The last several months have been a rollercoaster ride for shareholders of E-Commerce China Dangdang, Inc. (NYSE: DANG). The stock traded at under $4 per share in early June, and spiked to $11.71 in mid-August, before pulling back to under $8 per share by the end of the month. It was on the upswing again on Friday afternoon, trading at $10.84 per share. For investors looking to add downside protection now, here’s a way to get paid to do so.

Hedging With An Optimal Collar

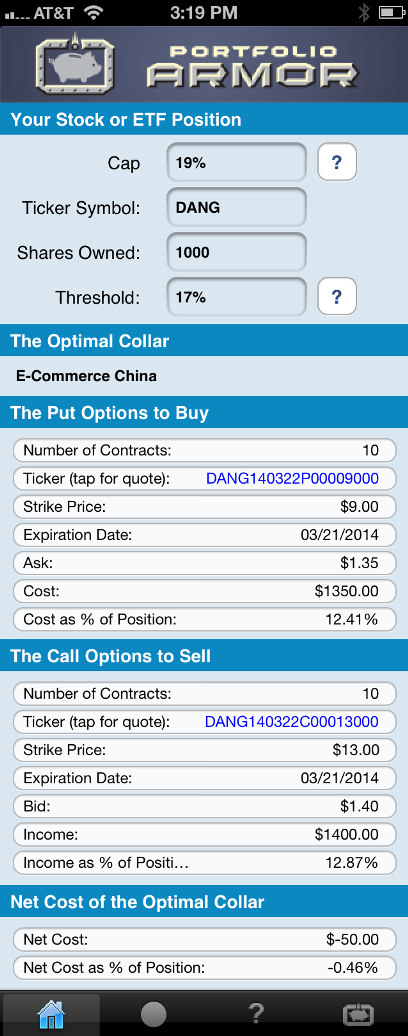

Below is the optimal collar*, as of Friday afternoon, to hedge 1000 shares of DANG against a >17% drop between today and March 21st, for an investor willing to cap his potential upside at 19% over the same time frame. Before we look at it, let me anticipate a question:

Why Would I Want To Cap My Upside At 19% For 6 Months?

Well, you might not. In which case, you could pay a lot to hedge, or just take your chances and hope the stock doesn’t sink back below $4 over then next six months. On the other hand, you might be willing to cap your upside here in return for getting paid to add downside protection, considering that you’re up about 250% if you’ve held this stock through the summer. In that case, here’s that optimal collar:

As you can see at the bottom of the screen capture below, the net cost of this optimal collar was negative, meaning you would have gotten paid to hedge in this case.

Note that, to be conservative, Portfolio Armor calculated the cost of this hedge by using the bid price of the call leg and the ask price of the put leg. In practice, you can often sell calls for more (at some price between the bid and ask) and buy puts for less (again, at some price between the bid and ask), so, in actuality, an investor opening the optimal collar above would likely have netted more than $50 to do so.

Possibly More Protection Than Promised

In some cases, hedges such as the ones above can provide more protection than promised. For a recent example of that, see this post about hedging shares of BlackBerry (BBRY).

*Optimal collars are the ones that will give you the level of protection you want at the lowest net cost, while not limiting your potential upside by more than you specify. Portfolio Armor’s algorithm to scan for optimal collars was developed in conjunction with a post-doctoral fellow in the financial engineering department at Princeton University. The screen captures above come from the Portfolio Armor iOS app.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.