There were greater expectations for Friday’s monthly jobs report, but the numbers didn’t deliver. Instead, disappointing data quickly quieted nascent talk of a possible September rate hike by the Fed.

The economy added 151,000 jobs in August, with unemployment flat at 4.9%. Expectations had been for 180,000 jobs and 4.8% unemployment, according to media surveys of analysts. But some analysts had expected 200,000 jobs or more. Job creation was down from a revised 275,000 in July, and the last three months have averaged 232,000.

Hourly wages, another important barometer, rose barely at all, up 3 cents month over month, or 0.12%, but up 2.4% from a year ago. Analysts had expected a 0.2% wage month-over-month rise.

Suddenly, a September rate hike seems far less likely, at least judging from the futures market’s reaction to the jobs data. Immediately after the jobs report, chances of a Fed rate hike in September, as measured by futures at the Chicago Mercantile Exchange, fell to 12%, from 27% right before the jobs number. Chances for a December hike, however, remain at about 50%, futures prices indicate.

Financial stocks, which might typically get a boost from higher rates, slumped in pre-market trading after the jobs data, and the U.S. 10-year Treasury yield, which had spent time above 1.6% earlier this week, traded at 1.57%.

The headline jobs figure of 151,000 was certainly below expectations, and when combined with Thursday’s surprisingly sluggish ISM manufacturing data (see below) and falling auto sales also released Thursday, represents another in a series of tepid data points this week from industry and government. And the job growth seen in August occurred mainly in the food and beverage and social services sectors, not typically areas where people are building careers. Jobs were lost in manufacturing and construction, areas where it would be nice to see gains.

However, it’s too early to panic. Jobs growth did occur in August, just not at the rate expected. Wages did go up, though not as much as analysts had predicted, and continue to move in the right direction. The Fed needed a strong jobs report to consider a September rate hike, and the data didn’t deliver. That puts more pressure on the December time period and the next few monthly jobs reports.

Though today’s jobs report is hogging the early headlines, it’s not the only government data on tap Friday. Later this morning comes July factory orders, which could be worth a look considering Thursday brought weak ISM manufacturing data. Consensus is for 2% growth in factory orders in July, following a drop of 1.5% the previous month, according to Briefing.com.

There’s also a Fed speech on the calendar, with Richmond Fed President Jeffrey Lacker scheduled to deliver remarks at 1 p.m. ET. Fed watchers often label Lacker a “hawk,” so it should be interesting to see if he has any reaction to today’s jobs number.

Oil futures have had their worst week in months, and front-month U.S. crude fell to $43.16 on Thursday, the lowest close since mid-August, before turning it around a little and rising early Friday. The recent descent came amid concerns of growing production and stockpiles, and on talk that OPEC might not agree to any freeze in output. OPEC members have a meeting scheduled for later this month in Algeria.

The correlation between oil and stocks isn’t what it once was, but falling oil often corresponds with weakness in the energy sector, which can indeed affect the overall stock market. Energy stocks in the S&P 500 (SPX) are down more than 1.75% since last Friday, and some of energy names posting losses Thursday included ConocoPhillips COP, Exxon Mobile Corporation XOM, and Hess Corp. HES.

Falling productivity and manufacturing activity accompanied by higher wages potentially make the Fed’s job more difficult. If manufacturing and productivity are sagging, higher rates wouldn’t necessarily be the correct prescription. At the same time, rising wages potentially point to inflation growth, and while the Fed wants inflation to reach its 2% benchmark, too much inflation wouldn’t be good either. The Fed typically raises rates to fend off economic growth that’s too frothy. Looking at these data along with Friday’s jobs number, it’s clear the Fed has its work cut out for it, but a September hike might be less likely with jobs coming in below expectations.

Checking on China: Worries about China’s economy have stalked the markets over the last year, but recent data, notably Thursday’s August purchasing manager’s index (PMI) that measures Chinese manufacturing, offered some hope. The PMI came in just above analysts’ consensus estimate at 50.4, with anything over 50 marking expansion, and represented the highest reading in nearly two years. However, analysts quoted by the media after the report said China’s economy remains at risk from a number of factors, including overcapacity, weak external demand, and high levels of corporate debt. It’s also worth noting that the somewhat bullish August reading came after notably weak July data. The Shanghai composite is down about 13.5% for the year but up 16% from its January low.

