After a week that went all over the place and ended up going nowhere, Monday starts with a muted tone as a host of earnings reports awaits. It’s one of the busiest earnings weeks of the season, and info tech might hog the spotlight.

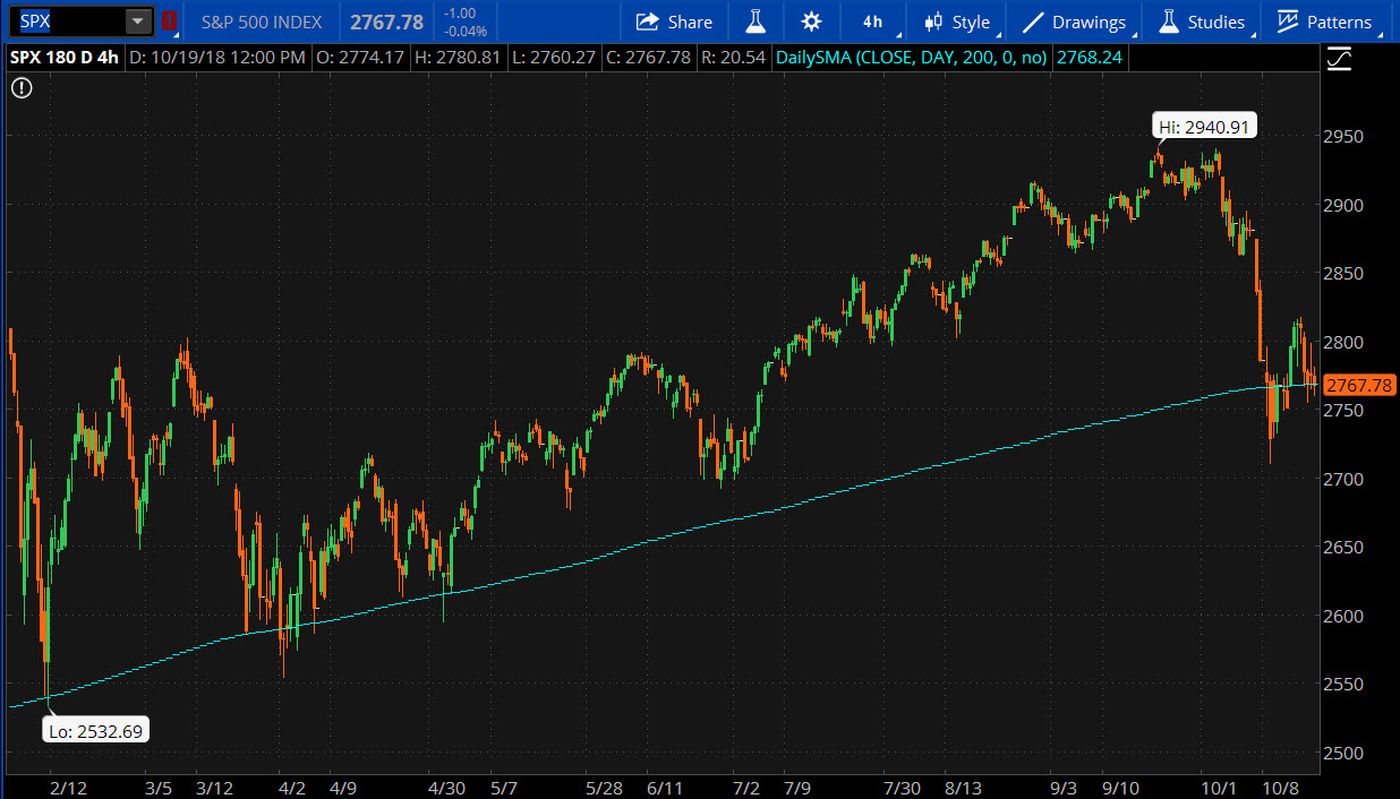

Last week’s market action, and Friday’s in particular, gave both bulls and bears some fodder. The S&P 500 (SPX) had some dramatic ups and downs, but finished the week almost exactly where it started at 2767, which just happens to be one point below its 200-day moving average and even with its year-to-date average. This level could hold some technical significance moving forward, perhaps forming a key support point.

