Image sourced from Unsplash

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

(Monday Market Open) Retail results will likely take center stage this week starting with tomorrow’s April retail sales report and major stores reporting earnings. Additionally, we’ll see housing data indicating how buyers are feeling about the residential market., Investors hope to extend Friday’s rally into today, but equity index futures pointed to a slightly lower open.

Potential Market Movers

Stocks may struggle to attract cash flow today because bond prices were rising in premarket trading. Investors appear to be heading for the safer havens of Treasuries. The higher bond prices pushed the 10-year Treasury yield (TNX) 22 basis points lower. Also, the Cboe Market Volatility Index (VIX) was slightly higher in premarket trading but was still below 30.

China reported weaker-than-expected retail sales and industrial production for April due to recent heavy COVID-19 restrictions and an increase in unemployment. However, there may be some light at the end of the tunnel as Shanghai is planning on a phased reopening of businesses. However, commodity traders may see the reopening as too slow because oil and wheat futures were trading lower in premarket action.

Lower demand for oil in China appears to be offsetting news that Germany plans to end Russian oil imports. gas despite breaking records on wholesale inflation for the third month in a row. Additionally, Finland’s president officially applied for NATO membership, which could aggravate Russian president Vladimir Putin given his previous threats against Finland and Sweden against joining NATO. Sweden is also expected to apply for NATO membership.

European economies continue to struggle in their recovery from the pandemic. Rising European inflation is being exacerbated by the Russia-Ukraine war, lower production, and supply chain issues interfering with recovery.

Some analysts are concerned that this overseas slowdown could be a drag on the U.S. economy. An increasing number of analysts are cutting economic projections for the U.S. and the S&P 500 (SPX). Goldman Sachs (GS) cut its year-end target for the S&P 500 to 4,300 from 4,700, saying there was a 35% chance the U.S. would move into recession in the next two years which could pull the S&P 500 down to 3,600.

However, some analysts are seeing opportunities in growth stocks. Wedbush Securities upgraded Netflix (NFLX) to outperform, sparking a 2.53% rally in premarket trading. JPMorgan (JPM) analysts upgraded several Chinese technology stocks including Alibaba (BABA), Baidu (BIDU), and JD.com (JD).

Reviewing the Market Minutes

Stocks saw a big rally Friday to end another volatile week of trading. The Nasdaq Composite ($COMP) rallied 3.82% on the day. The S&P 500 (SPX) climbed 2.39% and the Dow Jones Industrial Average ($DJI) rose 1.47%. It was a broad advance with NYSE advancers outpacing decliners by nearly 4-to-1. The rally was helped by short covering as bears closed some of their positions going into the weekend.

WTI crude oil futures also rallied Friday, closing 3.7% higher on the day and putting together a three-day, 10.85% rally. Oil was helped by positive news out of Shanghai and Beijing where COVID-19 restrictions may be lifted soon. RBOB gasoline futures also rallied more than 4% on the day for a three-day gain totaling nearly 13%. Gasoline futures finished up more than 33% from their March lows suggesting that commodity traders are still expecting a robust summer travel season despite higher inflation.

Before Friday’s rally, it was a tough week for stocks with only the consumer staples and technology sectors finishing in the green—and just barely. Real estate was the worst sector for the entire week with the Real Estate Select Sector Index falling more than 3.4%. Utilities, consumer discretionary, and health care weren’t far behind with the Utilities Select Sector Index, Consumer Discretionary Select Sector Index, and the Health Care Select Sector Index dropping about 3% respectively.

Real estate and utilities are known for having higher-than-average dividend yields. If these two sectors are losing favor, it could mean that investors don’t expect bond yields to go much higher and are therefore moving over to bonds. While it’s true that the Fed will likely keep raising the overnight rate, at this point, the Fed is playing catch-up with a bond market that has already seen the 2-year Treasury yield trade around the Fed’s target.

