NEW YORK, May 13, 2019 /PRNewswire/ -- Neuberger Berman Investment Advisers LLC and certain of its affiliates ("Neuberger Berman") that manage investment funds and client accounts that collectively own approximately 1,743,123 shares, or 2.7%, of the outstanding stock of Verint Systems, Inc. VRNT ("Verint" or the "Company") announced that it has delivered an open letter to Verint stockholders today.

"We continue to be disappointed with the Company's response to our engagement with them," said Benjamin Nahum, Senior Portfolio Manager and Managing Director, Neuberger Berman. Mr. Nahum continued, "Instead of agreeing to report industry-standard metrics for its cloud business, financial targets for its capital allocation plans, and upgrade the Board with critical software expertise, Verint has announced plans to spend $6.5 million fighting us, one of its longest-holding shareholders." Neuberger Berman has been a shareholder for more than 10 years.

Neuberger Berman details three steps to maximize value for Verint shareholders:

- Commit to transitioning to a modern cloud business model, with identified medium- and long-range financial and performance targets that give shareholders visibility into its growth and revenue quality, and the ability to hold management accountable;

- Clearly articulate the Company's capital allocation priorities and present a compelling case for its current business configuration, so shareholders know how their capital will be used to create value and why the Board believes the current conglomerate structure is optimal; and

- Upgrade the Board, by adding professionals with substantial software, analytics, cloud and corporate governance expertise to give shareholders confidence that the Board is properly overseeing the Company's strategy and will hold management accountable for performance.

The full text of the Neuberger Berman letter to Verint follows:

May 13, 2019

To Our Fellow Verint Shareholders:

We are writing to you on behalf of Neuberger Berman Investment Advisers LLC and certain of its affiliates ("Neuberger Berman") with respect to your investment in Verint Systems, Inc. ("Verint" or the "Company"). We are significant, long-term investors in Verint and we are asking you to elect three new, highly-qualified software executives to the Company's eight-person Board at the upcoming annual meeting of shareholders.

About Neuberger Berman and Why We Are Asking for Your Vote

Neuberger Berman was founded in 1939 to do one thing: deliver compelling investment results for our clients over the long term. That remains our singular purpose today, driven by a culture rooted in deep fundamental research and facilitated by the free exchange of ideas with the companies that we invest in.

Our Intrinsic Value Strategy has been invested in Verint since 2006 and currently owns 1,743,123 shares, or approximately 2.7%, of Verint's outstanding stock.

We firmly believe that Verint has the opportunity to create substantial value for its owners. However, for long-term investors like us, it has been particularly frustrating to watch Verint lag behind its peers, year after year, on many levels, including organic sales growth, operating margin and, most importantly, total shareholder return.

For the past 1, 3, 5 and 15 years, Verint has substantially underperformed its peers and the broader market. Indeed, NICE Ltd., its close peer, has generated a return for its investors that is approximately 8 times Verint's return over the last 15 years. Smaller companies that lack Verint's impressive technology base and extensive customer relationships have also created more value for their shareholders, while growing faster.

Total Shareholder Returns through Fiscal Year-End | ||||

January 31, 2019 | ||||

1 Year | 3 Years | 5 Years | 15 Years | |

Verint | 15.9% | 32.1% | 6.5% | 96.6% |

NICE Ltd. | 20.7% | 83.9% | 189.5% | 745.2% |

S&P 500 | -2.3% | 48.2% | 68.2% | 225.7% |

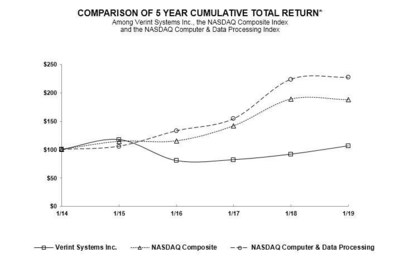

Despite Verint's claim that it has outperformed for shareholders, its own performance graph demonstrates that Verint's stock has woefully lagged relevant benchmarks. For example, $100 invested on January 31, 2014 in Verint stock would have been worth $106.45 on January 31, 2019. By contrast, $100 invested in the NASDAQ Computer & Data Processing Index during that same period would have been worth $227.03.

Source: Verint 10K for fiscal year-end January 31, 2019

* $100 invested on 1/31/14 in stock or index, including reinvestment of dividends

Over the past 20 years, the Intrinsic Value Strategy has made more than 450 investments in out-of-favor companies, one quarter of them in the technology sector. At Neuberger Berman, we believe that patience can reward the long-term investor in companies with excellent technology and great customers. But not always. When patience alone isn't working, we try to share with management our observations and urge management to implement strategies and best practices that have succeeded elsewhere.

