POULSBO, Wash., Aug. 8, 2016 /PRNewswire/ -- Pope Resources POPE reported net income attributable to unitholders of $436,000, or $0.09 per ownership unit, on revenue of $12.7 million for the quarter ended June 30, 2016. This compares to net income attributable to unitholders of $289,000, or $0.06 per ownership unit, on revenue of $13.9 million for the comparable period in 2015.

Net loss attributable to unitholders for the six months ended June 30, 2016 totaled $599,000, or $0.15 per ownership unit, on revenue of $23.8 million. For the six months ended June 30, 2015 the Partnership reported net income attributable to unitholders of $8.1 million, or $1.87 per ownership unit, on revenue of $40.8 million.

Cash used in operations for the quarter ended June 30, 2016 was $2.3 million, compared to cash provided by operations of $3.1 million for the second quarter of 2015. For the six months ended June 30, 2016, cash used in operations was $4.3 million, compared to cash provided by operations of $12.2 million in 2015.

"Our overall average log price realizations over the last several quarters have been fairly narrowly range-bound," said Tom Ringo, President and CEO, "with quarter-to-quarter variability in results for that business largely being a function of harvest volume fluctuations. More notably, in the second quarter of 2016 we invested $4.8 million of operating cash flow in our Harbor Hill residential project as we make preparations for the sale of a significant number of those lots later this year."

"Subsequent to the end of the second quarter, we closed on the acquisition of 7,324 acres of highly-productive, well-stocked timberlands in Pierce County, Washington for $31.9 million. This acquisition, which was 100% debt-financed, will increase the annual sustainable harvest on Partnership-only holdings by 8%, from 48 to 52 million board feet (MMBF). We expect the acquisition to provide net cash in excess of debt service of approximately $900,000 over the remainder of the year and to continue to be cash-accretive over the near-term. With the recent conclusion of Fund III's drawdown period and the initial close of Fund IV not expected until later this year, the Partnership was in a unique position to acquire its first significant timberland holding in a number of years."

Second quarter highlights

- Harvest volume was 20.9 MMBF in Q2 2016 compared to 15.1 MMBF in Q2 2015, a 38% increase. Harvest volume for the first six months of 2016 was 36.6 MMBF compared to 39.6 MMBF for 2015, an 8% decrease. These harvest volume figures do not include timber deed sales of 0.6 MMBF in Q1 2015 sold by ORM Timber Fund III. The harvest volume and log price realization metrics cited below also exclude these timber deed sales.

- Average realized log price per thousand board feet (MBF) was $563 in Q2 2016 compared to $562 per MBF in Q2 2015. For the first six months of 2016, the average realized log price was $575 per MBF compared to $591 per MBF for 2015, a 3% decrease.

- As a percentage of total harvest, volume sold to export markets in Q2 2016 increased only slightly to 15% from 14% in Q2 2015, while the mix of volume sold to domestic markets was 66% in Q2 2016 compared to 68% in Q2 2015. For the first six months of 2016, the relative percentages of volume sold to export and domestic markets were 17% and 63%, respectively, compared to 17% and 61%, respectively, in 2015. Hardwood, cedar and pulpwood log sales make up the balance of harvest volume.

- The Partnership acquired 287 acres of timberland during Q2 2016 for $1.1 million.

Second quarter and year-to-date operating results

Fee Timber:

Fee Timber operating income for Q2 2016 was $3.0 million, compared to $1.6 million for Q2 2015. In the current quarter, a 38% increase in harvest volume was primarily responsible for the increase in operating income as log prices declined only slightly.

Fee Timber operating income for the first six months of 2016 was $5.5 million compared to $6.5 million in 2015. Year-to-date declines from 2015 to 2016 in both harvest volume and average realized log prices (8% and 3%, respectively) were the major factors contributing to the lower segment operating income in 2016, along with a decrease in timber deed sales.

Driven by a strong U.S. dollar and expiration of the Softwood Lumber Agreement last October, British Columbia exports of softwood lumber to the U.S. in 2016 have increased 36% compared to 2015. This influx of Canadian lumber has kept lumber prices, and in turn, log prices in check relative to last year.

Timberland Management:

Operating losses incurred by this segment for Q2 2016 and Q2 2015 totaled $603,000 and $785,000, respectively, after eliminating revenue earned from managing the Funds of $788,000 and $767,000 of management fee revenue for Q2 2016 and Q2 2015, respectively.