The more attractive yields and the safety of Treasuries may help normalize the relationship between stocks and bonds. In the previous few months, we’ve seen stock and bond prices fall at the same time. Historically, the two have moved inversely. If stocks continue to fall, Treasuries may garner more attention which would drive bond prices higher. This is a potential development to keep an eye on.

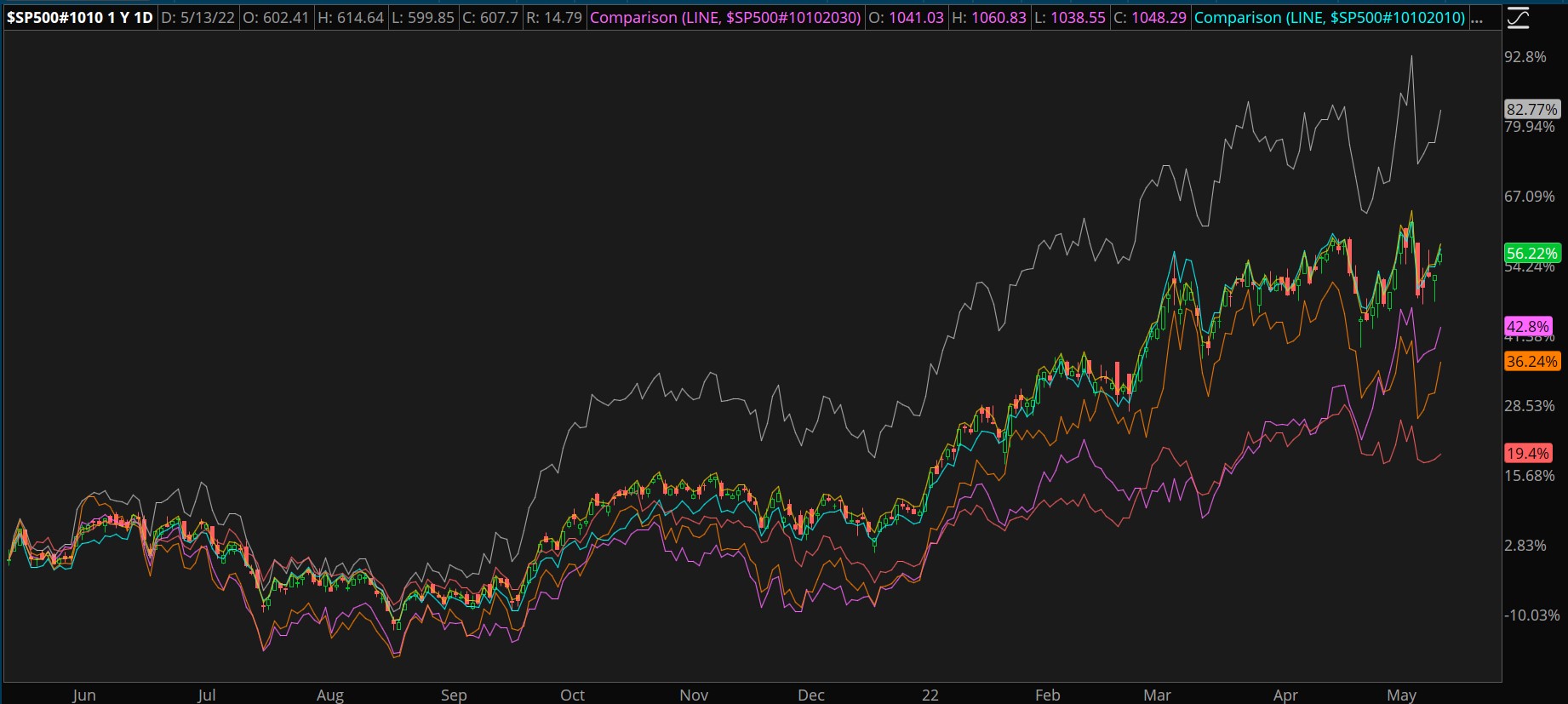

CHART OF THE DAY: OIL PAINTING. The S&P 500 Energy sector index ($SP500#1010—candlesticks) has gained more than 56% in the last year. The sector has been led by the Oil & Gas Exploration & Production ($SP500#10102020—gray) industry group. The Oil, Gas & Consumable Fuels ($SP500#101020—yellow) and Integrated Oil & Gas ($SP500#10102010—blue) groups have kept pace with the sector. While the Oil & Gas Refining & Marketing ($SP500#10102030—pink), Oil & Gas Equipment & Services ($SP500#10101020—orange), and Oil & Gas Storage & Transportation ($SP500#10102040—red) have underperformed. Data Sources: ICE, S&P Dow Jones Indices. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

Greasing the Wheels: In the last year, the energy sector has far outpaced the other sectors. Defensive sectors like utilities and consumer staples have had the second-highest returns but only in the high single-digits. Within the energy sector, oil and gas exploration firms have provided the highest returns over the last year despite a struggle to get financing.

However, The Wall Street Journal reported that BOK Financial BOKF has been working hard to provide loans to oil companies. Billionaire oilman George Kaiser is a majority shareholder in BOKF and has pushed the bank to provide loans to energy companies allowing the bank to take market share from U.S. and European banks. BOKF provided $2 billion in loans in the first quarter of this year.

So far, lending to energy companies hasn’t helped BOKF’s stock price because it’s underperforming the KBW Bank Index (KBX) by about 5% year to date. However, Mr. Kaiser, who now owns 56% of the bank, believes the long-term outlook is better.

Greenwashing: According to Reuters, some Canadian banks have recently come under fire for “greenwashing” loans to oil and gas companies. These banks have allocated sustainability-linked financing (SLF) loans to energy companies because the companies themselves are keeping ESG (environmental, social, and governance) standards even though the purpose of the loan may not be “climate-friendly.” SLF usually comes with a lower lending rate.

