Indivior guided for peak sales of $50 - $100 Million for their nasal naloxone product, according to Sarah Potter of Deutsche Bank. However, last week the FDA rejected Indivior's New Drug Application (NDA). Potter says the nasal naloxone product made up 5% of the present value of Indivior shares in her valuation model, or roughly $160 Million.

The week prior, Lightlake Therapeutics (LLTP) - a $19 Million market cap company - received FDA approval for their nasal naloxone product, called Narcan. Lightlake licensed Narcan to Adapt Pharma in exchange for a royalty and $55 Million in milestone payments a year ago.

Adapt Pharma - a $95-Million backed specialty pharma Company led by the team that sold Azur to Jazz Pharmaceuticals for $500 Million in 2011 (the deal is now worth approx. $2 Billion) - is totally focused on marketing Narcan.

If Just 10% Of What Deutsche Bank Believes Is Present Value ($160M) For A Nasal Naloxone Product Is Attributed To Lightlake, How Is It That The Company Trades For Just $19 Million?

LLTP has 3 clinical stage drug candidates, including a registration-study ready drug for Binge Eating Disorder, and could potentially see future royalties (not to mention sales-based milestone payments) from its Narcan product dwarf its current market cap.

LLTP has raised over $6 Million in non-dilutive financing in the last 12 months, at an implied valuation of $50 - $75 Million. In addition, LLTP should receive ~$3.75 Million from Adapt following FDA approval of Narcan [1].

Indivior traded down ~5% on the FDA's rejection of their nasal naloxone drug candidate. If a rejection cost Indivior ~$60M in market value, shouldn't some or all of this be LLTP's gain?

Paired Trades In Sarepta/BioMarin Show How An Efficient Market Functions. Lack of Movement In LLTP Following Indivior News Suggests An Arbitrage Opportunity Still Exists.

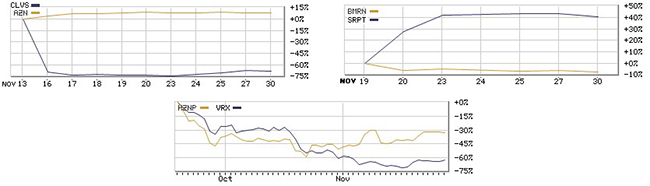

When AstraZeneca's (AZN) lung cancer therapy, Tagrisso, was approved by the FDA ahead of schedule, this adversely affected Clovis (CLVS), who had a competing drug, also pending FDA approval. Further, the FDA requested Clovis provide additional data before their drug could be approved. As might be expected, these news adversely affected shares of Clovis, and appear to have buoyed AstraZeneca's shares, as shown in Figure 1, below.

Figure 1: AstraZeneca Advanced On Clovis' SetBack; Sarepta Jumped On A Bad Panel Review For BioMarin. This Begs The Question: Is LLTP Ripe For A Move Off Of Indivior's Bad Break?

Sarepta (SRPT) and BioMarin (BMRN) were also in a tight race for potential regulatory approval for a rare disease called Duchenne muscular dystrophy (DMD). A FDA advisory panel meeting and potential approval date, or PDUFA, was scheduled first for BioMarin. As might be expected, this news adversely affected Sarepta.

However, the advisory panel was not favorable to BioMarin, suggested the Company's drug may face obstacles in winning approval. As Figure 1, above, clearly shows, Sarepta leaped on this outcome. Similarly, scrutiny in drug pricing hit specialty pharma names across the board: after Valeant (VRX) took a hit, Horizon Pharma (HZNP) and DepoMed (DEPO) sold off in tandem.

Particularly in the cases of AstraZeneca/Clovis and BioMarin/Sarepta, first to market with a novel drug for an unaddressed medical need is a substantial advantage. We wrote earlier that companies were paying over $100 Million for ‘vouchers' - just to cut FDA review time from 10 to 6 months [3]. This explains why these companies have experienced volatility worth hundreds of millions of dollars after either gaining or losing their position as first to market.

Indivior's Setback With The FDA Puts LLTP Ahead 6-12 Months.

Indivior and Lightlake were neck and neck for potential FDA approval of a reformulation of naloxone – an essential medicine used to treat opioid overdose. But last week the FDA put Indivior back at least 6-12 months. Both LLTP and Indivior had applied for regulatory approval of a device that allows naloxone to be administered through the nasal cavity. The FDA approved LLTP's drug, called Narcan, and later issued Indivior a Complete Response Letter (rejection letter) stating that their nasal naloxone did not closely enough mimic naloxone injection [2].

