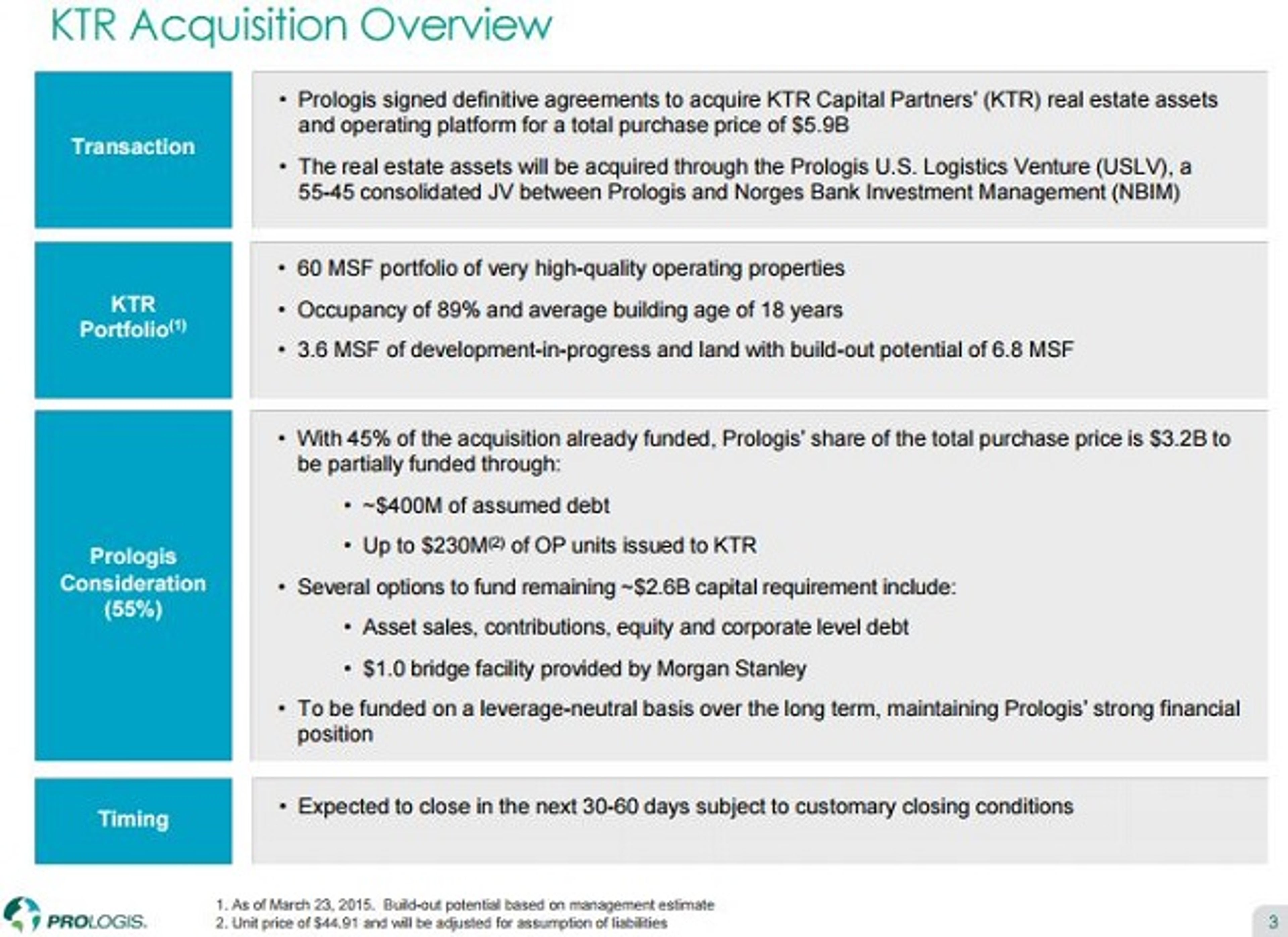

Global industrial REIT Prologis Inc PLD announced a $5.9 billion portfolio acquisition from KTR Capital Partners prior to its Q1 2015 earnings call Monday before the opening bell.

U.S. industrial developer KTR Capital is managed by the former Keystone Property Trust team, who sold the former NYSE listed REIT for $1.6 billion in 2004.

