Want to jump straight to the answer? VSP Vision Insurance is one of the most popular vision coverage providers in the nation. Learn more here.

You might think vision insurance is included with health insurance coverage but many health plans don’t cover glasses, contacts or eye exams. A separate individual vision plan can bridge the coverage gap, but is vision insurance worth it?

Key Takeaways: Is Vision Insurance Worth It?

- It may be worth it when you need to cover your entire family, you have Medicare, have health concerns or have little cash saved.

- It may not be worth it if you don't need frames, you only have access to discount plans or you have a health savings account or flexible spending account.

Overview: Vision Insurance

Eye care can be costly. Vision insurance can help reduce vision-related healthcare costs by covering part of the expenses for key services, such as:

- Eye exams

- Eyeglass frames

- Eyeglass lenses

- Lens options

- Contact lenses

- Discounts on LASIK or PRK

For individual vision plans, you’ll pay as low as $13 a month for a plan. More affordable plans usually cover an eye exam or glasses, but not both.

Vision insurance companies keep pricing affordable by using an approved provider network. If you have a favorite eye doctor, check to see if your doctor is part of the network before purchasing vision insurance. Out-of-network services may be costlier or may not have coverage at all. Often, for in-network claims, the doctor bills the vision insurance company directly, simplifying the process. Your copayment, if applicable, is paid directly to the service provider at the time of service.

Unlike other types of health insurance, vision insurance plans don't have a deductible. Instead, you can expect to make a copayment for many of the covered services, although some services may be offered without a copayment. In many cases, copayments are in the $15 to $25 range but can climb higher for certain items, particularly lens options, like anti-glare treatment, scratch-resistant lenses or impact-resistant lenses.

Vision insurance plans are offered as a contract, typically with a minimum 12-month commitment. You'll usually have the option of paying for 12 months of coverage all at once or splitting your premium into 12 monthly payments. Some plans may offer an additional discount of about 5% if you pay for the entire year in a single payment.

Plans for vision care don’t cover all eye-related needs. Typically, they do not cover more in-depth exams, such as those done by an ophthalmologist, who provides specialized eye care or performs surgeries. Elective procedures, such as LASIK or PRK surgery aren't covered by vision insurance plans. Instead, it's common to find generous discounts for these services bundled with your vision insurance coverage.

In many cases, a vision insurance plan can help you save money on the cost of glasses or contacts and eye exams. Depending on your vision care needs you may end up saving more money than paying out of pocket.

When Vision Insurance is Worth It

Whether a vision insurance plan is a good investment for you or your family can depend on several factors. Plans can be priced as low as $13 for individual vision plans and up to $40 per month or higher for family plans, so it’s important to weigh your purchase decision for vision insurance.

You Need to Cover a Family

Kids’ vision can change quickly, making regular exams important; it’s possible that every exam ends with a new prescription. Without vision coverage, replacing glasses regularly can be costly and with a family, those costs can multiply. A vision insurance plan can be a great way to make eye care costs more predictable. Expect to pay less per person for family plan coverage compared to the cost of individual coverage.

Children who struggle with vision may also struggle with routine school tasks or in athletics. Most plans cover comprehensive eye exams, sometimes with no copayment requirement, so you’ll always know if your child needs a new prescription.

You Have Medicare

Certain types of eye exams are covered by Medicare but these are limited to specific eye conditions, such as glaucoma. Medicare does not cover routine eye exams. Similarly, glasses or contacts are not covered by Medicare except when needed following certain covered medical procedures, like cataract surgery.

Many seniors purchase Medigap insurance to provide additional coverage, but Medigap plans, like Medicare, also don’t cover routine vision care. A vision insurance plan can fill the coverage gap and help make costs more predictable for seniors.

Some Medicare Advantage Plans (Part C) may provide coverage for vision or hearing care or may include dental insurance. If you have a Medicare Advantage Part C plan be sure to check your benefits to make sure it covers all of your vision care needs. However, Medicare Part A and B do not cover the cost of routine eye exams or prescription glasses or contacts.

You Don’t Have Much Money Saved

The total cost of an eye exam and glasses or contacts can be several hundred dollars. For many households, that’s a lot of money to part with all at once and the sudden large expense can make it difficult to cover other bills.

Many vision insurance plans offer a discount for paying the annual premium in one payment. For as little as 5% more, you can split your premium into 12 monthly payments, which can help make vision care expenses much more predictable. Because many plans require copayments or may have a capped allowance for frames, it's also wise to put some extra money aside each month to help cover out-of-pocket expenses when it's time for your exam and a new prescription.

