A month ago today, the S&P 500 Index (SPX) sank to three-year lows under 2200 as the economy reeled from the coronavirus pandemic.

The crisis still rages, but the SPX has sure caught fire since then. It closed yesterday just a touch below 2800 and up nearly 28% from last month’s low point, reflecting what appears to be a lot of faith in the ability of Congress and the Fed to prevent a devastating blow to the economy.

In some ways, it’s been devastating already when you think of so many people out of work and struggling to get by. Today’s weekly new jobless claims of more than 4.4 million, the oil market collapse, and companies pulling their guidance all reflect economic upheaval. More rough news came from overseas Thursday as Europe’s April PMI reading slid to 13.5, the lowest on record.

Besides claims—which were a little higher than analysts had expected but below the previous week— earnings continue to be the main focus today. Eli Lilly and Company LLY led things off with a really solid report, beating analysts’ estimates and even raising guidance. Shares bounced in pre-market trading. Intel Corporation INTC comes after the close, and there’s optimism following strong results from other chipmakers like Micron Technology, Inc. MU and Texas Instruments Incorporated TXN. Some analysts following the sector say demand remains strong despite the pandemic.

Getting back to our look at the last month, the SPX remains down 17.5% from its Feb. 19 intraday high and off 13% for the year, but it feels like it could be a lot worse from a market point of view. To put it in perspective, at its weakest level last month, the SPX was down 35% from its high point.

Just because things seem to be improving a little for stocks doesn’t mean anyone can relax. For one thing, analysts continue to chop their earnings estimates for 2020. Looking at the market from that perspective, one could argue that major indices might have come too far, too fast (see more below).

On the other hand, some investors seem to be in a “don’t fight the Fed” mode. With bond yields still near rock-bottom, there isn’t a lot of competition outside of corporate bonds for the dividends many companies continue to pay. All this could favor stocks over the long run, but we’ll have to wait and see how it plays out.

Crude Revival Sparked Midweek Rally

The market’s 5% cumulative losses from Monday and Tuesday got cut in half thanks to Wednesday’s 2.5% gains in the SPX. Thursday begins with the SPX just below 2800.

Information Technology, which suffered a setback earlier in the week, recovered its mojo Wednesday and looked more like the upbeat sector we got to know the first two weeks of April. Semiconductor stocks led the way following solid earnings from TXN, with INTC, Nvidia Corporation NVDA, and Advanced Micro Devices, Inc. AMD among the top performers. INTC presents earnings this afternoon, so stay tuned.

Crude’s comeback helped inject some optimism across the rest of the market, especially in the battered Energy sector. Oil field services firm Halliburton Company HAL helped lead the way with double-digit gains. Crude is up this morning as tensions rise in the Gulf between the U.S. and Iran.

Communication Services was another top dog on Wednesday as social media stocks got lifted by strong earnings from both Netflix, Inc. NFLX and Snap, Inc. SNAP. Strength spread into the rest of the sector to behemoths like Facebook, INc. FB and Alphabet, Inc. GOOGL GOOG, in part because the SNAP earnings helped ease some fears about the chance of advertisers potentially abandoning the social media space. Next week could bring new insight on how advertising is doing online when GOOGL and FB report.

Strength in tech stocks helped the Nasdaq (COMP) outperform competing indices yesterday, while small-caps remained the laggards, with the Russell 2000 Index (RUT) climbing the least. That’s been a theme for a while now and points to a trend where many investors seem to feel more comfortable climbing aboard big, deep-pocketed companies instead of small-cap or value names in these uncertain times.

From Thursday’s perspective, it feels like the crazy action in crude that saw front-month futures turn negative Monday for the first time ever might have really spooked the market. It took a couple of days and the May crude contract going off the board to help get through some of that oil-related volatility, and then Wednesday saw a relief rally in stocks based partly on crude settling down.

The crude market and the U.S. Energy sector are still in deep water, so to speak, but at least there’s a sign of life in the futures market. Prices there remain in contango for crude, meaning the farther-out contracts hold premiums to the nearby June. If that curve starts to flatten, it could spell some trouble as a possible sign of investors losing faith of any sort of “V-shaped” economic recovery.

Headlines Still in Driver’s Seat

A lot of the recent life on Wall Street could reflect hopes of seeing light at the end of the virus tunnel. Talk of some states getting ready to reopen sparked some of that, along with last week’s news of positive early results from a treatment study. The way things are, investors could continue to seize on any uplifting news, including this week’s expected passage in Congress of more help for small businesses. That’s what’s made it hard for bears the last few weeks since that atrocious start to April.

It’s also possible that having the backdrop of earnings helped ease some of the severe volatility of late March. Though earnings have been bad and many companies expect worse in Q2, it feels like a lot that got baked in through last month’s selloff. Remember, the market tends to look far ahead, and some analysts say major indices appear to already be pricing in hopes for better earnings in 2021.

The Fed, which meets next week, already has rates at basically zero. Bonds remain near recent highs and don’t show much sign of coming down. The 10-year yield fell below 0.6% earlier this week but now is back at 0.62%, and tests of the all-time low close not far below that can’t be ruled out amid all the caution. Volatility remains elevated at above 40 for the Cboe Volatility Index (VIX).