Prologis is taking the lead in a 55/45 JV with Norges Bank Investment Management (NBIM) in the Prologis U.S. Logistics Venture. The same $890 billion Norwegian sovereign wealth fund had previously invested in a Prologis European industrial portfolio back in 2012.

How This Purchase Stacks Up

Sporting a market cap of $23.3 billion, Prologis already dominates the U.S. industrial REIT landscape, with $7 billion cap Duke Realty Corp DRE being the only other U.S. industrial REIT with a market cap larger than the KTR portfolio asset value.

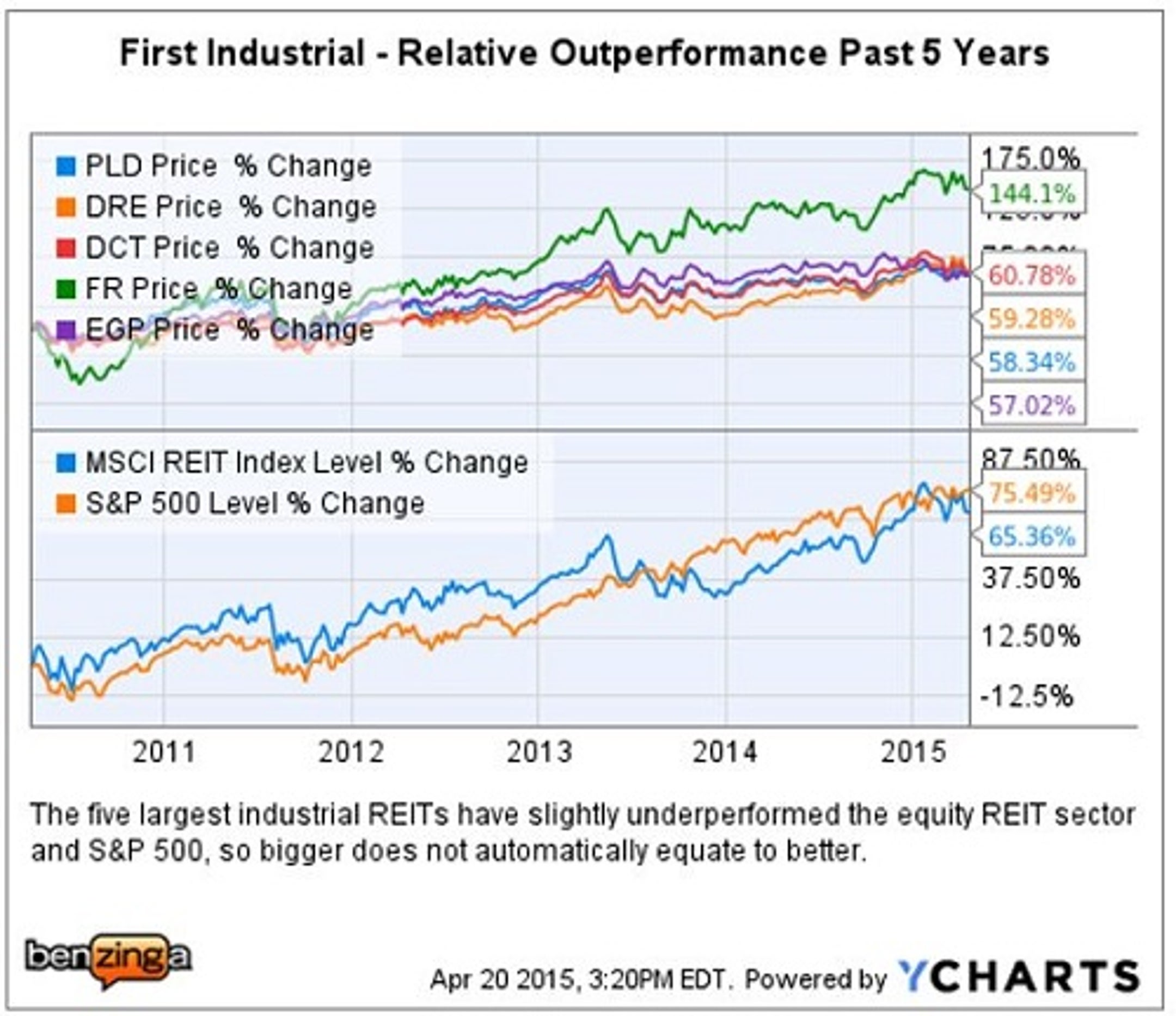

Tale Of The Tape – Big Five Past 5 Years

One of the challenges that all REITs face as they grow in size is finding accretive transactions large enough to move the needle.