For the last two years, Neuberger Berman has attempted to do this with Verint. Unfortunately, we faced a reluctant Board of Directors and an insular management team. While we are pleased that some of our recommendations – such as cloud revenue disclosure – have recently been adopted, these changes (which we believe are inadequate) only occurred after persistent pressure from us (and other shareholders) and after we submitted to Verint our nomination notice for the election of three new directors to the Board at the 2019 annual meeting. We're gratified that the stock market has reacted positively to our suggestions and management's promise to provide shareholders with improved disclosures. However, those promises - even assuming that they are fulfilled - are not enough.

In our view, Verint's reluctance to embrace a cloud business model, inefficient conglomerate structure, elevated operating expenses, poor capital allocation practices, and misaligned executive compensation programs have all contributed to the Company's persistent underperformance. Responsibility for Verint's longstanding failure to move with urgency to improve its performance and adopt clear business and financial performance targets lies with the current Board of Directors. This Board has simply been unwilling to make the changes that are necessary to correct Verint's course.

This is why we have reached the conclusion that Verint will benefit from additional perspectives in the boardroom provided by independent, experienced, senior-level software business leaders.

We believe Verint needs to do three things to maximize value for its shareholders:

- Commit to transitioning to a modern cloud business model, with identified medium- and long-range financial and performance targets that give shareholders visibility into its growth and revenue quality, and the ability to hold management accountable;

- Clearly articulate the Company's capital allocation priorities and present a compelling case for its current business configuration, so shareholders know how their capital will be used to create value and why the Board believes the current conglomerate structure is optimal; and

- Upgrade the Board, by adding professionals with substantial software, analytics, cloud and corporate governance expertise to give shareholders confidence that the Board is properly overseeing the Company's strategy and will hold management accountable for performance.

We have spent a considerable amount of time with the Company attempting to get it to commit to these simple, yet important, changes and we have been largely ignored.

Verint Should Commit to Transitioning to a Modern Cloud Model

We have specifically engaged with the Company about its lack of a coherent cloud strategy and disclosure for over a year now. Only on the Company's last earnings call did management begin to offer shareholders a glimpse into the Company's cloud plans. As we predicted, Verint's long-suffering shareholders cheered even this modest clarification of the Company's strategy.

But we don't think the Company is doing enough.

Verint has been very slow to embrace the industry-wide migration to a cloud-based business model. Verint's management continues to plod along at a sluggish pace, suggesting that its customers may not actually want to transition to the cloud. We don't believe it. Not only is that counter to industry practice and the perspective of sell-side analysts, we believe Verint's customers will be receptive to the conversion. Furthermore, the cloud model is a more profitable and predictable business model, which is why other software companies have readily embraced the move.

"…Verint's revenue disclosures are lacking...it does not provide inorganic revenue, maintenance revenue, or cloud revenue, metrics we believe would help us better judge the quality of revenue, the contribution to growth of different revenue streams, and organic growth."

Samad Samana, Jefferies research analyst

Jefferies Research Report January 10, 2019

It wasn't easy, but we managed to at least get the Company to talk with shareholders a bit more about its cloud business model. Now, shareholders need clear guidance and objective metrics both to know that the Company is truly committed to these plans and to be able to hold management accountable for the transition.

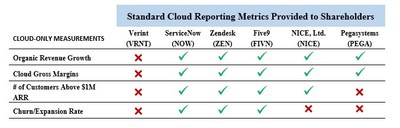

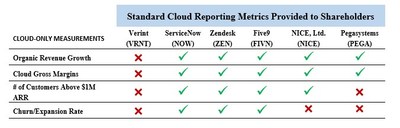

Absent guidance and ongoing disclosure, shareholders cannot properly predict, model or value Verint's cloud business or the Company. Verint should adopt the same set of metrics that other comparable cloud-based software companies have already implemented, including: cloud-only revenue and gross margins, the number of customers above $1 million in annual recurring revenue and cloud churn/expansion rate.

These are the metrics that investors and analysts are looking for and measurements other Boards use to hold management accountable.

Verint Financial Reporting vs. Comparable Software Companies

Verint Should Clearly Articulate its Capital Allocation Priorities and Present a Compelling Case for its Current Conglomerate Structure

Verint has invested heavily in R&D and technology acquisitions over the past decade. However, this investment spree has failed to deliver any meaningful return to shareholders.

Verint spends more than 17% of its revenues on R&D, far above what other low-growth software companies spend. In the last 12 years, Verint has spent nearly $2.1 billion on acquisitions and over $1.9 billion on R&D and capital expenditures, for a total of over $4.0 billion of investments, which is more than Verint's entire market value today!

