growth has already begun to slow.

TSMC is one of the largest buyers of those silicon wafers. Nominal billings are strong, although they have been plateauing over the last six months. In fact, growth has fallen back to 1-year levels.

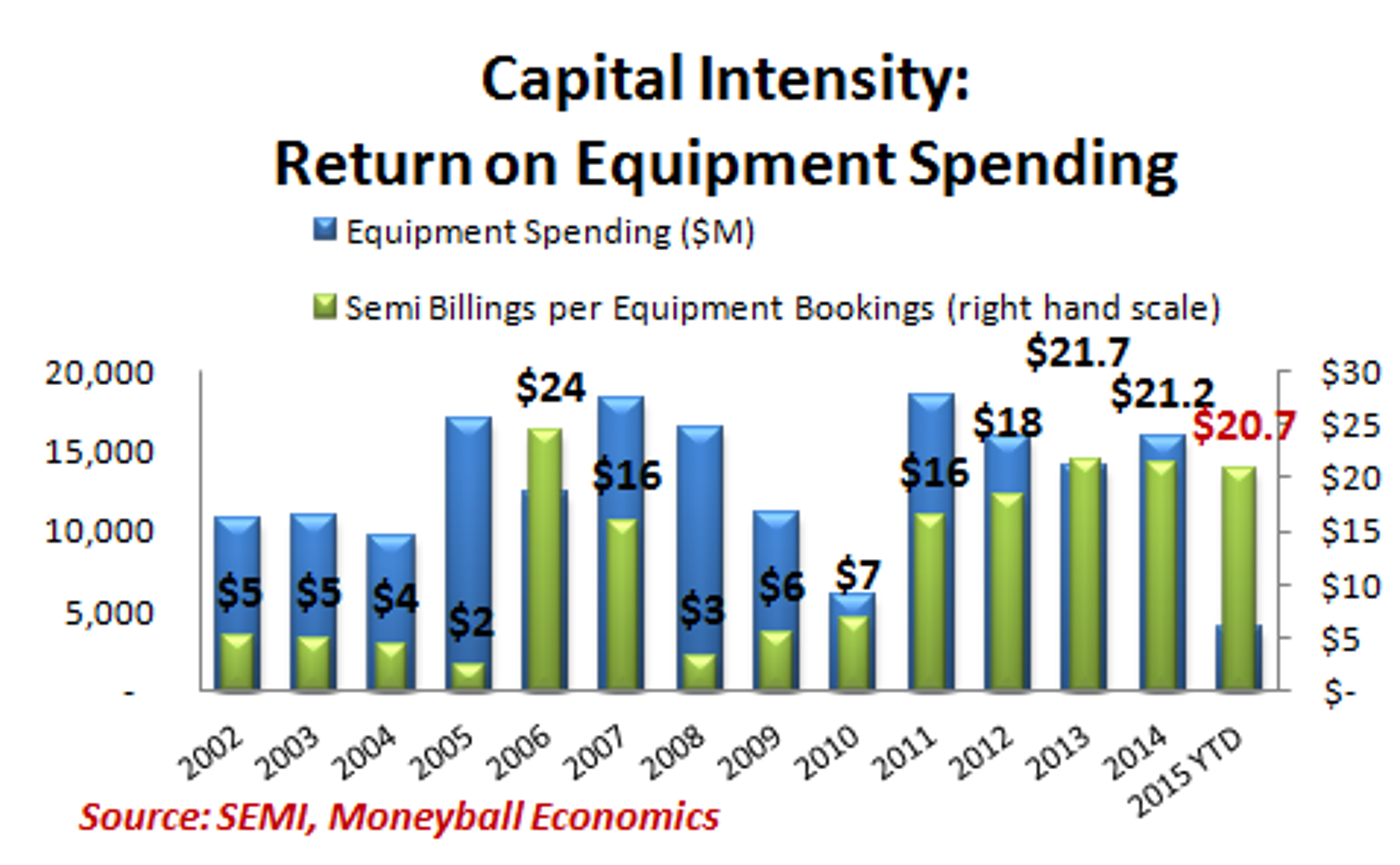

The falling microchip revenues are pushing down equipment spending.

The returns on equipment investment (capital intensity) are slipping and the reaction has been swift. In the last month, announced CAPEX cuts include:

Intel cut $1.3B

TSMC cut $1B

Spending is pulling back pretty sharply. It’s on track to grow 4 percent in 2015. That’s a big drop from 12 percent in 2014. The qualities that make semiconductors a leading economic indicator are starting to surface.