However, this JV acquisition with NBIM was hefty even by Prologis standards, and based upon this, company presentation will immediately be accretive to earnings.

5 Slides – Prologis Acquisition Highlights

In addition to the 60 million square feet of operating properties being acquired by the JV, there are 10 development projects underway, totaling 3.6 million SF.

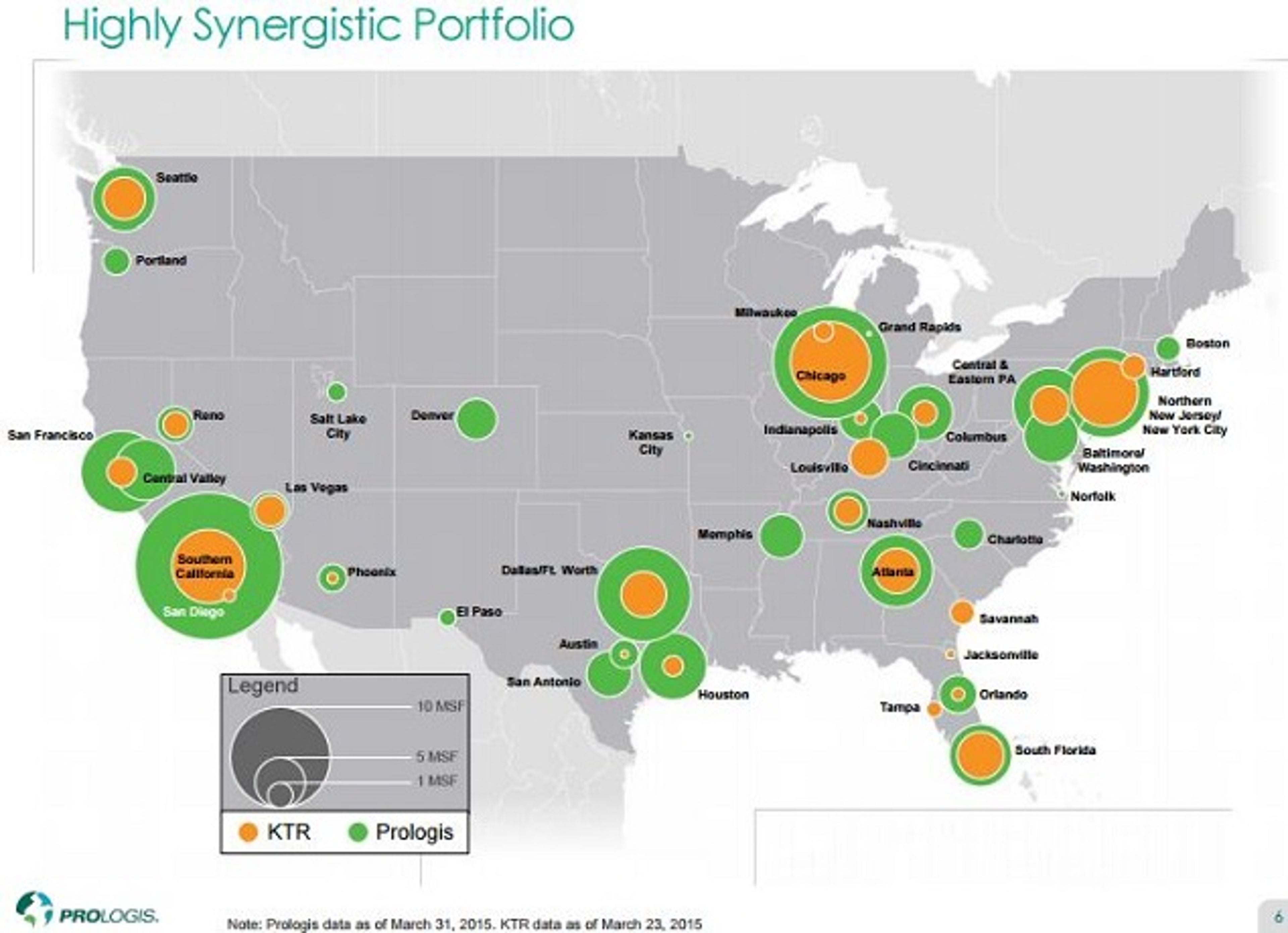

Notably, 65 percent of the development projects are located in California. The completion of all projects under active development is anticipated by Q1 2016, leaving a land-bank that can support an additional 6.8 million SF of future development on behalf of the Prologis/NBIM venture.