Operating losses incurred by this segment for first six months of 2016 and 2015 totaled $1.3 million and $1.5 million, respectively, after eliminating management fees earned from the Funds of $1.6 million for each of the first six months of 2016 and 2015.

Real Estate:

Our Real Estate segment posted an operating loss of $1.2 million for Q2 2016 compared to operating income of $575,000 for Q2 2015. There were no land sales in the second quarter of 2016, whereas in Q2 2015 we closed on the sale of 33 residential lots from our Harbor Hill development for $3.3 million and a 175-acre conservation land sale for $920,000.

For the first six months of 2016, the Real Estate segment reported an operating loss of $2.2 million, having sold only nine single-family residential lots from our Harbor Hill development. This compares to 2015 operating income of $5.7 million in 2015, driven primarily by the sale of 75 residential lots from Harbor Hill for $9.0 million and on conservation land and easement sales covering 3,861 acres for $6.0 million.

General & Administrative (G&A):

G&A expenses for Q2 2016 and 2015 were $1.1 million and $1.2 million, respectively. For the first six months of 2016 and 2015, G&A expenses were $2.7 million and $2.4 million, respectively. The increase in 2016 is due primarily to being fully staffed relative to the prior year.

Timberland acquisition

On July 22, 2016, we closed on a 7,324-acre timberland acquisition from a client of Hancock Timber Resource Group consisting of 6,746 owned acres and a timber deed on 578 acres that expires in 2051. The acquisition contains 17.6 MMBF of merchantable inventory, including 3.4 MMBF from acres in the timber deed. The merchantable inventory is comprised of 55% Douglas-fir and 34% whitewoods, with the remainder spread across western red cedar, red alder, and other hardwood species.

The acquisition brings total Partnership timberland to 119,000 acres, a 7% increase, with all these acres located in Washington. The acquisition also represents a 6% increase in the Partnership's merchantable volume, boosting the total to 316 MMBF.

New financing

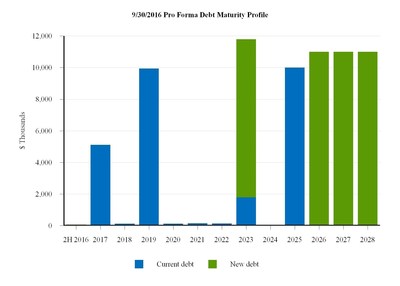

The timberland acquisition was financed with a new $32.0 million credit facility issued under our existing master loan agreement with Northwest Farm Credit Services (NWFCS) consisting of multiple balloon maturities: $10 million in 2023, $11.0 million in 2026, and $11.0 million in 2028. The first maturity is variable-rate debt while the latter two are fixed-rate. The three tranches carry a weighted average interest rate of 2.79%, net of patronage. The debt covenants of the master loan agreement were adjusted as well to provide more operating flexibility.

The Partnership has also entered into a second new credit facility issued under the master loan agreement with NWFCS to borrow up to $21.0 million. We expect to borrow $11.0 million on this facility in August to pay down the Partnership's operating line of credit (LOC) so that the LOC's full capacity is available to fund either Real Estate lot development, Port Gamble environmental remediation expenditures, or other liquidity needs. The Partnership's operating line of credit balance was $9.3 million on June 30, 2016. The $11.0 million tranche will be priced at LIBOR plus a spread of 104 basis points, net of patronage, and matures in 2027. The remaining $10.0 million portion of the facility remains available through March 31, 2017 and will be used to provide additional liquidity, if needed.

Taking into account the aforementioned borrowings, our interest coverage ratio is greater than 5 to 1 on a pro-forma basis using 2015 results and layering in these new debt facilities. This level is consistent with that of our timber-REIT peers and maintains a balance sheet that enables us to take advantage of the harvest optionality characteristic that is so important for this timberland asset class.

Outlook

Depending on log markets, we expect our total 2016 harvest volume to be between 88 and 93 MMBF, including volume from the new timberland acquisition. For our Real Estate segment, markets remain strong and in the second half of 2016 we anticipate significant residential lot sales from our Harbor Hill project as well as some potential sales of undeveloped land.

The financial schedules accompanying this earnings release provide detail on individual segment results and operating statistics.