Capital intensity levels aren’t dropping enough to move the investment dial more substantially… yet. The current dip is very slight: from 2014’s $21.2M to the current $20.7M. Thus, producers are responding to a downshift in future demand, which are expected to slow and even slip by fine tuning their own orders.

This is every factory’s way of avoiding the bust side of the cycle, and that’s an important red flag: semiconductor companies are planning for slower growth, which can add to the slowdown if other manufacturers arrive at the same expectation.

Canary in the Coalmine: Manufacturing and Demand Implications

A slowdown in semiconductor demand is signaling a 2H slowdown in business spending and factory investments.

Slowing Chinese business and consumer demand appears to be at the center of the slowdown and it is dragging the EU down with it.

There are variations here, based on region:

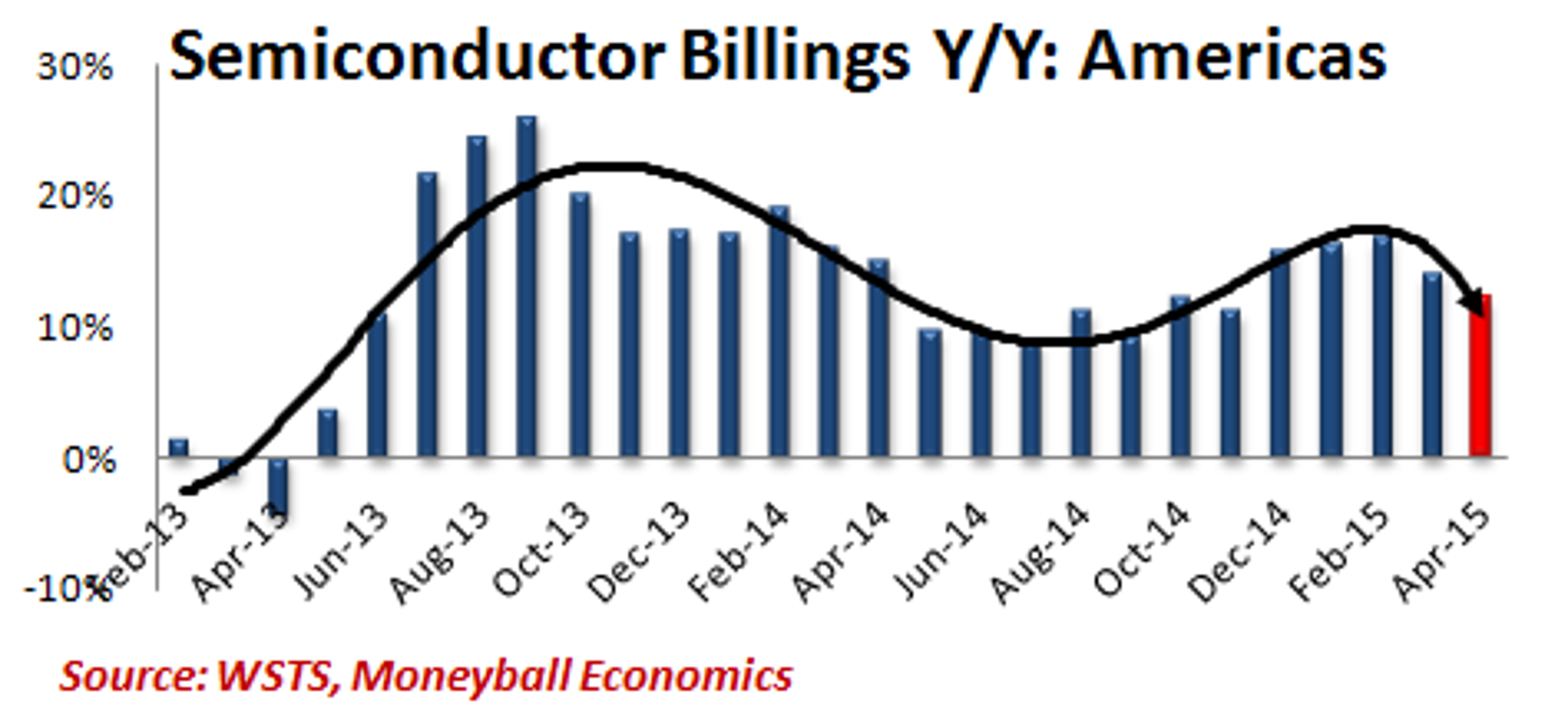

The Americas remain relatively strong, although some pullback is underway:

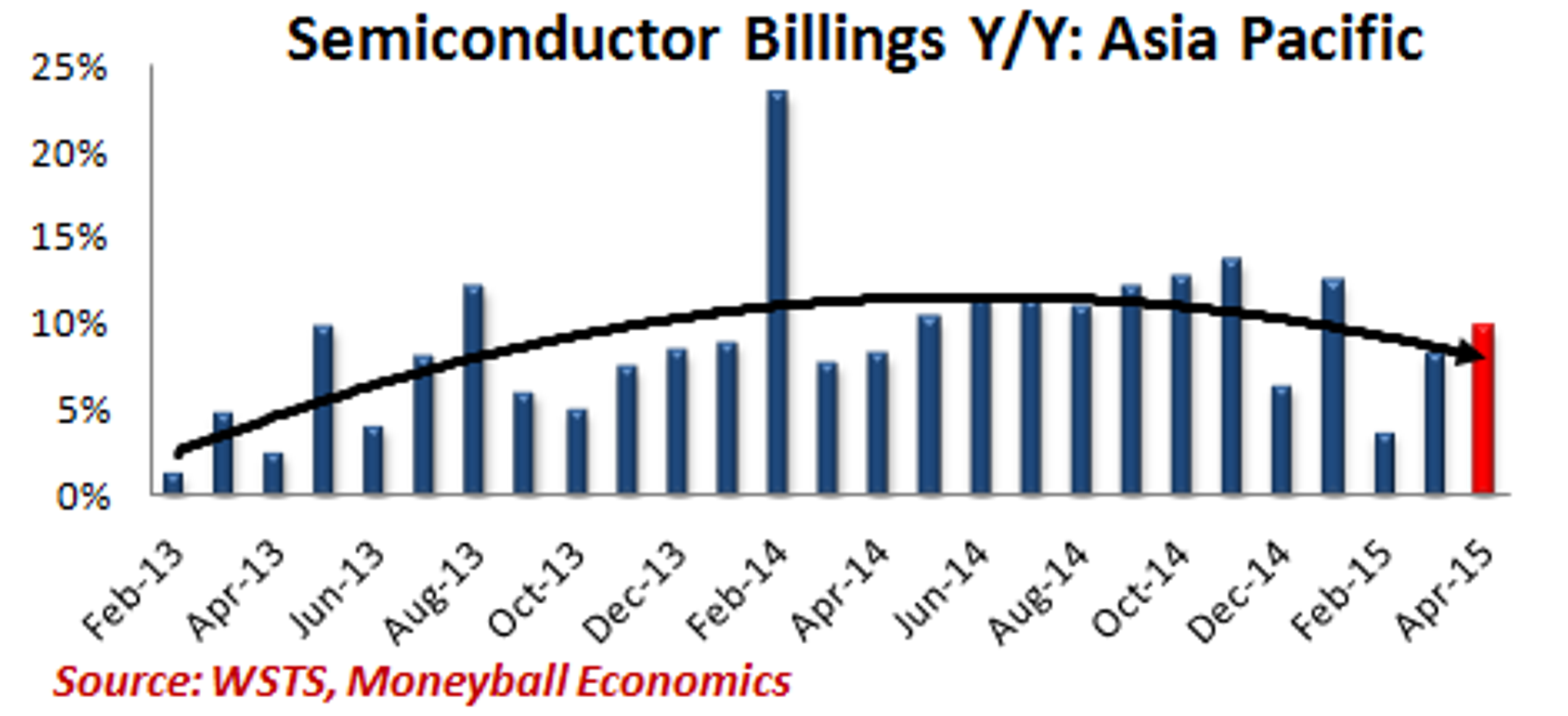

Asia Pacific (China) is slowing a bit:

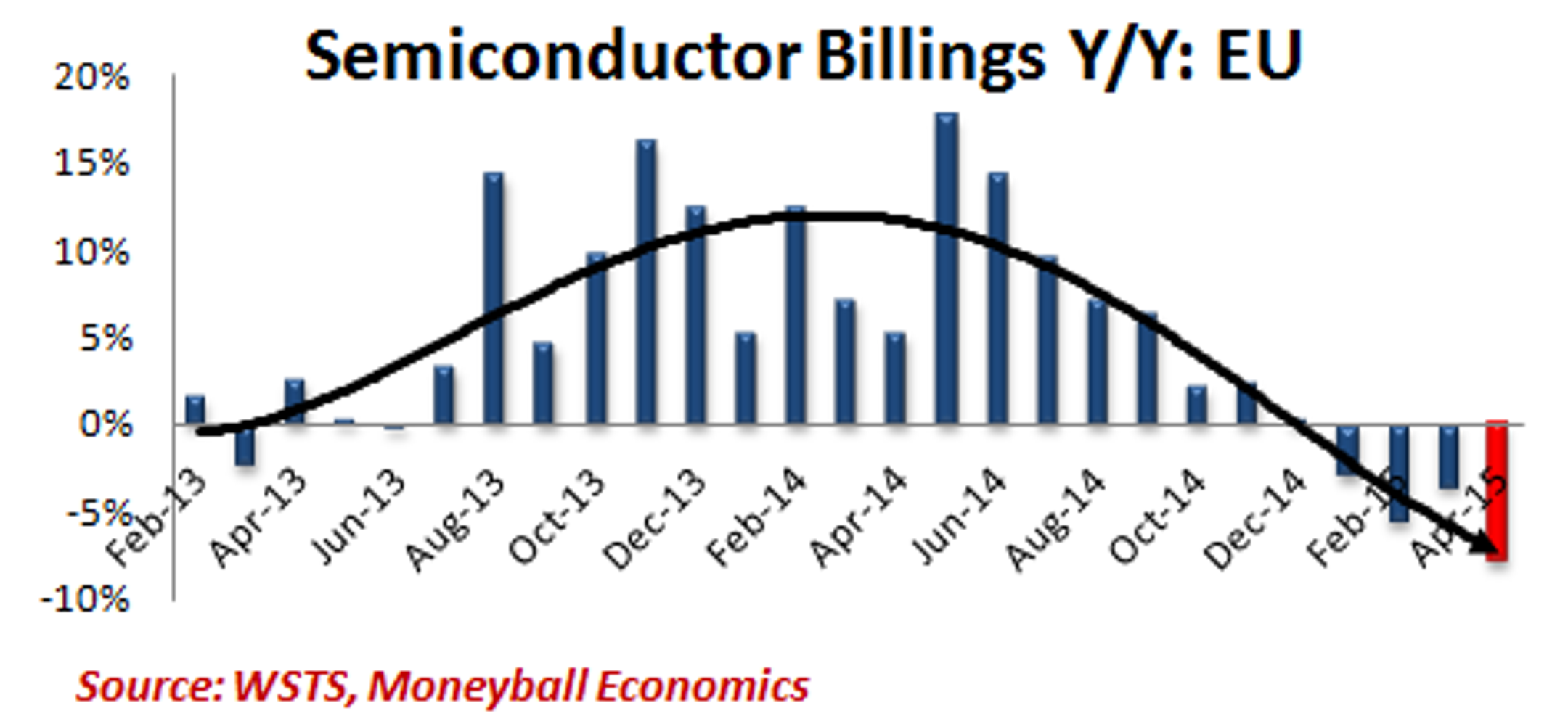

EU is flat-out recessionary:

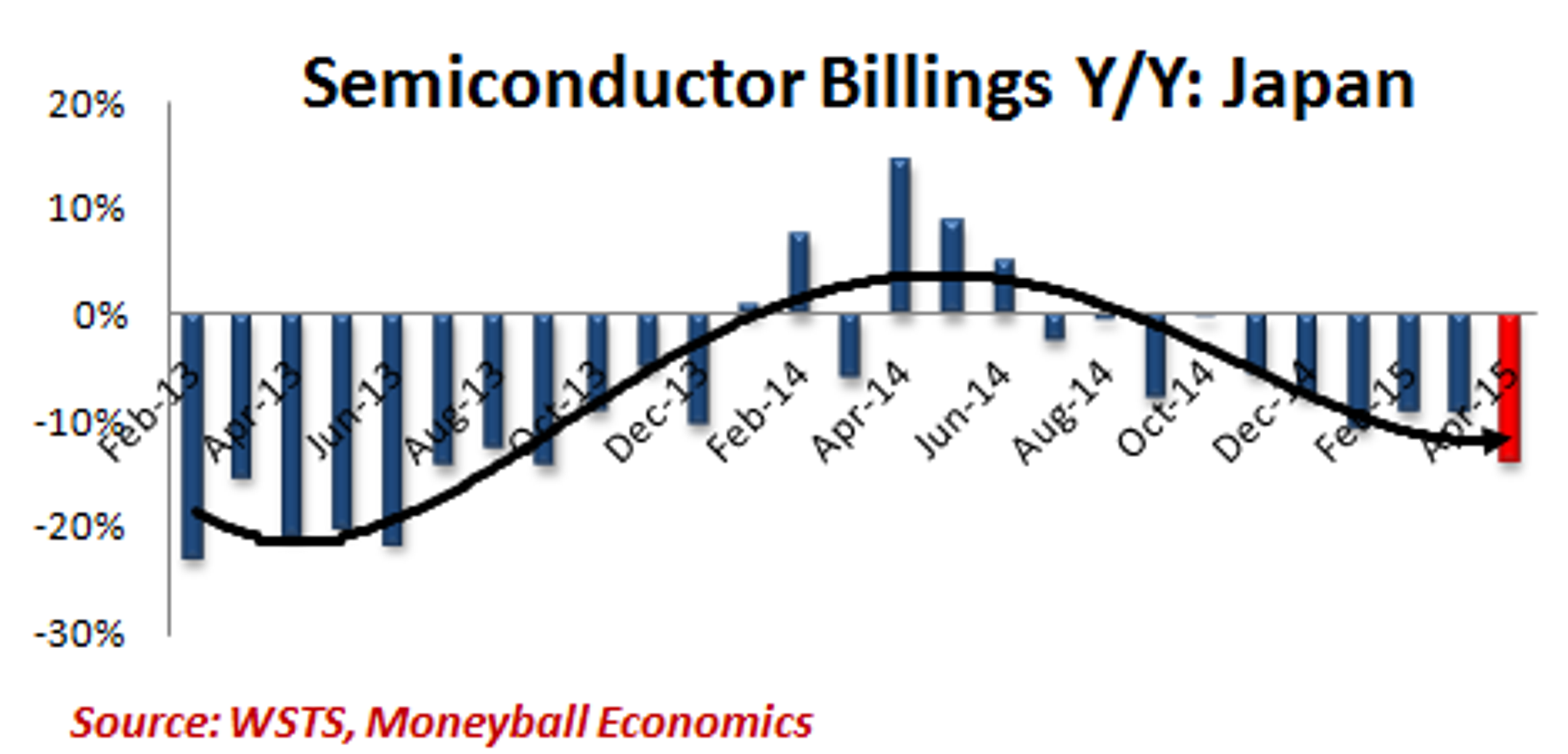

Japan is also recessionary.

For exporting countries, semiconductor consumption is a litmus test for economic growth. The EU and Japan don’t show any growth in consumption. In fact, they have been contracting for months.

Moreover, the slowing China growth evident in the Asia-Pacific billings is the likely culprit behind the EU’s semiconductor slowdown. As a proxy for their economies, this data is saying that the EU will only be as strong as China’s growth, which also looks a bit softer these days.

Expect More M&A to Come as Sales Flatten

The market is peaking, as we’ve shown. Top-line growth is slowing and CAPEX budgets are either being cut or held flat.

Meanwhile, too much cash sits there unused. The universal theme in the last round of earnings conference calls in the semiconductor sector was what to do with cash on the sidelines. Since tech stocks rarely do dividends, analysts focused on buybacks and M&A.

The responses were uniformly vague but definitely not negative. That is, M&A was referenced as a direction ‘when it made sense’, and buyback specifics were not called out. The consensus was that the cash wouldn’t be sitting around for long.

Some recent M&A activity is synergistic. For example, Intel’s only growth sector is in the data center but its microchips for those servers are energy intensive. A play for Altera Corporation ALTR (or Xilinx, Inc. XLNX) would be a way to tackle that problem. In another case, NXP Semiconductors NV NXPI's acquisition of Freescale makes sense as it continues to dominate the auto market.

Broadcom Corporation BRCM very recent merger with Avago Technologies Ltd AVGO is a great example of consolidation to show growth and keep that share price up. Broadcom is cashing out at the top. The company depends on Telecom spending, and growth is slowing. That’s partly because of US telecom mergers which lead to redundant network gear, and partly because the big infrastructure opportunities are done. China is in the middle of a major roll-out, but when it ends, there aren’t many profitable opportunities for Broadcom on the horizon.

Broadcom is on the way to being another Cisco Systems, Inc. CSCO: servicing telecom companies with a large installed base of legacy infrastructure investments and dependent on upgrade cycles and organic growth.

Now would be a good time to exit Broadcom, before the inevitable slow growth hits the company’s numbers and stock price. Additionally, with interest rates poised to rise, it’s a good time for Avago to borrow.

To some extent the Avago/Broadcom deal is a footnote to the end of the smartphone product cycle.

For perspective, the iPhone debuted 8 years ago – an eon in the high tech world. Broadcom has been central to the wireless mobility infrastructure that had to be built out to enable smartphones (and tablets). As that expansion slows, so too does Broadcom’s growth.

As a macro signal, the Broadcom exit points to the coming lull in top line growth for high tech companies specifically and for producers in general. It also says that stock prices have room to run as share buybacks propel stock prices higher. And then…the ammunition ends.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.