Over the past five years alone, Verint's R&D expense has increased at a rate of 10.5% per year. During that same period, the Company has spent nearly $1.0 billion on acquisitions. Despite this, revenue growth (including revenue obtained through acquisitions) was only 6.2% per year on average.

Examine the table below that compares the amount Verint and its peers have invested in R&D, CapEx and acquisitions over the past five years and the resulting increase in market cap value. Through January 31, 2019, Verint has invested a total of $2.2 billion, resulting in a mere $728 million increase in market cap value. On the other hand, ServiceNow has invested a total of $2.9 billion, resulting in a market cap value increase of $31 billion!

This doesn't make any sense to us. Verint has been unable to adequately explain to shareholders why it spends so much on R&D and acquisitions without generating a reasonable return on its investment.

Verint vs. Comparable Software Companies | |||

5-Year Cumulative Market Cap Gain Compared to 5-Year Cumulative Investments | |||

5-Year Change | 5-Year Cumulative | Market Cap Gain as a | |

Five9 | $2,644 | $160 | 16.5x |

ServiceNow | $30,914 | $2,867 | 10.8x |

Zendesk | $6,196 | $856 | 7.2x |

Pegasystems | $2,705 | $955 | 2.8x |

NICE, Ltd.*** | $4,407 | $2,422 | 1.8x |

Verint | $728 | $2,161 | 0.3x |

*January 31, 2014 through January 31, 2019 except Five9 and Zendesk calculations use a start date of May 31, 2014, as they were not publicly traded on January 31, 2014. ** All calculations use past five fiscal years. *** Converted to $USD | |||

The Verint Board is responsible for overseeing the Company's R&D investments and acquisition strategy and ensuring that the Company's capital allocation practices focus on opportunities that generate appropriate shareholder returns. To this end, we believe it is imperative that the Board fully disclose to Verint shareholders a comprehensive and complete capital allocation plan.

While management has spent heavily on R&D + CapEx + Acquisitions, Verint's Board of Directors has allowed the share count to more than double over the last 12 years – growing from 31 million to almost 66 million shares outstanding today! We believe that, for a low-growth software company such as Verint, a robust share repurchase program should be an important component of its capital allocation strategy and that the Board should resist share dilution.

We also believe that shareholders do not understand why Verint has decided to maintain its ownership of both its Customer Engagement Solutions ("CES") and Cyber Intelligence Solutions ("CIS") divisions. We believe that these divisions serve different markets, have disparate products and service offerings, and do not share operational synergies.

Owning these two businesses makes it harder for the Company to receive a fair valuation from the public markets. In addition to the analytical complexity associated with shareholders trying to understand how the Company will allocate its limited capital, analyze different end-markets with different growth rates, and assess the optimal capital structure for two very different businesses, having two disparate businesses in a mid-size company undoubtedly taxes management's limited time and resources.

We believe Verint should honor its 2015 commitment to provide segment-level financials for CES and CIS. Instead, the Company only provides a one-line segment "contribution" figure and does not allocate shared corporate expenses (which represents more than 75% of segment contribution), SG&A and R&D expenses between the two segments. That opaque reporting prevents investors from appropriately valuing each business unit and its contribution to Verint as a whole.

If management and the Board believe it is optimal to have both CIS and CES under one corporate umbrella, they need to present a compelling case for this conglomerate strategy. We believe it is incumbent upon them to explain why this inefficient company configuration is good for shareholders.

Verint Should Upgrade its Board with Software, Analytics, Cloud, and Governance Expertise

Verint's Board today has only one independent director with any senior-level operating software experience. We think this is inadequate given the accelerating changes in the software landscape, the complexity of transitioning from enterprise software to a cloud-based model and the history of underperformance at Verint.

We believe the Company would benefit from fresh perspectives on the Board, especially from professionals that have built, executed and overseen cloud-based software businesses.

Over the past year, we have proposed seven different potential board members with a broad set of impressive technology, software, cloud, security, and governance credentials that we believe would benefit the Company and its shareholders. Unfortunately, Verint has rejected every single one of our proposed accomplished professionals.

We have, therefore, taken the extraordinary step of nominating three new directors to the Board and are asking our fellow shareholders to support their election at the upcoming annual meeting.

Our nominees are:

Ms. Beatriz Infante. Ms. Infante is a software industry veteran and a four-time CEO with a track record of successfully leading multiple international technology businesses to extremely high levels of growth, profitability and shareholder return. As one of the first employees of Oracle, Ms. Infante reported directly to Larry Ellison, and has since led both early stage and Fortune 100 organizations through $2B in revenues across a variety of technology sectors, including SaaS/Cloud, cybersecurity, enterprise software, big data & analytics, digital transformation, communications, mobile, and hardware.

