The Crude Oil futures and options markets are the most liquid and actively traded global commodities contracts in the world. With Weekly Options on WTI Crude Oil Futures expiring on Friday each week, CME Group provides market participants with a flexible tool to fine tune their crude oil market exposure. The addition of Weekly Options to a trader’s hedging strategy offers a low-cost tool to mitigate risk associated physical or financial positions.

Key features

- Expire every Friday and exercise into the active futures contract

- Automatic exercise with no contrary instructions

- Flexibility to manage short-term volatility and risk

- Precision timing to target specific market movements or events like OPEC meetings

- More flexible hedging at a lower premium

Figure 1. WTI Weekly Options Performance

Crude Oil Weekly Options – Storage Applications

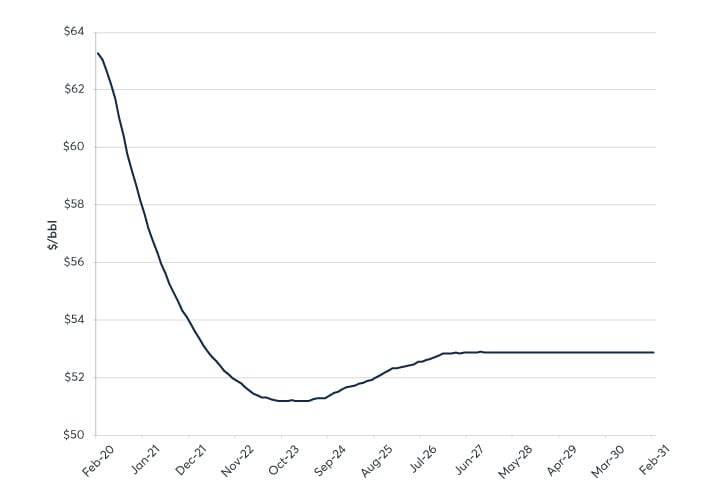

Crude oil options trading is applicable to market participants with exposure to crude oil price volatility. Since crude oil prices are settled to a new price each day, using a specific series of days is useful to fit a given pricing window for both buyers and sellers. Scenarios in which traders and producers require short-term storage can provide opportunities for utilizing Weekly Options strategies. The forward term structure in crude oil is largely influenced by supply/demand, storage costs, and production estimates. The shape of the forward curve has important implications for inventory management. If the market is backwardated (Figure 2), then the current value of inventory is greater than the deferred future price. In this environment, producers and traders are unlikely to store product for long-periods of time and may have a need to hedge short-term storage exposure over the course of 1-4 weeks. Depending on a trader’s short-term storage strategy, they will need to reduce intramonth price exposure in the case of a market moving event. In Example 1 we will look at utilizing Weekly Crude Oil options to hedge physical price exposure during an adverse global event.

Figure 2. WTI Crude Oil Futures Term Structure (1/6/2020)

Crude Oil Weekly Option Example 1: Coronavirus Outbreak

A Crude Oil trader purchases a cargo and intends to store it until a buyer is procured. The trader wishes to hedge his price exposure over the coming week as he finds a buyer. For hedging purposes, the trader implements a collar strategy which includes purchasing an at-the-money Weekly put option and selling an out-of-the-money Weekly call option with the same expiry. This strategy allows the trader to hedge downside risk while reducing the cost of the strategy by selling the call. The trader will have limited upside set at the strike price of the call but has partially offset the cost of the hedge. Additionally, the trader’s expiration timeline is precise and tailored to his specific short-term needs.

Date: 1/6/2020

WTI Futures Feb20 Price: $62.00/bbl

Physical Position: 100k bbls

Collar Strategy:

Buy 100 Weekly Puts @$62.00 for $0.40 premium

Sell 100 Weekly Calls @$65.00 for $0.30 premium

On Monday 1/6/2020 the trader initiates a collar using Weekly Options that expire on Friday 1/10/2020. At expiry, the underlying WTI Futures Feb20 price drops and settles at $59.00/bbl following World Health Organization reports that the coronavirus has broken out in Wuhan, China. The trader’s physical position of 100,000 bbls realizes a $300,000 loss in value while in storage. However, because the trader has used Weekly Options to construct a collar hedge, he has offset the loss with a $290,000 gain generated through his options position ($300,000 gross profit - $10,000 cost to implement the strategy).

Figure 3. Collar Hedge Using Weekly Options

Crude Oil Weekly Options - Downstream Applications

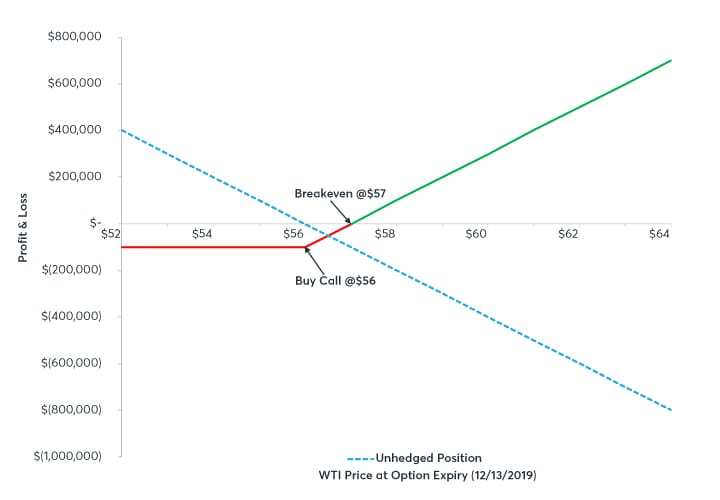

Crude Oil Weekly Option Example 2: Refinery Risk Management

A refiner has committed to buy 100,000 bbls of crude oil off the local pipeline in two weeks. The barrels will price the week of delivery and the refiner has concerns that markets may rally ahead of the pricing week. As a result, she purchases an at-the-money Weekly call option that is available for the exact week of the delivery at a cost well below the monthly option that expires the following week. She is comfortable locking in a price of $57.00/bbl using this option strategy. On the Wednesday before the pricing week, the market experiences a sizable and unexpected draw in crude oil inventories reported by the EIA, pushing the price of WTI up 4%. The refiner’s P/L using a Weekly call option can be seen below.