About Pope Resources

Pope Resources, a publicly traded limited partnership, and its subsidiaries Olympic Resource Management and Olympic Property Group, own or manage 215,000 acres of timberland and development property in Washington, Oregon, and California. We also manage, co-invest in, and consolidate two private equity timber funds, for which we earn management fees. These funds provide an efficient means of investing our own capital in Pacific Northwest timberland while earning fees from managing the funds for third-party investors. The Partnership and its predecessor companies have owned and managed timberlands and development properties for over 160 years. Additional information on the company can be found at www.poperesources.com. The contents of our website are not incorporated into this release or into our filings with the Securities and Exchange Commission.

Forward Looking Statements

This press release contains a number of projections and statements about our expected financial condition, operating results, business plans and objectives, and about management's plans for future operations and strategies. These statements reflect management's estimates based on current goals and its expectations about future developments. Because these statements describe our goals, objectives, and anticipated performance, they are inherently uncertain, and some or all of these statements may not come to pass. Accordingly, they should not be interpreted as promises of future management actions or financial performance. Our future actions and actual performance will vary from current expectations and under various circumstances the results of these variations may be material and adverse. Among those forward-looking statements contained in this report are statements about management's expectations for future log prices, harvest volumes and markets, and statements about our expectations for future sales in our Real Estate segment. However, readers should note that all statements other than expressions of historical fact are forward-looking in nature. Some of the factors that may cause actual operating results and financial condition to fall short of expectations, or that may cause us to deviate from our current plans, include our ability to accurately predict fluctuations in log markets domestically and internationally, and to adjust our harvest volumes timely and appropriately; our ability to estimate the cost of ongoing and changing environmental remediation obligations, including our ability to anticipate and address the political and regulatory climate that affects these obligations; our ability to consummate various pending and anticipated real estate transactions on the terms management expects; our ability to manage our timber funds and their assets in a manner that our investors consider acceptable, and to raise additional capital or establish new funds on terms that are advantageous to the Partnership; conditions in the housing construction and wood-products markets, both domestically and globally, that affect demand for our products; the effects of competition, particularly by larger and better-financed competitors; fluctuations in foreign currency exchange rates that affect both competition for sales of our products and our customers' demand for them; the effect of treaties and other international agreements that affect the supply of logs in the United States and demand for logs overseas; conditions affecting credit markets as they affect the availability of capital and costs of borrowing; labor, equipment and transportation costs that affect our net income; our ability to anticipate and mitigate potential impacts of our operations on adjacent properties; the impacts of natural disasters on our timberlands and on surrounding areas; and our ability to discover and to accurately estimate other liabilities associated with our assets. Other factors are set forth in that part of our Annual Report on Form 10-K entitled "Risk Factors."

Other issues that may have an adverse and material impact on our business, operating results, and financial condition include those risks and uncertainties discussed in our other filings with the Securities and Exchange Commission. Forward-looking statements in this release are made only as of the date shown above, and we cannot undertake to update these statements.

