The S&P 500 (SPX) logged a sixth straight weekly gain even after a challenging Friday—a streak that most analysts think could have some backbone. Challengers could peck at those gains, however, spurred by uncertainty for Federal Reserve aggressiveness after a stronger-than-expected October job report.

The Fed is watching hiring gains but is especially sensitive to wage-driven inflation. This week’s consumer-focused economic reports could reveal if healthier paychecks are being spent.

Too Good?

Friday brought initial gains for stock prices and Treasury yields (moving the opposite of falling bond prices) following a report that showed a stronger-than-expected addition of 271,000 U.S. jobs in October. That figure marked the biggest gain of the year, pushing the unemployment rate down to a seven year-low of 5%. The underemployment rate—which includes part-time workers who’d prefer a full-time position and people who want to work but have given up looking—fell to 9.8%, the lowest since May 2008.

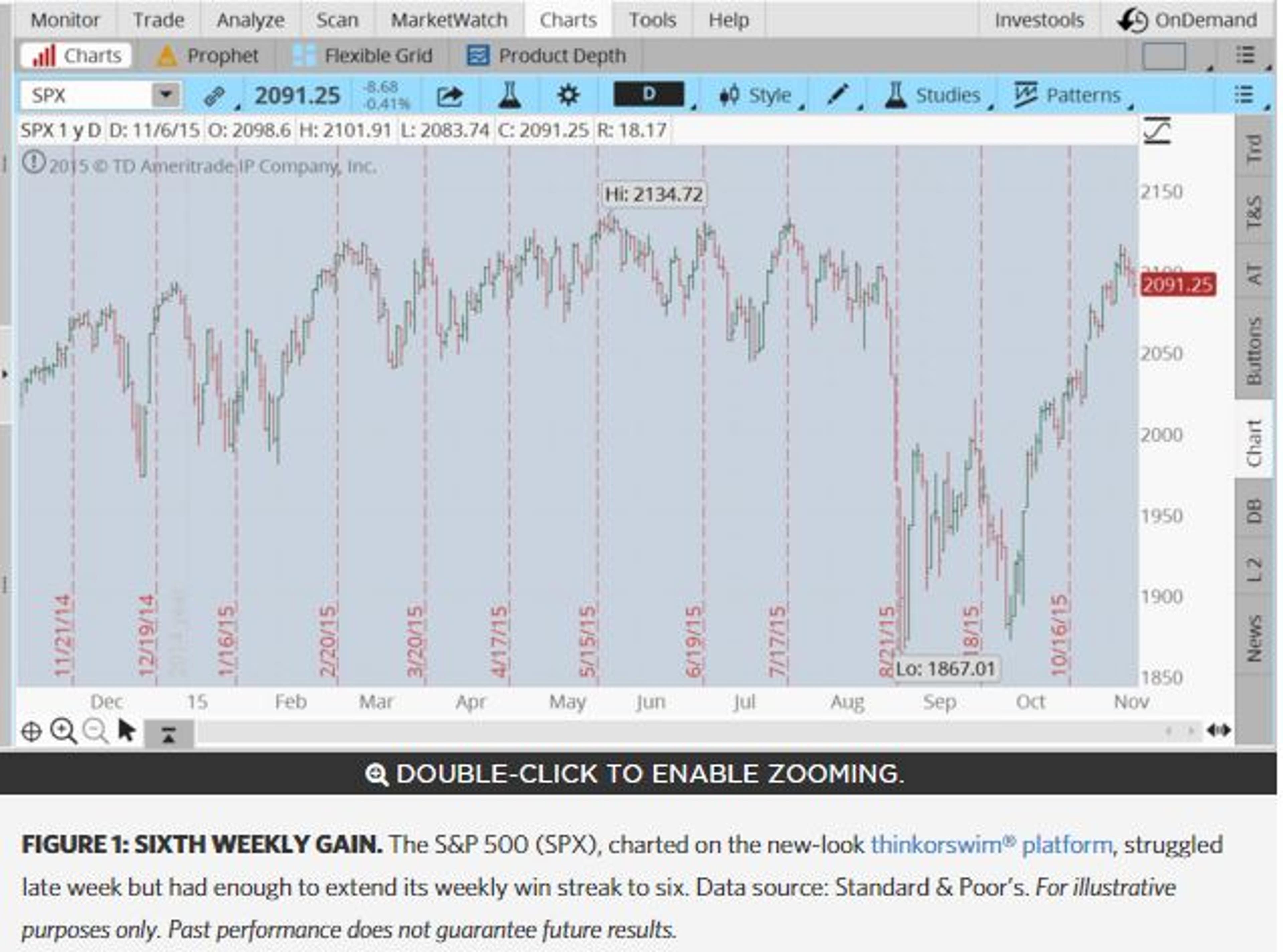

But broader stock averages turned more defensive later Friday, pushing the SPX back below the psychologically significant 2100 line (figure 1). The driver? Fears that the Fed response could be too aggressive and choke off an economy that could be finally producing evenly. Financial shares gained as higher rates are typically positive for banks; biotech lifted the NASDAQ Composite.

Finally, Some Money to Spend?

The long-awaited increase in worker pay might finally be here. Pay—and the impact that a lack of pay increases has had in capping inflation—has created one of the biggest mysteries of the recovery. It’s challenged a Federal Reserve trying to juggle the competing push-and-pull of the economy—the global economy, in fact.

U.S. hourly pay has been stagnant for five years despite the creation of nearly 12 million new jobs and a 5% national unemployment rate. Friday’s report showed that the average hourly wage paid to American workers rose 0.4% in October as the typical worker earned an average $25.20 an hour in October, up 9 cents from the prior month. From October 2014 to October 2015, hourly wages rose 2.5%, the best year-over-year gain since the U.S. exited recession in June 2009. Annualized increases in pay had stuck to a tight range of 2.2% or less for the past five years.