Date: 12/2/2019

Jan20 WTI Futures Price: $56.00/bbl

Committed Physical Exposure: 100k bbls

Long Call Hedge Strategy:

Buy 100 Weekly Calls @ $56.00 for $1.00 premium

By Friday 12/13/2019, Jan20 WTI Futures price rises and settles at $60.00/bbl following the previous week’s bullish EIA crude oil inventory report. The refiner purchases 100,000 physical bbls @ $60.00/bbl for $6,000,000 ($400,000 more than expected on 12/2/2019 when WTI Futures were $56.00). Profit from the Weekly call option hedge at expiry is $300,000 ($400,000 profit - $100,000 premium), leading to a reduced net payment of $5,700,000 or $57.00/bbl. The refiner leveraged the time and cost benefits associated with the Weekly call option to effectively hedge her supply cost against an unexpected move higher in futures prices

Figure 4. Call Hedge Using Weekly Options

Crude Oil Weekly Options - Upstream Applications

Crude Oil Weekly Option Example 3: Producer Hedge

A producer is required to hedge 70% of his supply on a monthly basis and is hedging his August 2019 production using WTI Futures. In the last week of July, the producer starts to see higher than expected yields in his wells and projects an increase in volume, leading to an underhedged position come August. The producer decides to utilize short-dated Weekly put options to provide some price certainty around the expected increase in volume and retain his 70% hedging covenant while he finds a buyer. To hedge his current expected production of 1,000,000 bbls and meet the 70% hedging requirement, the producer sells 700 Sep19 WTI Futures contracts (700,000 bbls). Late in July, well production is projected at 1,200,000 bbls, leaving 140,000 bbls unhedged (70% x 200,000 bbls). The producer is worried about the impact of certain geopolitical and economic announcements set for the week of July 29, 2019 and implements a Weekly bear put spread strategy that expires August 9, 2019 to hedge downside price risk. The bear put spread includes selling a lower strike put option and buying a higher strike put option with the same expiry in order to hedge against bearish market expectations. By purchasing a put spread instead of an outright put, the producer reduces the cost of the options hedge.

Date: 7/29/2019

Sep19 WTI Futures Price: $56.00/bbl

Expected Physical Exposure: 140k bbls

Bear Put Spread Strategy:

Sell 140 Weekly Puts @ $53.00 for $0.20 premium

Buy 140 Weekly Puts @ $56.00 for $0.70 premium

From 7/29/2019 to 8/9/2019, Sep19 WTI Futures fall approximately 6% to $53.00/bbl due to additional U.S. tariffs on Chinese goods and bearish remarks from the Fed Chairman regarding the likelihood of future rate cuts. 70% of the producer’s additional well supply loses $420,000 in value after the two-week period but is offset by a $350,000 gain from the option strategy ($420,000 profit - $70,000 premium). The producer is now able to sell the additional 140,000 bbls at a net price of $55.50/bbl.

The producer can replicate this strategy each week throughout the month to maintain his 70% mandate.

Figure 5. Bear Put Spread Hedge Using Weekly Options

Summary

Oil prices are highly elastic with respect to various fundamental factors including economic data, geopolitical risk, and unanticipated supply/demand issues. Unpredictable changes in any of these factors can have an impact on unhedged financial and physical crude oil positions. WTI Weekly options provide a deep pool of liquidity for market participants to not only express their views on market moving events but also manage the volatility associated with them. Participants can leverage lower option premiums coupled with greater precision to implement efficient and timely hedging strategies.

Figure 6. WTI Crude Oil Weekly Options – Contract Specifications

|

CONTRACT SPECIFICATIONS |

|

|---|---|

|

CONTRACT |

WTI Crude Oil Weekly Option |

|

COMMODITY CODE |

LO1-LO5 |

|

UNDERLYING FUTURES |

Light Sweet Crude Oil Futures (CL) |

|

RULE CHAPTER |

1011 |

|

LISTING PERIOD |

Weekly contracts listed for 4 consecutive weeks. |

|

CONTRACT SIZE |

1,000 barrels |

|

SETTLEMENT TYPE |

Deliverable into futures |

|

TERMINATION OF TRADING |

Trading terminates on Friday of the contract week. |

|

MINIMUM PRICE TICK |

$0.01 per barrel |

|

VALUE PER TICK |

$10.00 |

|

BLOCK TRADE MINIMUM THRESHOLD |

10 contracts |

|

TRADING AND CLEARING HOURS |

Sunday - Friday 6:00 p.m. - 5:00 p.m. (5:00 p.m. - 4:00 p.m. CT) with a 60-minute break each day beginning at 5:00 p.m. (4:00 p.m. CT) |

To learn more about futures and options, go to Benzinga’s futures and options education resource.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.