On Thursday, Warren Buffett's Berkshire Hathaway BRK filed a 13F disclosing a 40 million share stake in Exxon Mobil XOM. Footnoted tweeted that confidential filings indicate Berkshire had acquired the shares earlier. Nevertheless, StockTwits noted XOM was now Berkshire's 7th largest position, behind only Wells Fargo WFC, Coca-Cola KO, IBM IBM, American Express AXP, Procter & Gamble PG, and Walmart WMT. With John Hussman and others warning of a possible stock market crash early next year, Exxon longs may be interested in adding some downside protection. The good news is that that's pretty cheap to do right now. We'll look at a way to do so below.

1) Hedging With Optimal Puts

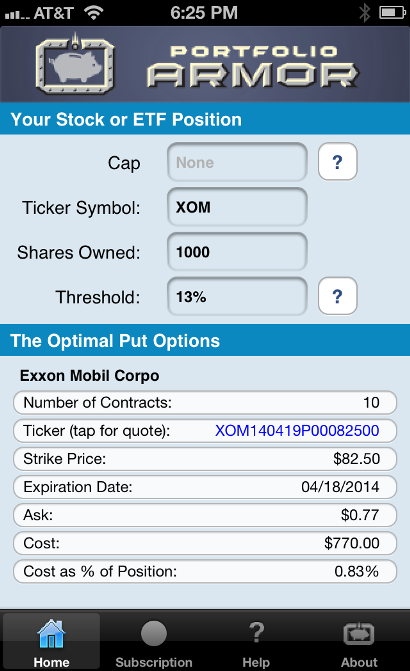

Uncapped upside, 0.83% cost.

Usually when hedging equities I use 20% decline thresholds, but since XOM is inexpensive to hedge now, I've used a smaller decline threshold here. These were the optimal puts, as of Thursday's close, to hedge 1000 shares of XOM against a greater-than-13% drop between now and April 18th:

As you can see at the bottom of the screen capture above, the cost of hedging, as a percentage of position value, was 0.83%. Note that, to be conservative, Portfolio Armor calculated the cost of this hedge using the ask price of the optimal puts; in practice, an investor can often by puts for a less (some price between the bid and ask), so the actual cost of this protection may have been slightly lower.

Possibly More Protection Than Promised

In some cases, hedges such as the ones above can provide more protection than promised. For a recent example of that, see this post about hedging shares of Tesla Motors, Inc. TSLA.

*Optimal puts are the ones that will give you the level of protection you want at the lowest possible cost. Portfolio Armor uses an algorithm developed by a finance PhD to sort through and analyze all of the available puts for your stocks and ETFs, scanning for the optimal ones.

**Optimal collars are the ones that will give you the level of protection you want at the lowest net cost, while not limiting your potential upside by more than you specify. The algorithm to scan for optimal collars was developed in conjunction with a post-doctoral fellow in the financial engineering department at Princeton University. The screen captures above come from the Portfolio Armor iOS app.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date of Trade | ticker | Put/Call | Strike Price | DTE | Sentiment |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.