Dr. Mark Greene. Dr. Greene is a senior financial software and analytics executive with 35+ years of global executive experience leading and growing complex global businesses. Over the course of his career, Dr. Greene managed several large enterprise software businesses, including as CEO of OpenLink, a high-growth, private equity-backed global software and services business, CEO of Fair Isaac Corporation (FICO), a pioneer in credit risk scoring and analytics for the financial services industry, and as a General Manager at IBM, where he was ultimately responsible for IBM's security business.

Mr. Oded Weiss. Mr. Weiss has 25+ years of experience in building value and creating high-performing leadership teams in fast growing global businesses. Mr. Weiss is the former President and currently a strategic advisor to Temenos, AG, a $12 billion market cap developer of a cloud-native front office, core banking, payments, fund management and wealth management software products for banks worldwide. Mr. Weiss also served as CEO and a Managing Director and a member of the Board of Directors of IGEFI Group s.a r.l. (doing business as Multifonds), an award-winning investment software company providing fund accounting, portfolio accounting and investor servicing and transfer agency on a single platform. Previous to this, Mr. Weiss was a Partner at McKinsey & Co. and led their technology practice in New York.

If elected, these nominees are committed to working with the other Directors to establish new financial measurements and a capital allocation framework while holding management accountable for performance.

In stark contrast, the Company has re-nominated last year's slate of eight candidates, including Mr. Howard Safir, who has been on Verint's Board for 17 years, who has never held a senior management role at a public company and whose primary experience is in law enforcement; Dr. Richard Nottenburg, who has been on Verint's Board for a total of 11 years, including the time he spent on the Board of Verint's former parent company, Comverse Technology, and who has had more than enough time to make a positive impact on the Company's financial performance; and Mr. John Egan, whose last executive role was 21 years ago, has been a Director and Chairman of the Corporate Governance & Nominating Committee since August 2012 and Verint's Lead Independent Director since August 2017, and who, in our view, has been an ineffective independent steward for Verint shareholders. And so, we are proposing to replace these long-tenured underperforming directors with our industry-experienced nominees.

The addition of Ms. Infante, Dr. Green and Mr. Weiss will ensure the board provides rigorous oversight of the Company's cloud strategy and capital allocation and business configuration.

Neuberger Berman's Nominees vs. Verint's Long-Tenured Directors

We encourage you to support our comprehensive approach for value creation at Verint by voting on the GOLD proxy card for our candidates.

Finally, we think it's important to let you know that we were astonished to learn that Verint intends to spend $6.5 million to run a proxy contest to defend the status quo. We tried to avoid this proxy contest and made multiple proposals to Verint to reach an acceptable compromise. In addition to rejecting all seven of our candidates, Verint has refused to commit publicly to sensible business measurements and financial targets that would enable shareholders to clearly understand Verint's strategy, measure its performance against that strategy and evaluate the Board's capital allocation choices. We are deeply troubled that Verint would spend so much of its shareholders' money to defend the record of the current Board. This underscores the need for immediate change at Verint and we look forward to your support.

On behalf of Neuberger Berman, we appreciate your time and attention to our shared investment.

If you have any questions about how to vote, our proxy solicitor, Okapi Partners, can be reached at info@okapipartners.com or (855) 305-0857.

Please sign, date and mail the GOLD proxy card, voting for Ms. Infante, Dr. Greene and Mr. Weiss.