The use of SLF loans is a risk to banks because the Bank of Canada has warned that greenwashing could lead to large losses to banks.

Last week, French bank BNP Paribas said it would end financing of oil production in the Amazon rainforest as part of its pledge to reach zero emissions by 2050 and its shorter-term goal to cut emissions by 10% by 2025.

However, there’s still strong demand for oil and gas in Europe, especially as Western countries try to clamp on additional sanctions for Russian oil and gas. Many European countries are now looking to Africa to meet their petroleum needs. But Africa has also experienced a major decline in oil investments, according to S&P Global.

The lack of investment is likely to keep oil supplies tight and prices high.

Homing In: This week, the housing market is going to attract a lot of attention with several key reports. On Wednesday, the Mortgage Bankers Association will report weekly mortgage applications and the Census Bureau will release April building permits and housing starts. On Thursday, the National Association of Realtors will issue the existing home sales report.

Additionally, a couple of big housing-related companies will announce earnings. Home Depot HD is slated for Tuesday and Lowe’s LOW will report Wednesday. Both are important because they supply smaller contractors. Also on Wednesday, Legacy Housing LEGH, which sells and finances manufactured homes, will report earnings. LEGH’s results could provide insight into alternatives for homebuyers who have been priced out of the existing housing market.

Notable Calendar Items

May 17: Retail Sales, and earnings from Walmart WMT and Home Depot HD

May 18: Building permits, and earnings from Cisco CSCO, Lowe’s LOW, Target TGT, TJX Companies TJX, and NetEase NTES

May 19: Philadelphia Manufacturing Index, Existing home sales, and earnings from Salesforce CRM, Applied Materials AMAT, and Kohls KSS

May 20: Earnings from Deere & Co. DE and Foot Locker FL

May 23: Earnings from Advance Auto Parts AAP

TD Ameritrade® commentary for educational purposes only. Member SIPC.

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.