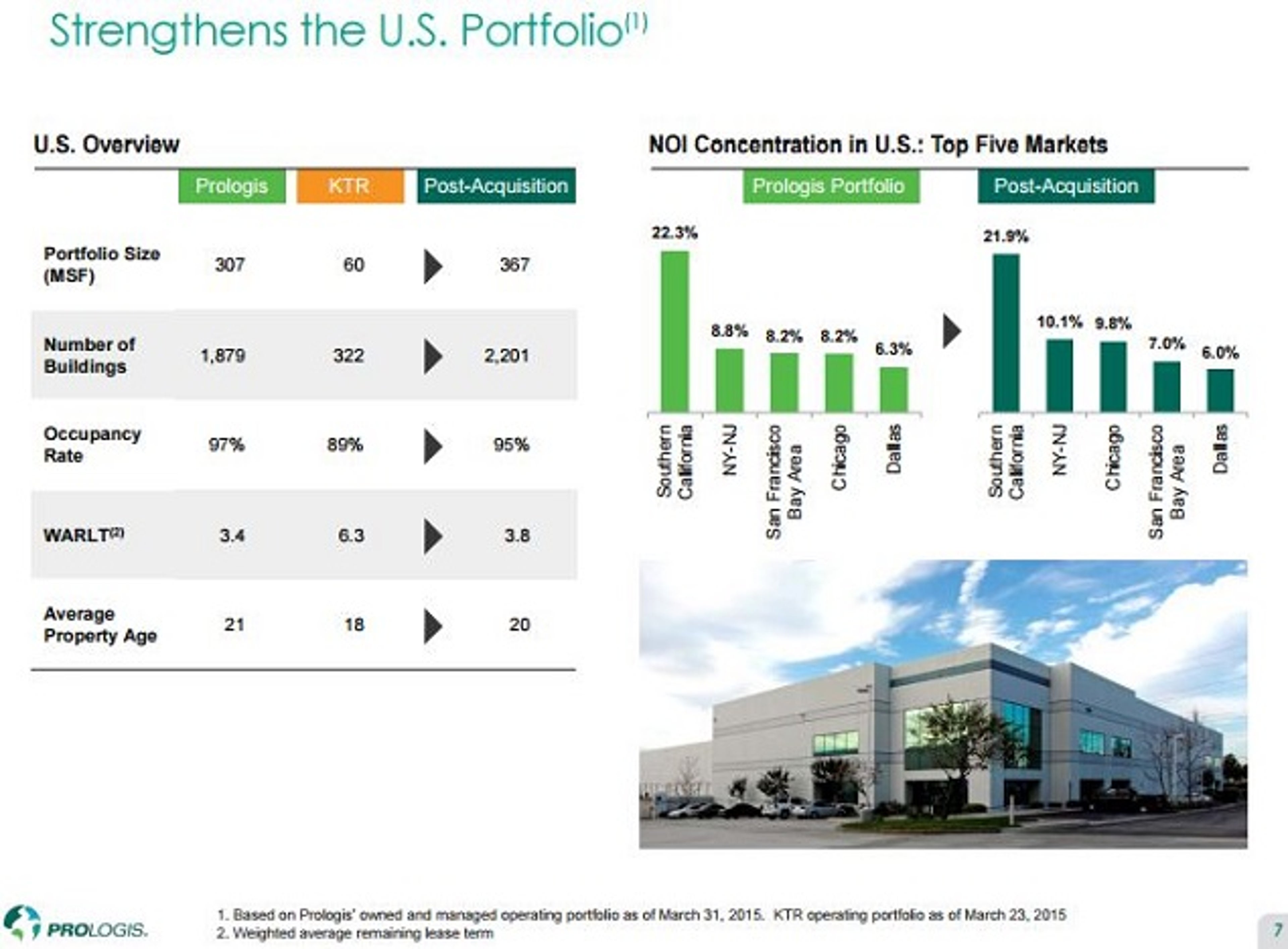

The weighted average remaining lease term (WARLT) of 6.3 years on the KTR portfolio is almost twice as long as the existing Prologis 3.4 year average; however, it only moves that needle up to 3.8 years when combined.