Sincerely,

Benjamin H. Nahum

Senior Portfolio Manager and Managing Director

Neuberger Berman Investment Advisers LLC

Amit Solomon

Portfolio Manager and Managing Director

Neuberger Berman Investment Advisers LLC

IMPORTANT INFORMATION

On May 13, 2019, Neuberger Berman Investment Advisers LLC, Neuberger Berman Investment Advisers Holdings LLC, Neuberger Berman Group LLC, NBSH Acquisition LLC, Neuberger Berman Breton Hill ULC, NB Acquisitionco ULC, Neuberger Berman Canada Holdings LLC, Ms. Infante, Dr. Greene and Mr. Weiss (each of Ms. Infante, Dr. Greene and Mr. Weiss are referred to herein as a "Neuberger Berman Nominee" and, collectively with Neuberger Berman, as the "Neuberger Berman Participants", "our", "us" or "we"). Benjamin Nahum, Scott Hoina, Amit Solomon, Ph.D., Beatriz V. Infante, Dr. Mark Greene, and Oded Weiss (collectively, the "Participants") filed a definitive proxy statement on Schedule 14A (the "Neuberger Berman Proxy Statement") with the Securities and Exchange Commission ("SEC"), along with an accompanying GOLD proxy card, to be used in connection with the Participants' solicitation of proxies from the stockholders of Verint Systems Inc. (the "Company") for use at the Company's 2019 Annual Meeting of Stockholders (the "Proxy Solicitation"). All stockholders of the Company are advised to read the Neuberger Berman Proxy Statement and the accompanying GOLD proxy card because they contain important information. The Neuberger Berman Proxy Statement and the accompanying GOLD proxy card will be furnished to some or all of the Company's stockholders and are, along with other relevant soliciting material of the Participants, available at no charge at the SEC's website at www.sec.gov, from the Participants' proxy solicitor, Okapi Partners LLC (Call Toll-Free: (855) 305-0857). To the extent that independent researchers or financial analysts are quoted in this document, it is the policy of the Participants to use reasonable efforts to verify the source and accuracy of the quote. The Participants have not, however, sought or obtained the consent of the quoted source to the use of such quote as soliciting material. This document may contain expressions of opinion and belief. Except as otherwise expressly attributed to another individual or entity, these opinions and beliefs are the opinions and beliefs of the Participants.

CONTACTS:

Verint Stockholders:

Pat McHugh/Bruce Goldfarb/Lisa Patel

Okapi Partners

(212) 297-0720

info@okapipartners.com

Media:

Alexander Samuelson

Neuberger Berman

(212) 476-5392

Alexander.Samuelson@NB.com

About Neuberger Berman

Neuberger Berman, founded in 1939, is a private, independent, employee-owned investment manager. The firm manages a range of strategies—including equity, fixed income, quantitative and multi-asset class, private equity and hedge funds—on behalf of institutions, advisors and individual investors globally. With offices in 23 countries, Neuberger Berman's team is more than 2,100 professionals. For five consecutive years, the company has been named first or second in Pensions & Investments Best Places to Work in Money Management survey (among those with 1,000 employees or more). Tenured, stable and long-term in focus, the firm has built a diverse team of individuals united in their commitment to delivering compelling investment results for our clients over the long term. That commitment includes active consideration of environmental, social and governance factors. The firm manages $323 billion in client assets as of March 31, 2019. For more information, please visit our website at www.nb.com.

Certain statements in this press release, such as those related to changes in a portfolio management team, constitute forward-looking statements, which involve known and unknown risks, uncertainties and other factors that may cause the actual results, levels of activity, performance or achievements of the strategy, or industry results, to be materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward-looking statements. Among other risks and uncertainties are the possibility of differences in the timing or nature of any portfolio manager changes, the adverse effect from a decline in the securities markets or a decline in the strategy's performance, a general downturn in the economy, competition from other closed end investment companies, changes in government policy or regulation, inability of the strategy's investment adviser to attract or retain key employees, inability of the strategy to implement its investment strategy, inability of the strategy to manage rapid expansion and unforeseen costs and other effects related to legal proceedings or investigations of governmental and self-regulatory organizations. As a result, no assurance can be given as to future results, levels of activity, performance or achievements, and neither the strategy nor any other person assumes responsibility for the accuracy.

All information is as of March 31, 2019 unless otherwise indicated and is subject to change without notice. Firm data, including employee and assets under management figures, reflects collective data for the various affiliated investment advisers that are subsidiaries of Neuberger Berman Group LLC. Firm history/timeline includes the history of all firm subsidiaries, including predecessor entities and acquisitions.

This material is being issued on a limited basis through various global subsidiaries and affiliates of Neuberger Berman Group LLC. Please visit www.nb.com/disclosure-global-communications for the specific entities and jurisdictional limitations and restrictions.

The "Neuberger Berman" name and logo are registered service marks of Neuberger Berman Group LLC.

© 2019 Neuberger Berman Group LLC. All rights reserved.

www.nb.com . (PRNewsFoto/Neuberger Berman Group LLC)" alt="Neuberger Berman, founded in 1939, is a private, independent, employee-owned investment manager. The firm manages equities, fixed income, private equity and hedge fund portfolios for institutions and advisors worldwide. With offices in 18 countries, Neuberger Berman's team is more than 2,100 professionals. Tenured, stable and long-term in focus, the firm fosters an investment culture of fundamental research and independent thinking. For more information, please visit our website at www.nb.com . (PRNewsFoto/Neuberger Berman Group LLC)">

SOURCE Neuberger Berman

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.