If Indivior's application did not prove that uptake of naloxone through their nasal spray device was effectively the same as when naloxone is administered through injection, the company could be forced to alter its drug dose. If this is the case, and an additional study is required, Indivior could find itself 12+ months behind LLTP and partner Adapt Pharma, who have already announced that Narcan will sell for $37.50 per kit, compared to Indivior's nasal spray at $50, most naloxone syringes at $30+ and an auto-injector approved last year at $500+.

We believe first-mover advantage could be worth tens of millions, conservatively, in present market value to LLTP, which trades at just $19 Million in the market.

Indivior Setback Could Be Worth $39 Million or $21 Per Share To This $10 LLTP Stock, According To Conservative Estimates

Lightlake's nasal naloxone, Narcan, is marketed by Adapt Pharma, who pays Lightlake a royalty on worldwide sales. Adapt is led by an experienced group of pharma executives with expertise in specialty drugs, like naloxone.

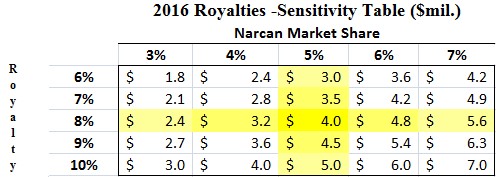

We assumed that since LLTP/Adapt are first to market with a nasal naloxone - the need for which is dire - Narcan will capture 5% of the market in 2016. We further assumed an 8% royalty would flow to Lightlake, as shown in Figure 2, below.

Figure 2: Under Conservative Assumptions, LLTP Could Receive $4.0M in 2016 Royalties

Under our assumption, Lightlake would receive $4 Million in royalty revenue in 2016. This is based off the low end ($50M) of Indivior's own internal guidance for sales of their nasal naloxone, which, you might recall, did not receive FDA approval.

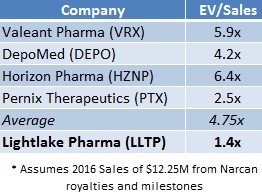

We took a random sample of specialty pharma companies and compared their valuations to Lightlake's projected sales in 2016. Inclusive in our estimate of Lightlake's sales is a $3.75M milestone payment for winning FDA approval and a $4.8M sales milestone.

If our assumptions hold true, Lightlake should see 2016 revenue of $12.25 Million. If we apply the average EV/Sales multiple among specialty pharma companies Valeant, DepoMed et al., as shown in Figure 3, below, LLTP shares would be worth $31, excluding cash.

Figure 3: LLTP Currently Trades at 1.4x EV/Sales; Peers Command 4.75x

The question of what Indivior's setback might be worth to Lightlake is quantifiable. Based on our conservative assumptions, it's worth the difference between $31 and LLTP's current market value – roughly $10 a share.

In other words, if LLTP captures $12.25 Million in sales in 2016, shares have an implicit upside of 211% from recent market prices.

References

[1] Computed as 50% of regulatory milestones of $7.5M, see http://ir.baystreet.ca/article.aspx?id=178&1448018042

[2] http://indivior.com/investor-news/indivior-receives-complete-response-letter-from-fda-not-approving-naloxone-nasal-spray-new-drug-application-for-opioid-overdose/

[3] FDA Fast-Track Should Accrete Significant Value to This Overlooked Biotech

[4] http://ir.baystreet.ca/article.aspx?id=153

[5] http://www.fiercemedicaldevices.com/story/kal-o-cuts-price-auto-injector-opioid-overdose-partnership-clinton-foundati/2015-01-27

About One Equity Research

One Equity Research is a leading provider of proprietary and in-depth research crafted by respected financial analysts and domain experts. Our team includes trained finance professionals with diverse backgrounds that include equity research, investment banking, and strategic consulting at preeminent firms. We distribute our research through mainstream media partners and to subscribers of our Intelligence Service. To learn more please visit http://www.oneequityresearch.com/

Legal Disclaimer: This research note has been prepared by One Equity Research, LLC ("One Equity") on behalf of Lightlake Therapeutics ("Lightlake" or the "Company") as part of research coverage services. We have received one hundred twenty thousand dollars and ten thousand restricted shares of Lightlake for our services as of the date of this report. One Equity intends to sell its shares in the Company as soon as it is legally permissible to do so. We may receive additional compensation in the future. This research note is not an offer or solicitation to buy or sell the securities of Lightlake. Information contained in this note is believed to be accurate as of the date of publication. This note is for information purposes only, and is not intended to (and is provided explicitly on the condition that it not) be used as a basis to make any investment decisions. Investing involves considerable risk. One Equity urges all readers to carefully review the Company's SEC filings and consult with an investment professional before making any investment decisions. Investors should make their own determinations whether an investment in any particular security is consistent with their investment objectives, risk tolerance, and financial situation. Please read our full disclaimer at http://www.oneequityresearch.com/terms/

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.