This all means that consumer spending measures could gain increased importance for investors. Macy’s M is out with its Q3 earnings report on Tuesday. Its performance is typically impacted by domestic demand fluctuations and job market strength, but also by currency changes, as a stronger dollar can sap tourist spending at its flagship New York store. M is among the several retailers, including Wal-Mart WMT, Home Depot HD, Target T, Best Buy BBY, and Tiffany TIF, throughout November. Their results matter but what could hold more sway with Wall Street is their commentary about holiday spending.

The Commerce Department’s retail sales report, which has continued to trend below pre-recession levels, is due for release on Friday (see the full economic report schedule below). Traders are likely to see what quality of spending is taking place. Auto sales, for instance, have improved: October’s car sales surged to an annualized pace of 18.12 million units—the fastest pace since July 2005.

Expectations on the Rise

Increased consumer activity could factor into Fed decision-making next month. The CME Group’s FedWatch Tool, calculated based on pricing in the Fed funds futures market, shows traders are pricing in about a 70% shot for a rate hike in December according to market pricing on Friday. That’s up from the 35% odds priced in right after the Fed took a pass on an October rate change but issued a statement entertaining the thought of a December hike. Traders in this market see a 73% chance for a hike in January and a 85% shot for a hike in March, according to market action through midday Friday.

Inclusion of specific security names in this commentary does not constitute a recommendation from TD Ameritrade to buy, sell, or hold.

Market volatility, volume, and system availability may delay account access and trade executions.

Past performance of a security or strategy does not guarantee future results or success.

Options are not suitable for all investors as the special risks inherent to options trading may expose investors to potentially rapid and substantial losses. Options trading subject to TD Ameritrade review and approval. Please read Characteristics and Risks of Standardized Options before investing in options.

Supporting documentation for any claims, comparisons, statistics, or other technical data will be supplied upon request.

The information is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade. Clients must consider all relevant risk factors, including their own personal financial situations, before trading.

TD Ameritrade, Inc., member FINRA/SIPC. TD Ameritrade is a trademark jointly owned by TD Ameritrade IP Company, Inc. and The Toronto-Dominion Bank. © 2015 TD Ameritrade IP Company, Inc. All rights reserved. Used with permission.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.