|

CONDENSED CONSOLIDATED STATEMENTS OF INCOME (LOSS) | |||||||||||||||

|

(all amounts in $000's, except per unit amounts) | |||||||||||||||

|

Quarter ended June 30, |

Six Months Ended | ||||||||||||||

|

2016 |

2015 |

2016 |

2015 | ||||||||||||

|

Revenue |

$ |

12,713 |

$ |

13,904 |

$ |

23,782 |

$ |

40,812 |

|||||||

|

Cost of sales |

(7,471) |

(8,815) |

(14,611) |

(23,312) |

|||||||||||

|

Operating expenses |

(5,100) |

(4,909) |

(10,077) |

(9,247) |

|||||||||||

|

Gain on sale of timberland |

— |

— |

226 |

— |

|||||||||||

|

Operating income (loss) |

142 |

180 |

(680) |

8,253 |

|||||||||||

|

Interest expense, net |

(747) |

(777) |

(1,405) |

(1,522) |

|||||||||||

|

Income (loss) before income taxes |

(605) |

(597) |

(2,085) |

6,731 |

|||||||||||

|

Income tax expense |

— |

(28) |

(50) |

(368) |

|||||||||||

|

Net income (loss) |

(605) |

(625) |

(2,135) |

6,363 |

|||||||||||

|

Net loss attributable to noncontrolling interests |

1,041 |

914 |

1,536 |

1,735 |

|||||||||||

|

Net income (loss) attributable to Pope Resources' unitholders |

$ |

436 |

$ |

289 |

$ |

(599) |

$ |

8,098 |

|||||||

|

Basic and diluted weighted average units outstanding |

4,313 |

4,298 |

4,312 |

4,296 |

|||||||||||

|

Basic and diluted net income (loss) per unit |

$ |

0.09 |

$ |

0.06 |

$ |

(0.15) |

$ |

1.87 |

|||||||

|

CONDENSED CONSOLIDATING BALANCE SHEETS | |||||||||||||||||||

|

(all amounts in $000's) | |||||||||||||||||||

|

June 30, 2016 |

December 31, | ||||||||||||||||||

|

Assets: |

Pope |

ORM |

Consolidating |

Consolidated |

|||||||||||||||

|

Cash and cash equivalents |

$ |

912 |

$ |

1,892 |

$ |

— |

$ |

2,804 |

$ |

9,706 |

|||||||||

|

Land held for sale |

6,624 |

6,624 |

3,642 |

||||||||||||||||

|

Other current assets |

2,811 |

1,085 |

(644) |

3,252 |

4,048 |

||||||||||||||

|

Total current assets |

10,347 |

2,977 |

(644) |

12,680 |

17,396 |

||||||||||||||

|

Timber and roads, net |

33,855 |

229,445 |

263,300 |

266,104 |

|||||||||||||||

|

Timberland |

14,954 |

38,996 |

53,950 |

53,879 |

|||||||||||||||

|

Land held for development |

26,860 |

26,860 |

25,653 |

||||||||||||||||

|

Buildings and equipment, net |

5,832 |

15 |

5,847 |

6,024 |

|||||||||||||||

|

Investment in ORM Timber Funds |

18,284 |

(18,284) |

— |

— |

|||||||||||||||

|

Deposit for acquisition of timberland |

1,581 |

1,581 |

— |

||||||||||||||||

|

Other assets |

969 |

969 |

1,000 |

||||||||||||||||

|

Total assets |

$ |

112,682 |

$ |

271,433 |

$ |

(18,928) |

$ |

365,187 |

$ |

370,056 |

|||||||||

|

Liabilities and equity: |

|||||||||||||||||||

|

Current liabilities |

$ |

4,779 |

$ |

1,760 |

$ |

(644) |

$ |

5,895 |

$ |

5,426 |

|||||||||

|

Current portion of long-term debt |

117 |

117 |

114 |

||||||||||||||||

|

Current portion of environmental remediation |

11,905 |

11,905 |

11,200 |

||||||||||||||||

|

Total current liabilities |

16,801 |

1,760 |

(644) |

17,917 |

16,740 |

||||||||||||||

|

Long-term debt |

36,492 |

57,257 |

93,749 |

84,537 |

|||||||||||||||

|

Environmental remediation and other long-term liabilities |

809 |

809 |

5,713 |

||||||||||||||||

|

Total liabilities |

54,102 |

59,017 |

(644) |

112,475 |

106,990 |

||||||||||||||

|

Partners' capital |

58,580 |

212,416 |

(212,693) |

58,303 |