This caution reflects in part what most analysts expect will be continued soft data. Today’s big number, besides claims, is March new home sales, coming up right after the open. Durable orders bow tomorrow, with analysts expecting a 10% plunge for March, according to market research firm Briefing.com.

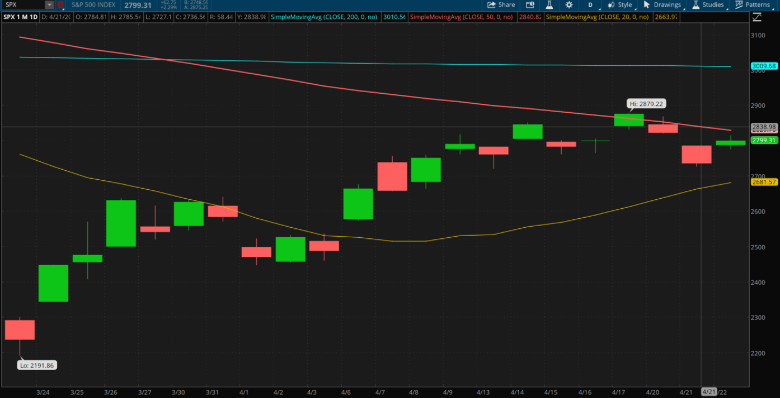

When you look up from here, it’s pretty simple to see some technical resistance for the SPX stretching from around the 50-day moving average near 2830 up to last week’s closing high near 2875 (see chart). A punch through that area would potentially set up a challenge of the 200-day moving average just above 3000, but let’s not get ahead of ourselves. Technical support could rest at the psychological 2750 level, and below that at recent lows recorded this week and last of just below 2730.

CHART OF THE DAY: CHECKING THE RANGE: This one-month chart of the S&P 500 (SPX—candlestick) shows it trending well above the 20-day moving average (yellow line) and closing in on the 50-day moving average (red line), which rests just above Wednesday’s close at around 2830. The SPX continues to trade in a range between the 20-day and 50-day moving averages, but multiple tests of support below 2730 this week and last failed, perhaps putting the market into more positive technical territory. Data Source: S&P Dow Jones Indices. Chart Source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Multiple Matters: It’s looking like many market participants have started to conclude that 2020 earnings will be bad and have turned their attention to 2021, research firm CFRA told investors in a note this week. If forecasters are right about earnings falling in the mid-teens this year, as some now project, that might imply the SPX has room to the downside—assuming you plug in a multiple near the ones the index traded at over the last year or so, say around an 18 price-to-earnings ratio. If investors end up unwilling to assign that kind of multiple, which is historically on the high side, you could argue the market has even more room to fall.

This kind of thing that could be making some people nervous about the recent rally, but cold calculations don’t account for many other factors that could influence the market. Any headlines about a positive bend in the virus curve or possible progress on treatment always have a chance to re-ignite so-called “animal spirits” we saw last Friday. There’s also the chance companies could return in Q2 with improved outlooks. These are some reasons why if you’re bearish, it’s also too hard to get comfortable.

By the way, some would say an 18 multiple is on the high side, but it might make more sense if you consider all the backing the Fed and Congress continue to give the market in the form of low rates, massive balance sheets, and fiscal stimulus. These aren’t normal markets, so one could make the argument that normal multiples aren’t necessarily required, either.

Want a Metal? An under-the-radar economic indicator gained a little ground Wednesday as copper prices jumped from recent lows. Copper is often thought of as a barometer for economic demand because it’s a material used in many electronic devices, including phones. Last month, copper futures touched nearly four-year lows near $2 a pound, but have rallied back to nearly $2.30 and were up 2.5% yesterday. That’s still way below mid-2018 highs above $3.30 when the economy and stocks were rolling along. The February 2020 peak was above $2.88. Sometimes people ignore commodities outside of gold and crude, but copper prices are worth a look because of what they might hint for the technology sector and electric cars, where copper is also a key component.

Seeking Sentiment Sunshine: Markets are all about relationships, and one big relationship is between consumer sentiment and performance. When consumers are pessimistic, so is the market a lot of times. And vice versa, as baseball great Yogi Berra might have said. If sentiment still means anything, it could be worth looking at a poll that came out this week from the Washington Post/University of Maryland. The vast majority of people surveyed said they wouldn’t feel comfortable gathering in groups of 10 or more until the end of June at the earliest. That’s possibly bad news for anyone who’d been hoping for restaurants and other public places to start attracting customers anytime soon, once they can reopen.

The good news, if you can call it that, is 37% of people polled think the economy can recover quickly. OK, 37% isn’t huge, but it counts for something that more than a third of the population is hopeful the economy can bounce right back when this is over. Positive sentiment can mean a lot, but we have to remember that with so many having lost their jobs, a quick return of consumer spending along the lines of last year’s is probably too much to hope for. For more on this, stay tuned tomorrow for April sentiment data from the University of Michigan.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.