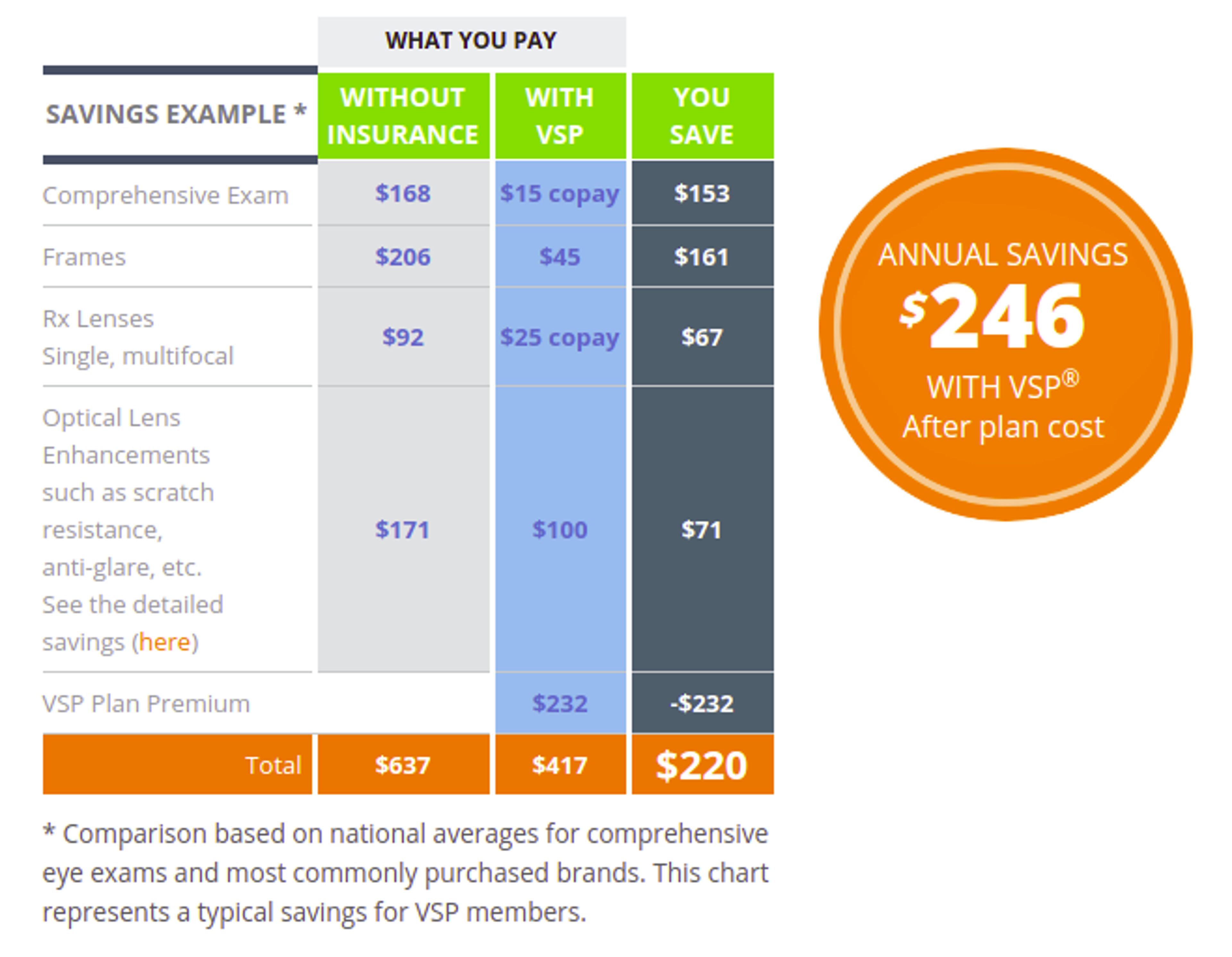

VSP, a nationwide leader in employer-sponsored and individual vision insurance plans, estimates an annual cost of more than $600 if you need glasses. Typically, you can expect the cost of the exam and the cost of lenses and frames or contacts to occur within the span of 30 days.

A vision insurance plan becomes a type of forced savings, where you pay a low monthly premium, keeping the money you’ve budgeted for eye care focused on providing eye care for you and your family. VSP Individual Vision Plans also estimates annual savings of more than $200 when compared to paying for eye care services without coverage.

Concerns about Overall Health

A vision screening isn't a full health exam for your eyes, but a routine vision exam can often detect signs of other health conditions, such as diabetes, high blood pressure or high cholesterol. Early detection of potential health concerns can provide you with more options for treatment and more time to consult with your doctor.