64,548 |

||||||||||||||

|

Noncontrolling interests |

194,409 |

194,409 |

198,518 |

||||||||||||||||

|

Total liabilities and equity |

$ |

112,682 |

$ |

271,433 |

$ |

(18,928) |

$ |

365,187 |

$ |

370,056 |

|||||||||

|

RECONCILIATION BETWEEN NET INCOME (LOSS) AND CASH FLOWS FROM OPERATIONS | |||||||||||||||

|

(all amounts in $000's) | |||||||||||||||

|

Quarter ended June 30, |

Six months ended June 30, | ||||||||||||||

|

2016 |

2015 |

2016 |

2015 | ||||||||||||

|

Net income (loss) |

$ |

(605) |

$ |

(625) |

$ |

(2,135) |

$ |

6,363 |

|||||||

|

Add back (deduct): |

|||||||||||||||

|

Depletion |

1,863 |

1,737 |

4,193 |

4,948 |

|||||||||||

|

Equity-based compensation |

178 |

242 |

594 |

580 |

|||||||||||

|

Excess tax benefit of equity-based compensation |

— |

— |

— |

(5) |

|||||||||||

|

Real estate project expenditures |

(4,656) |

(2,029) |

(5,225) |

(4,615) |

|||||||||||

|

Depreciation and amortization |

187 |

159 |

371 |

314 |

|||||||||||

|

Deferred taxes |

— |

24 |

— |

203 |

|||||||||||

|

Cost of land sold |

133 |

2,425 |

1,037 |

6,503 |

|||||||||||

|

Gain on sale of timberland |

— |

— |

(226) |

— |

|||||||||||

|

Gain on disposal of property and equipment |

(11) |

— |

(24) |

— |

|||||||||||

|

Change in environmental remediation liability |

(953) |

(286) |

(4,175) |

(572) |

|||||||||||

|

Change in other operating accounts |

1,527 |

1,423 |

1,293 |

(1,527) |

|||||||||||

|

Cash provided by (used in) operations |

$ |

(2,337) |

$ |

3,070 |

$ |

(4,297) |

$ |

12,192 |

|||||||

|

SEGMENT INFORMATION | |||||||||||||||

|

(all amounts in $000's) | |||||||||||||||

|

Quarter ended June 30, |

Six months ended June 30, | ||||||||||||||

|

2016 |

2015 |

2016 |

2015 | ||||||||||||

|

Revenue: |

|||||||||||||||

|

Partnership Fee Timber |

$ |

8,134 |

$ |

4,771 |

$ |

12,524 |

$ |

13,561 |

|||||||

|

Funds Fee Timber |

4,136 |

4,501 |

9,498 |

11,657 |

|||||||||||

|

Total Fee Timber |

12,270 |

9,272 |

22,022 |

25,218 |

|||||||||||

|

Timberland Management |

— |

— |

8 |

— |

|||||||||||

|

Real Estate |

443 |

4,632 |

1,752 |

15,594 |

|||||||||||

|

Total |

$ |

12,713 |

$ |

13,904 |

$ |

23,782 |

$ |

40,812 |

|||||||

|

Operating income (loss): |

|||||||||||||||

|

Fee Timber |

$ |

2,969 |

$ |

1,588 |

$ |

5,453 |

$ |

6,448 |

|||||||

|

Timberland Management |

(603) |

(785) |

(1,269) |

(1,514) |

|||||||||||

|

Real Estate |

(1,165) |

575 |

(2,201) |

5,707 |

|||||||||||

|

General & Administrative |

(1,059) |

(1,198) |

(2,663) |

(2,388) |

|||||||||||

|

Total |

$ |

142 |

$ |

180 |

$ |

(680) |

$ |

8,253 |

|||||||

|

SELECTED STATISTICS | |||||||||||

|

Quarter ended June 30, |

Six months ended June 30, | ||||||||||

|

2016 |

2015 |

2016 |

2015 | ||||||||

|

Log sale volumes by species (million board feet): |

|||||||||||

|

Sawlogs |

|||||||||||

|

Douglas-fir |

9.4 |

7.8 |

18.2 |

19.1 |

|||||||

|

Whitewood |

5.4 |

3.0 |

8.0 |

9.0 |

|||||||

|

Pine |

1.2 |

1.1 |

1.2 |

1.1 |

|||||||

|

Cedar |

1.0 |

0.5 |

1.9 |

1.8 |

|||||||

|

Hardwood |

0.7 |

0.4 |

1.3 |

1.9 |

|||||||

|

Pulpwood - all species |

3.2 |

2.3 |

6.0 |

6.7 |

|||||||

|

Total |

20.9 |

15.1 |

36.6 |

39.6 |

|||||||

|

Log sale volumes by destination (million board feet): |

|||||||||||

|