Volatility, meanwhile, remains elevated. The VIX began the week near 19, up from September lows below 12 and perhaps signaling more possible turbulence ahead.

Stocks moved slightly higher in pre-market trading Monday, apparently getting a boost from the second-straight day of big gains in China after the government there took measures to support the market and started talking over the weekend about a possible tax cut, according to media reports. The Shanghai Composite rose 4 percent Monday. Stocks in Europe also climbed amid positive earnings and as concerns about Italy’s economy eased slightly after a less dramatic than expected downgrade from Moody’s. It looks like U.S. stocks might hop on for the ride, judging from action in the futures market.

Before looking at this week’s earnings menu, a look back at Friday’s reports seems in order. Honeywell International Inc. HON beat Wall Street analysts’ earnings-per-share estimate and matched on revenue. Procter & Gamble Co. PG beat estimates on both top-and-bottom lines, and PayPal Holdings Inc. PYPL beat earnings expectations and offered guidance a little above analysts’ forecasts. Meanwhile, American Express Company AXP also beat expectations amid higher card member spending and increased loans.

The AXP earnings might have told investors more good news about the consumer. People seem to be out there spending money, and few if any reports—either data or earnings—conflict with that theory. The AXP results could provide more evidence.

On the earnings watch early Monday, both Halliburton Company HAL and Kimberly Clark Corp. KMB kept the positive results flowing as each beat Wall Street analysts’ estimates. However, Hasbro (HAS) came up a bit short.

Lots of Possible Distraction From Earnings

We’re seeing good earnings, and at the end of the day earnings are what drive the markets. When companies like PG report good earnings and provide good guidance, that tends to be a positive thing for the market overall. Strong earnings can often cause the market to go higher, but there’s a lot of noise right now that might be distracting some investors from company results.

It looks like several ingredients are still in the mix for volatility to continue, though the VIX fell below 19 early Monday. The relatively new wild card is the surge in Treasury yields, with any fresh meaningful rise in rates likely to pressure the market. The benchmark 10-year yield was roughly flat early Monday but still above last week’s lows, resting at 3.19 percent.

Trade worries also haven’t gone away, so any big news on that front could move the market. And we’re getting closer to November elections. Any headlines about candidates and their economic policies could factor into uncertainty.

When people talk about “noise” distracting the markets, all of the items above arguably qualify. Most of those elements are domestic, but overseas issues also are in the mix. There are a lot of political situations around the world, and evidence was all over the place the last few days with China, Italy, and Saudi Arabia. Investors are starting to see little hot pockets of news that can potentially hit the market at any given time, and when you add elections on top of that, it’s no wonder volatility moves up.

Markets are back to a more normal historical volatility level after a year or so of abnormal smoothness, and that could affect the market’s course the rest of 2018. Some analysts say the U.S. market historically tends to rally into the end of the year after midterm elections, though that’s something we’ll have to wait and see about. But even if it happens, it doesn’t seem likely to be a very clean rally. It could be uglier than normal with a lot of back and forth.

Tech, Industrial Earnings on Tap

As for earnings, there are some market leaders scheduled to report in coming days, notably from the industrials and tech sectors. Those include results from Caterpillar Inc. CAT and Boeing Co. BA as well as Microsoft Corporation MSFT, Advanced Micro Devices, Inc. AMD, Twitter Inc. TWTR, Snap Inc. SNAP, and Alphabet Inc. GOOG GOOGL. Amazon.com, Inc. AMZN is scheduled to report alongside these companies.