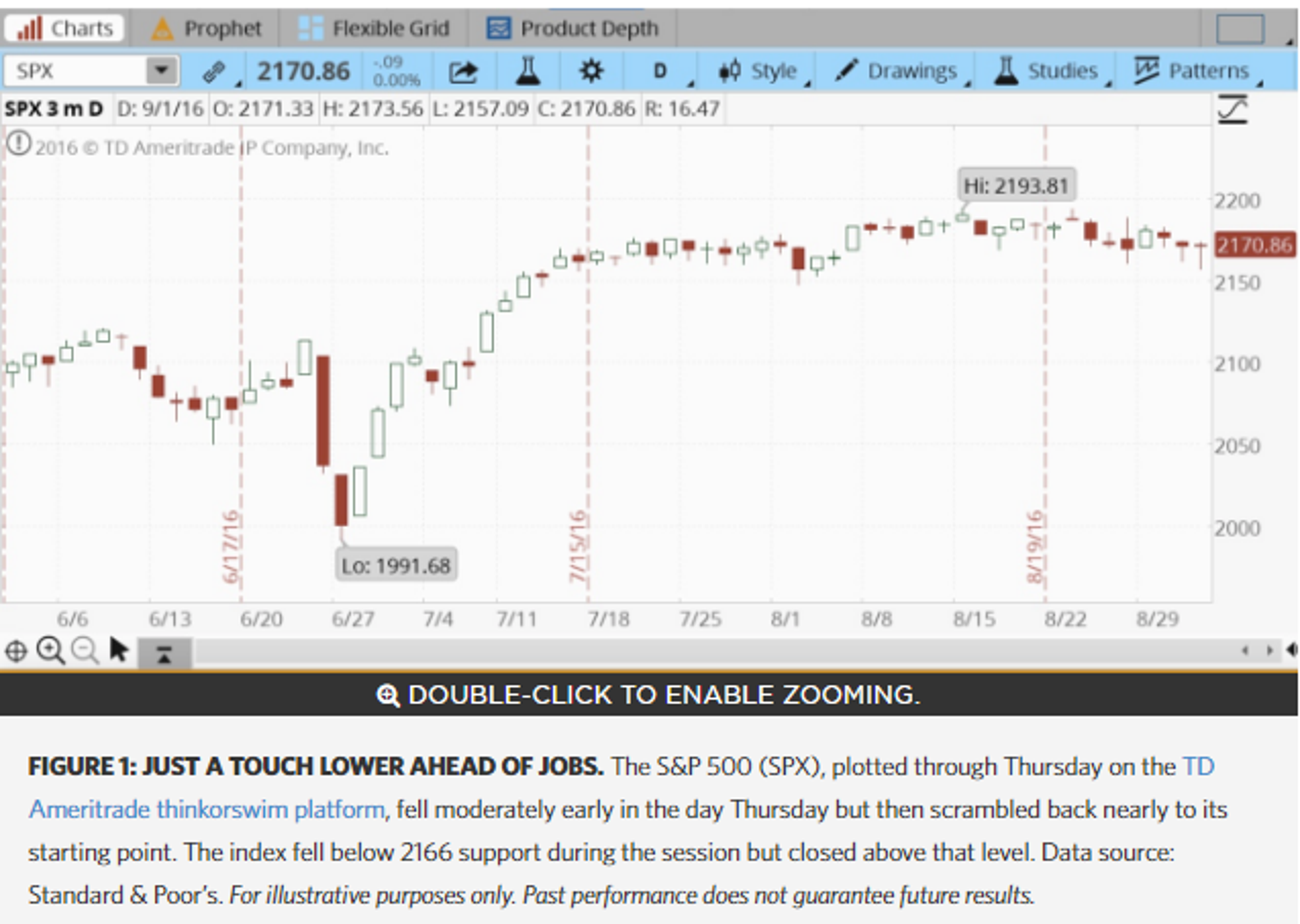

Looking Ahead to Tuesday: Here’s something to ponder: The stock market has risen the day after Labor Day in 14 of the last 21 years. Remember, though, that past performance is no guarantee of future results. Kind of interesting, though, especially since history shows that September tends to have the worst monthly performance for both the Dow Jones Industrial Average (DJIA) and the S&P 500 (SPX). September can also be a more volatile month than sleepy August, so it could pay for investors to stay on their toes. The market is down a bit from its recent peak, but closed Thursday still within 1% of the all-time SPX high, meaning it’s a good idea to continue exercising caution.

Inclusion of specific security names in this commentary does not constitute a recommendation from TD Ameritrade to buy, sell, or hold.

Market volatility, volume, and system availability may delay account access and trade executions.

Past performance of a security or strategy does not guarantee future results or success.

Options are not suitable for all investors as the special risks inherent to options trading may expose investors to potentially rapid and substantial losses. Options trading subject to TD Ameritrade review and approval. Please read Characteristics and Risks of Standardized Options before investing in options.

Supporting documentation for any claims, comparisons, statistics, or other technical data will be supplied upon request.

The information is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade. Clients must consider all relevant risk factors, including their own personal financial situations, before trading.

TD Ameritrade, Inc., member FINRA/SIPC. TD Ameritrade is a trademark jointly owned by TD Ameritrade IP Company, Inc. and The Toronto-Dominion Bank. © 2016 TD Ameritrade IP Company, Inc. All rights reserved. Used with permission.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.