Export |

3.2 |

2.1 |

6.1 |

6.8 |

|||||||

|

Domestic |

13.8 |

10.3 |

23.2 |

24.2 |

|||||||

|

Hardwood |

0.7 |

0.4 |

1.3 |

1.9 |

|||||||

|

Pulpwood |

3.2 |

2.3 |

6.0 |

6.7 |

|||||||

|

Subtotal log sale volumes |

20.9 |

15.1 |

36.6 |

39.6 |

|||||||

|

Timber deed sale |

— |

— |

— |

0.6 |

|||||||

|

Total |

20.9 |

15.1 |

36.6 |

40.2 |

|||||||

|

Average price realizations by species (per thousand board feet): |

Quarter ended June 30, |

Six months ended June 30, | |||||||||||||

|

2016 |

2015 |

2016 |

2015 | ||||||||||||

|

Sawlogs |

|||||||||||||||

|

Douglas-fir |

$ |

596 |

$ |

608 |

$ |

608 |

$ |

629 |

|||||||

|

Whitewood |

550 |

541 |

530 |

550 |

|||||||||||

|

Pine |

500 |

552 |

500 |

551 |

|||||||||||

|

Cedar |

1,271 |

1,120 |

1,384 |

1,398 |

|||||||||||

|

Hardwood |

521 |

532 |

529 |

623 |

|||||||||||

|

Pulpwood - all species |

290 |

322 |

300 |

326 |

|||||||||||

|

Overall |

563 |

562 |

575 |

591 |

|||||||||||

|

Average price realizations by destination (per thousand board feet): |

|||||||||||||||

|

Export |

$ |

607 |

$ |

604 |

$ |

636 |

$ |

646 |

|||||||

|

Domestic |

618 |

608 |

632 |

647 |

|||||||||||

|

Hardwood |

521 |

532 |

529 |

623 |

|||||||||||

|

Pulpwood |

290 |

322 |

300 |

326 |

|||||||||||

|

Overall log sales |

563 |

562 |

575 |

591 |

|||||||||||

|

Timber deed sale |

— |

— |

— |

389 |

|||||||||||

|

Owned timber acres |

111,000 |

111,000 |

111,000 |

111,000 |

|||||||||||

|

Acres owned by Funds |

94,000 |

80,000 |

94,000 |

80,000 |

|||||||||||

|

Depletion expense per MBF - Partnership tree farms |

$ |

43 |

$ |

48 |

$ |

43 |

$ |

47 |

|||||||

|

Depletion expense per MBF - Fund tree farms |

$ |

177 |

$ |

166 |

$ |

201 |

$ |

192 |

|||||||

|

Capital and development expenditures ($000's) |

$ |

4,450 |

$ |

2,201 |

$ |

6,283 |

$ |

5,879 |

|||||||

|

PERIOD TO PERIOD COMPARISONS | |||||||

|

(Amounts in $000's except per unit data) | |||||||

|

Q2 2016 vs. |

YTD 2016 vs. | ||||||

|

Q2 2015 |

YTD 2015 | ||||||

|

Net income (loss) attributable to Pope Resources' unitholders: |

|||||||

|

2nd Quarter 2016 |

$ |

436 |

$ |

(599) |

|||

|

2nd Quarter 2015 |

289 |

8,098 |

|||||

|

Variance |

$ |

147 |

$ |

(8,697) |

|||

|

Detail of earnings variance: |

|||||||

|

Fee Timber |

|||||||

|

Log volumes (A) |

$ |

3,260 |

$ |

(1,773) |

|||

|

Log price realizations (B) |

21 |

(586) |

|||||

|

Gain on sale of tree farms |

— |

226 |

|||||

|

Production costs |

(942) |

1,886 |

|||||

|

Depletion |

(206) |

675 |

|||||

|

Other Fee Timber |

(752) |

(1,423) |

|||||

|

Timberland Management |

182 |

245 |

|||||

|

Real Estate |

|||||||

|

Land sales |

(1,590) |

(3,314) |

|||||

|

Conservation easement sales |

— |

(4,311) |

|||||

|

Other Real Estate |

(150) |

(283) |

|||||

|

General & Administrative costs |

139 |

(275) |

|||||

|

Net interest expense |

30 |

117 |

|||||

|

Taxes |

28 |

318 |

|||||

|

Noncontrolling interest |

127 |

(199) |

|||||

|

Total variance |

$ |

147 |

$ |

(8,697) |

|||

|

(A) Volume variance calculated by extending change in sales volume by the average log sales price for the comparison period. |

|

(B) Price variance calculated by extending the change in average realized price by current period volume. |