The KTR portfolio 89 percent occupancy is 800 bps less than the Prologis existing portfolio, which results in a pro-forma 95 percent average for the combined portfolio at closing.

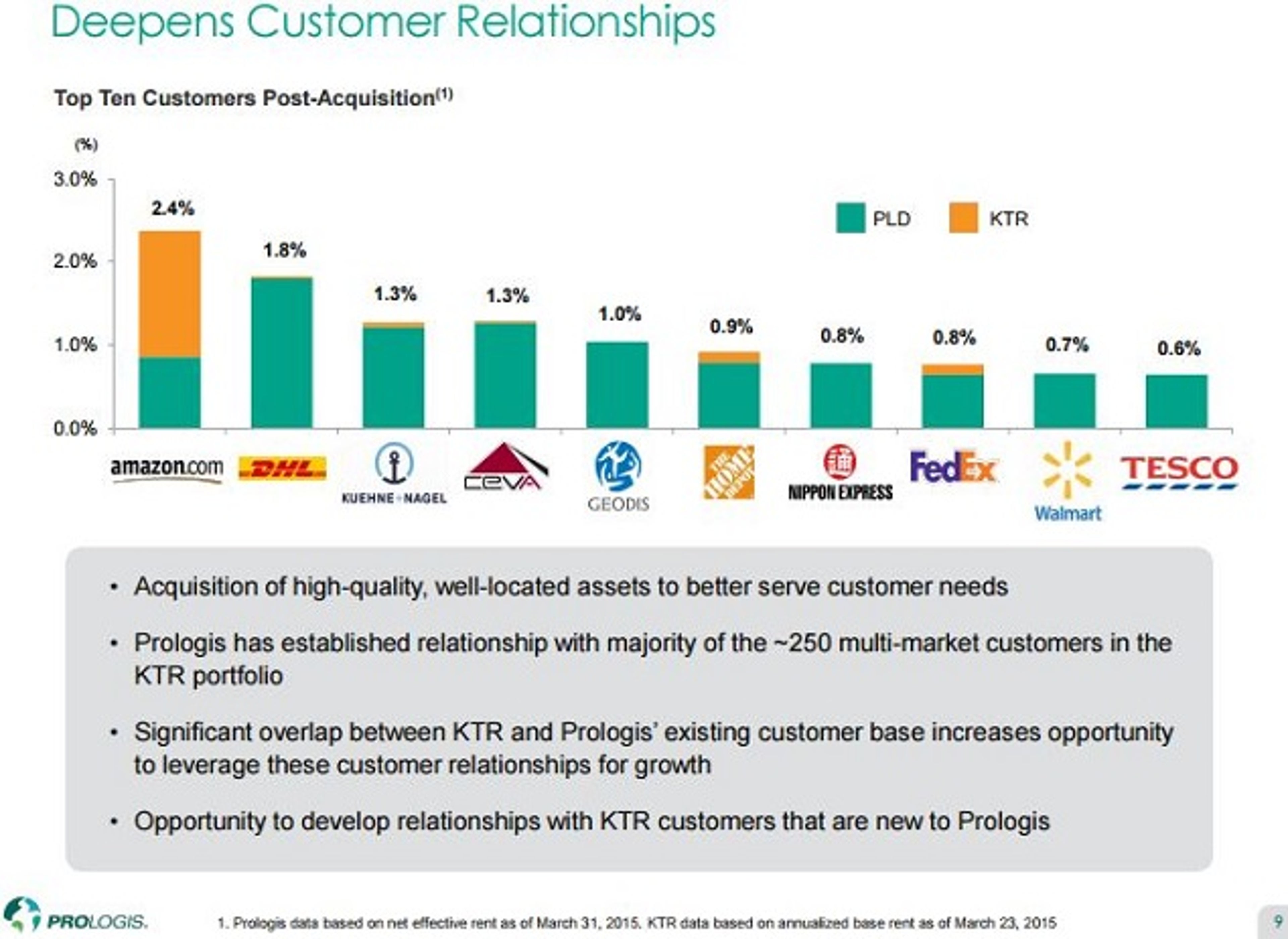

Prologis having existing relationships with the vast majority of the KTR tenants bodes well for future lease-up and provides an opportunity for organic growth after closing.

