Well, hedge fund manager Tim Knight was right. Boehner blinked, the government's back open, and the S&P 500 hit a record high Thursday, rallying on news of the latest increase in the US government's credit card limit.

When there was still some uncertainty about how the standoff in DC would resolve itself, volatility began to rise a bit. From Tuesday, October 1st, to Wednesday, October, 9th, the iPath S&P 500 Short Term VIX Futures ETN VXX climbed more than 15%. At that point, I posted a hedge for VXX longs looking to add some downside protection ("Getting Paid To Limit Your Downside On VXX"). In this post, I'll show how that hedge reacted to VXX's post-deal drop.

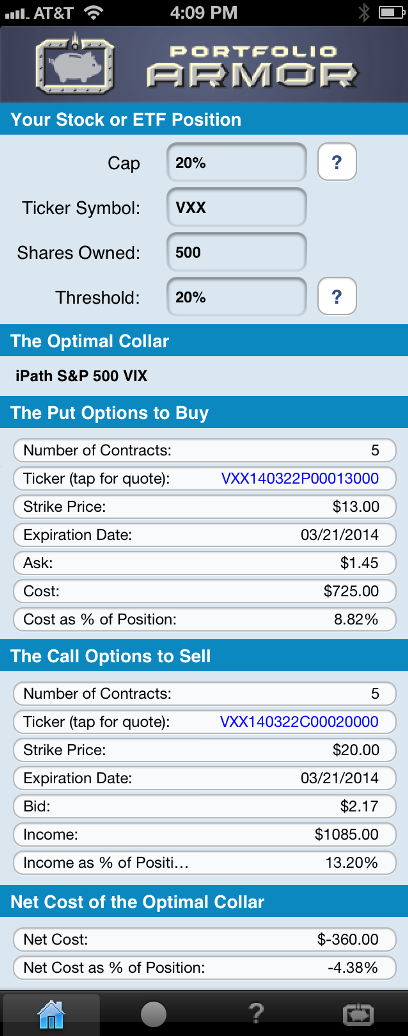

The October 9th VXX Hedge

This was the optimal collar*, as of October 9th's close, designed to limit an investor's losses to 20% over the next several months, for an investor willing to cap his upside at 20% over the same time frame:

As you can see at the bottom of the screen capture above, the net cost of that optimal collar was negative, meaning the investor would have gotten paid $360 to hedge.

How That Hedge Has Reacted To VXX's Drop

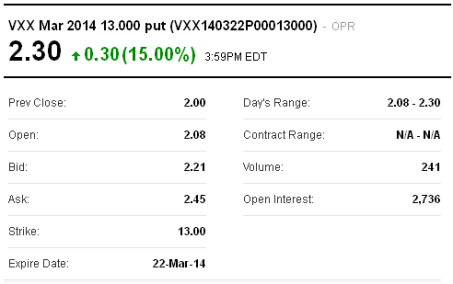

Here is an updated quote on the put leg as of Thursday's close:

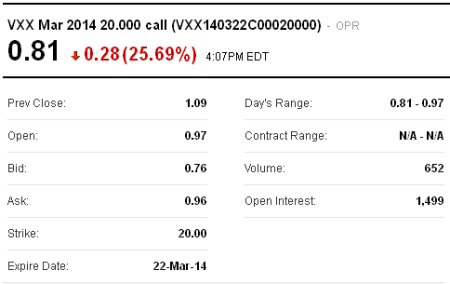

And here is an updated quote on the call leg:

How That Hedge Protected Against Wednesday's Drop

VXX closed at $16.37 on Wednesday, October 9th. A shareholder who owned 500 shares of it and opened the collar above on October 8th had $8,185 in VXX shares plus an outlay of -$360 on the hedge, so $7,825 taking into account the hedge.

VXX closed at $13.01, on Thursday, October 17th, down 20.5% from its price on October 9th. The investor's shares were worth $6,505 as of Thursday's close, his put options were worth $1,150, and if he wanted to close out the short call leg of his collar, it would cost him $405. So: ($6,505 + $1,150) - $405 = $7,250. $7,250 represents a 7.3% drop from $7,825.

More Protection Than Promised

So, although VXX had dropped by 20.5% at the time of the calculations above, and the investor's hedge was designed to limit him to a loss of no more than 20%, he was actually down only 7.3% on his combined hedge + underlying position by this point.

Options Give You Options

Being hedged gives an investor breathing room to decide what his best course of action is. A VXX long hedged with this collar could exit his position with an 7.3% loss now, he could wait to see what happens, or if he remains bullish on VXX (despite its egregious long term chart), he could buy-to-close the call leg of this collar, to eliminate his upside cap. If he's even more bullish, he could sell his appreciated puts, and use those proceeds to buy more VXX. He has those options because he's hedged.

*Optimal collars are the ones that will give you the level of protection you want at the lowest net cost, while not limiting your potential upside by more than you specify. Portfolio Armor's algorithm to scan for optimal collars was developed in conjunction with a post-doctoral fellow in the financial engineering department at Princeton University. The screen captures above come from the Portfolio Armor iOS app.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.