|

September 30, 2016 Pro Forma Capitalization | ||||||||||||||||||||

|

(Partnership only) | ||||||||||||||||||||

|

amounts in thousands, debt balances exclude debt issuance costs |

Sources |

Uses |

||||||||||||||||||

|

Maturity |

Net |

Balance |

Timberland |

Other |

Timberland |

Debt |

Other uses |

Pro Forma | ||||||||||||

|

Interest-only, fixed-rate mortgage |

2017 |

3.85 |

% |

$5,000 |

$5,000 |

|||||||||||||||

|

Interest-only, fixed-rate mortgage |

2019 |

5.40 |

% |

9,800 |

9,800 |

|||||||||||||||

|

Revolving line of credit (4) |

2020 |

1.22 |

% |

9,250 |

($9,250) |

— |

||||||||||||||

|

Amortizing, fixed-rate mortgage |

2023 |

2.80 |

% |

2,636 |

(29) |

2,607 |

||||||||||||||

|

Interest-only, fixed-rate mortgage |

2025 |

5.05 |

% |

10,000 |

10,000 |

|||||||||||||||

|

Interest-only, variable-rate mortgage (5) |

2023 |

1.89 |

% |

$10,000 |

10,000 |

|||||||||||||||

|

Interest-only, fixed-rate mortgage |

2026 |

3.08 |

% |

11,000 |

11,000 |

|||||||||||||||

|

Interest-only, variable-rate mortgage (6) |

2027 |

1.54 |

% |

$11,000 |

11,000 |

|||||||||||||||

|

Interest-only, fixed-rate mortgage |

2028 |

3.32 |

% |

11,000 |

11,000 |

|||||||||||||||

|

Total debt |

$36,686 |

$ |

70,836 |

|||||||||||||||||

|

Less: Cash |

912 |

$32,000 |

$11,000 |

($31,901) |

($9,279) |

($2,732) |

— |

|||||||||||||

|

Net debt |

$35,774 |

$70,836 |

||||||||||||||||||

|

Equity market cap (7) |

$282,639 |

$282,639 |

||||||||||||||||||

|

Net debt / enterprise value (8) |

11.2 |

% |

20 |

% | ||||||||||||||||

|

Weighted average interest rate, net of patronage |

3.9 |

% |

3.3 |

% | ||||||||||||||||

|

(1) Interest rate net of patronage of 100 bps on debt held at 6/30/16 and 81 bps on new debt | ||||||||||||||||||||

|

(2) Additional $10.0 million available, must be drawn by 3/31/2017 | ||||||||||||||||||||

|

(3) Including, but not limited to, acquisition closing costs, environmental remediation expenditures and Harbor Hill development costs | ||||||||||||||||||||

|

(4) Maximum borrowing limit of $20.0 million | ||||||||||||||||||||

|

(5) Rate is based on LIBOR of 0.50% plus spread of 1.39% (net of patronage) | ||||||||||||||||||||

|

(6) Rate is based on LIBOR of 0.50% plus spread of 1.04% (net of patronage) | ||||||||||||||||||||

|

(7) Based on unit price of $65 and outstanding units of 4,348,298 | ||||||||||||||||||||

|

(8) Enterprise value equals equity market cap plus net debt | ||||||||||||||||||||

The following table presents the calculation of our interest coverage ratio on a pro-forma basis utilizing 2015 results and interest expense under these new loans.

|

Amounts in thousands, except interest coverage ratio |

|||

|

Net income attributable to unitholders |

$ |

10,943 |

|

|

Interest expense |

2,970 |

||

|

Less: interest expense attributable to noncontrolling interests |

(2,111) |

||

|

Income taxes |

207 |

||

|

Less: income tax expense attributable to noncontrolling interests |

(292) |

||

|

Depreciation and amortization expense |

736 |

||

|

Less: depreciation and amortization expense attributable to noncontrolling interests |

(20) |

||

|

Depletion expense |

9,900 |

||

|

Less: depletion expense attributable to noncontrolling interests |

(7,076) |

||

|

EBITDDA attributable to unitholders |

$ |

15,257 |

|

|

Interest expense attributable to unitholders, including capitalized interest |

1,743 |

||

|

Interest expense related to new $32 and $11 million borrowings |

1,062 |

||

|

Pro-forma 2015 interest expense attributable to unitholders, including capitalized interest |

$ |

2,805 |

|

|

Pro-forma interest coverage ratio |

5.4 |

||

Photo - http://photos.prnewswire.com/prnh/20160805/396035

To view the original version on PR Newswire, visit:http://www.prnewswire.com/news-releases/pope-resources-reports-second-quarter-income-of-436000-acquisition-of-7324-acres-of-washington-timberland-new-financing-300310045.html

SOURCE Pope Resources

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.