Reduces FX Headwinds

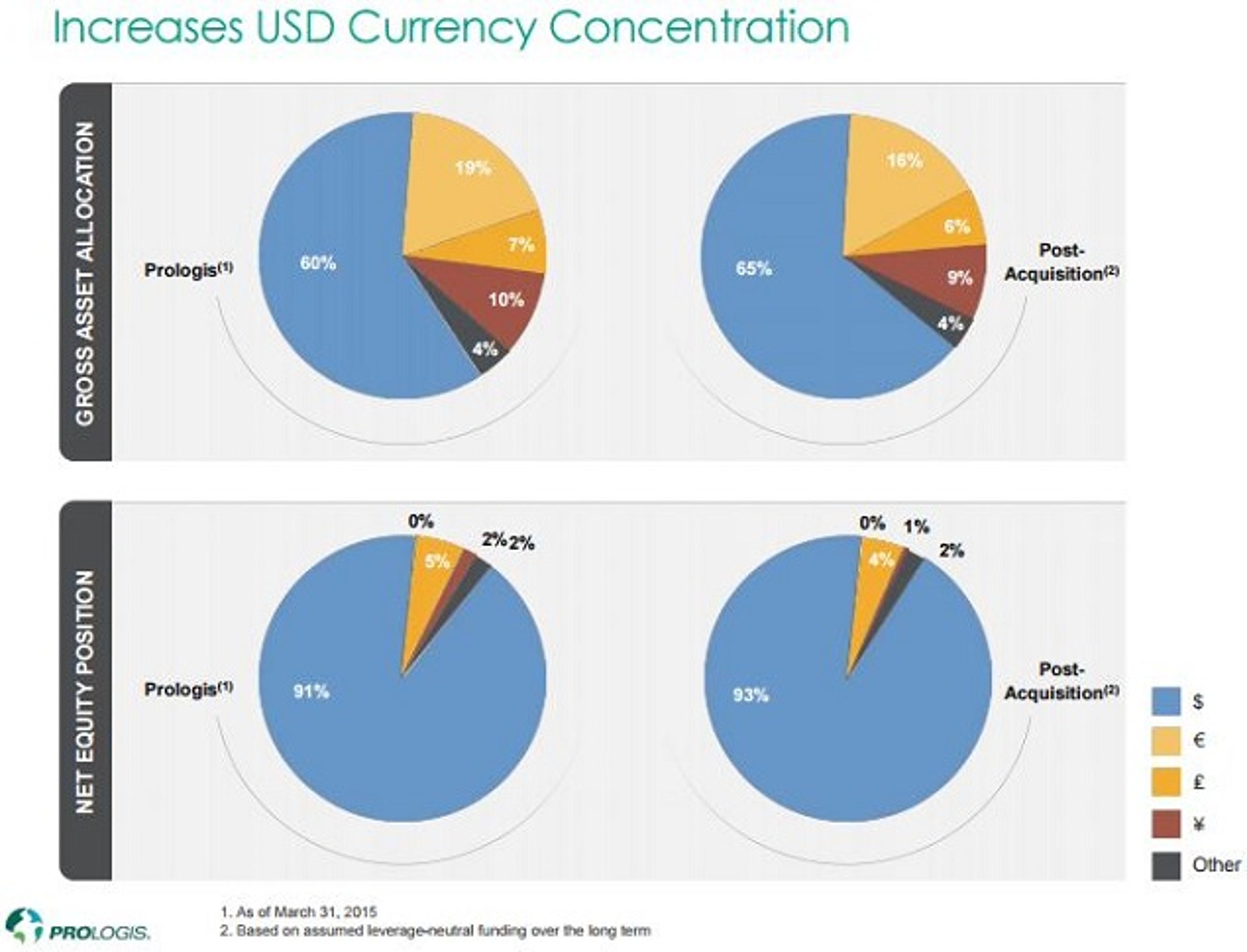

Prologis increases its exposure to top U.S. industrial markets while reducing its exposure to FX headwinds, which can dilute cash available for distribution.

The Norges fund gets to diversify its industrial real estate holdings further by investing in the faster growing U.S. economy.

Investor Takeaway

Prologis projects this deal to immediately add $0.05 to core FFO, assuming a 30 to 60 day close, and expects annual stabilized core FFO to be approximately $0.14 per share.

Prologis expects this deal to be funded in a leverage neutral fashion to its balance sheet and has several means at its disposal to fund its part of the JV asset purchase.

Prologis ability to team up again with the huge Norway sovereign wealth fund on a deal of this magnitude in the U.S. is certainly a positive development for Prologis investors.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.