It will be interesting to see whether executives at the big multinationals have anything to say on the latest developments on international trade issues. Investors might also want to monitor major defense contractors Raytheon Company RTN and Lockheed Martin Corporation LTM in addition to BA to see if they predict any impact on their business from recent tension between the U.S. and Saudi Arabia, a big arms buyer.

Eying GDP, Beige Book

On the economic, inflation, and interest rate fronts, the Fed is scheduled to release its Beige Book this coming Wednesday. Investors may want to scour the summary of anecdotal information on current economic conditions for clues as to what is guiding the thinking of monetary policy makers. Of particular interest could be any commentary about the tightness of the labor market and whether that’s leading to rising wages. Also of possible interest would be any comments on whether the trade war with China could be putting a damper on the economy, which would run counter to the inflationary environment of strong economic performance we’re seeing at the moment.

Speaking of the strong economy, investors are scheduled to get the first government reading on Q3 gross domestic product on Friday, Oct. 26. According to a consensus of economists, expectations are for a reading of a 3.3 percent annualized yearly growth rate. As of Oct. 17, the Atlanta Fed’s GDPNow model estimate for seasonally adjusted annual 3Q GDP growth stood at 3.9 percent.

Either of those readings would be below the 4.2 percent in Q2 but still nothing to sneeze at. Also, an easing of GDP growth would arguably lessen the pressure on the Fed to raise interest rates. While it might not actually alter the trajectory of gradual rate hikes, anything pointing to lower inflation could be a comfort to any on Wall Street who are worrying the central bank might raise rates too quickly for the market’s comfort.

FIGURE 1: BREACHING THE BASELINE? The rally in the S&P 500 Index (SPX) that commenced after the February 2018 meltdown had one commonality: any temporary breach of the 200-day moving average (blue line) was short-lived. Recent moves, however, have many chart watchers on alert. SPX finishes the week right on this long-term technical indicator. Data Source: S&P Dow Jones Indices. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Rising Rates, Inflation, and Bond Investing

Even though rising rates tend to depress the prices of previously-issued bonds, in the long term, higher yields can mean strong income for bond investors over time. Outright losses in the bond market tend to be small, Jeffrey DeMaso, director of research with Adviser Investments, said in a note, pointing to the Bloomberg-Barclays U.S. Aggregate Bond Index, which has never lost more than 5 percent over a calendar year since its inception in 1976 and has only had three negative years, with 2018 potentially being the fourth. Further, intermediate-term U.S. government bonds delivered positive returns each year from 1971 to 1981 even though the yield on the 10-year Treasury rose from around 5.9 percent to more than 15.5 percent, he noted. And bonds tend to rise when stocks falter, giving them their role as a portfolio diversifier.

But rising inflation can eat away purchasing power and negatively affect the real value of bond returns. Factoring in inflation meant a much weaker performance during that 1971-1981 period, when inflation ran as high as 14 percent, DeMaso noted. Thankfully, we’re nowhere near that right now. “Today’s bond investor might be wary of inflation, but they absolutely shouldn’t fear rising rates,” DeMaso said. “Rather, they should welcome higher interest rates for the larger income streams they will produce over time.”

Home Affordability Crimping Sales

Part of the fallout from rising interest rates is that mortgages on homes are more expensive, along with rising costs for steel and lumber. That appears to be crimping the U.S. housing market, whether it’s upstream in the form of building permits for future homes or downstream with the sale of existing homes. In a recent column, we noted how both housing starts and building permits data for September came in under expectations. That was followed by numbers on Friday showing that sales of existing homes came in at a seasonally adjusted annual rate of 5.15 million units. That reflected a month-on-month decline and a miss of the 5.3 million units economists in a Briefing.com consensus had expected.

“Home sales activity was pressured by the limited supply of lower-priced homes and the affordability constraints presented by higher mortgage rates,” Briefing.com noted. Investors are scheduled to get another couple of peeks into the housing market on Oct. 24, with data on new home sales for September due out after a housing price index for August. September pending home sales data is due out the next day.

Information from TDA is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.