For diseases like diabetes, early detection is key and can make a big difference in both longevity and quality of life. Combined with cost savings, the possibility of early detection for other medical conditions can make vision insurance even more valuable.

When it May Not Be Worth It

In some cases, a vision insurance plan just doesn’t provide enough value to merit a 12-month commitment.

You Don’t Need Glasses

For many individuals and households, the best value in vision insurance plans is found in plans that cover both exams and eyeglasses or contacts. However, if you don't need glasses yet, a vision insurance plan isn't likely to save you any money.

Even inexpensive entry-level plans that only cover the cost of the exam can cost as much annually as the annual exam itself. If you don't need glasses, you might be better off waiting until your vision changes before purchasing vision insurance coverage.

The Plan is Only a Discount Plan

Learn the details of each plan you’re considering because some plans are simply discount plans and don't pay toward any vision-related expenses. You may be able to find similar or even better discounts without paying for a discount plan.

Coverage Only Covers Exams or Glasses (But Not Both)

Several of the vision insurance plans we looked at only covered the cost of exams or the cost of glasses but didn't cover both items. By extension, lens options also may not be covered by these entry-level plans.

As the coverage benefits are reduced with budget-minded vision insurance plans, it becomes more difficult to make a math case that illustrates significant savings. If the plan you're considering covers only the cost of the exam or only the cost of your glasses or contacts, question whether you want to make a 12-month commitment in exchange for limited benefits.

You Have an HSA or an FSA

A health savings account (HSA) or a flexible spending account (FSA) can both be used to cover the cost of eye exams or prescription glasses. Both types of accounts allow you to put away pre-tax money in a special account.

These funds can be used for approved expenses, which include eye exams and glasses. Because both types of accounts use pre-tax money, you make purchases with these funds and immediately save the amount of money you would have lost to taxes.

Depending on your tax bracket, the bottom-line savings can be significant and may remove the need for a vision insurance plan. In effect, with an HSA or FSA, you’re self-insuring for part of your overall healthcare needs.

FSAs are available through employers that offer this benefit. HSAs are coupled with high-deductible health insurance plans and provide higher tax-free savings limits. Funds in an HSA can be used to pay for essential vision care coverage, like glasses or contact lenses, but can also be used to pay for elective procedures, like LASIK.

Try Warby Parker

Warby Parker is a unique online eyeglasses and sunglasses one-stop-shop. While this is not an insurance provider, the platform makes it easy and affordable for consumers to purchase prescription glasses that are also stylish and durable.

When you use Warby Parker, you can have several pairs sent to your home for at-home try-on. Don’t want to wait for the glasses to arrive, you can use the virtual try-on feature to see what they would look like on your phone. You keep the frames you want and send back the rest. You can enter your prescription information on the website, and Warby Parker processes your order, sends you your new glasses, and provides a hard-shelled case along with a cleaning wipe.

Warby Parker is also a great place to go if you need to replace your glasses and you want to spend as little money as possible.

Contact lenses are also available for affordable prices, and you can order any time from the mobile app. Additionally, Warby Parker does maintain a few retail stores that allow you to visit in person, work with the retail staff, and get your glasses the old-fashioned way.

Decide Whether Vision Insurance is Right for You

You may not be fully aware of the benefits and potential cost savings of vision insurance. The ability to spread out your vision care costs into manageable monthly premiums, coupled with overall cost savings that can add up to several hundred dollars per year makes vision insurance worth a closer look. Learn more about choosing the best vision insurance.

Also, evaluate the limitations of the plans you’re considering. Plans that provide an allowance for frames may limit the frame to coverage to 1 pair of frames every 24 months while others offer an allowance for frames once every 12 months. Two years can be a long time to wait for new frames.

Consider copayment requirements as well. While copayments tend to be small, they can add up quickly if you choose lens options with your glasses. If you purchase vision insurance, you'll still have out-of-pocket expenses, but by planning ahead, a vision plan can help make vision care costs both affordable and predictable.

Want to learn more about insurance? Check out Benzinga's guides to the best vision insurance companies, the best cheap car insurance and the best homeowners insurance.

Frequently Asked Questions

How do I know I got the right vision insurance?

Review what is covered and what is not when you choose vision insurance. Make certain you choose a vision policy that offers the services you need.

What’s typically included with a vision insurance policy?

A vision insurance policy typically includes coverage for exams, frame reimbursement and lens reimbursement. Vision insurance might also include discounts from certain retailers or doctor’s offices.

What types of vision plans are available to me?

Vision plans generally include a discount plan where you pay out of pocket and a benefits plan where you make copayments and the provider files your claims.