Locking In First Solar Gains

With shares of First Solar, Inc. FSLR up more than 45% on Tuesday, in this post we’ll show a way investors can get paid to lock in their gains with an optimal hedge.

Two Ways To Hedge; One Works Here

Hedging With Optimal Puts

In a recent article, we looked at two ways to hedge Apollo Group, Inc. APOL against a greater-than-20% decline over the next several months. The first way, using optimal puts*, allowed uncapped upside, but was more expensive; the second way, using an optimal collar**, capped an investor’s potential upside, but was less expensive. As of Tuesday’s close, though, it was quite expensive to hedge First Solar against a greater-than-20% drop over the next several months using optimal puts — the cost of that put protection would have been greater than 13% of position value.

Hedging With An Optimal Collar

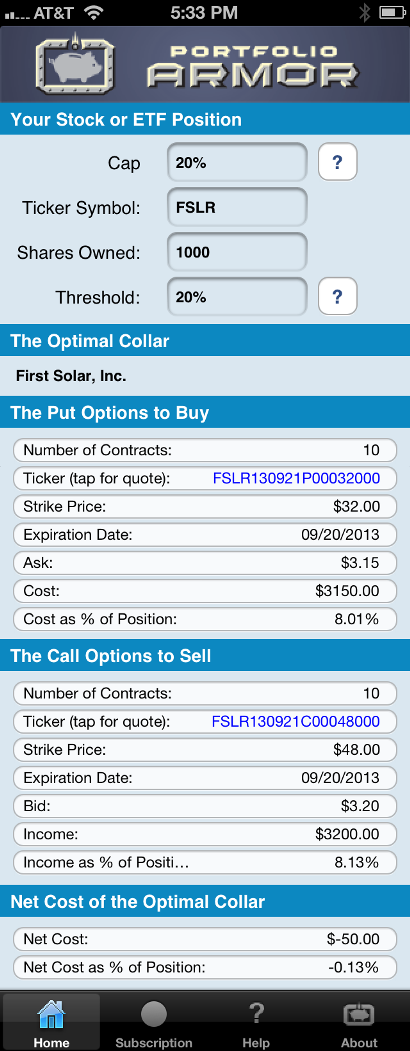

It wasn’t, however, too expensive to hedge First Solar against a >20% drop over the next several months using an optimal collar, if you were willing to cap your potential upside by the same percentage over the same time frame. The screen capture below shows the optimal collar, as of Tuesday’s close, to hedge 1000 shares of FSLR against a greater-than-20% drop by September 20th, with an upside cap of 20%.

As you can see at the bottom of the screen capture above, the net cost of this optimal collar was negative, meaning a First Solar investor would have gotten paid to hedge in this case.

Calculating Net Cost Conservatively

Bear in mind, that to be conservative, Portfolio Armor uses the ask price of the puts to calculate the cost of buying them, and the bid price of the calls to calculate the income generated by selling them. In practice, an investor can often buy a put for a slightly lower price (i.e., some price between the bid and the ask), and sell a call for a slightly higher price (again, some price between the bid and the ask). Because of this, an investor opening this collar on Tuesday would likely have been paid more than $50 to do so.

*Optimal puts are the ones that will give you the level of protection you want at the lowest possible cost. Portfolio Armor uses an algorithm developed by a finance Ph.D to sort through and analyze all of the available puts for your stocks and ETFs, scanning for the optimal ones.

**Optimal collars are the ones that will give you the level of protection you want at the lowest net cost, while not limiting your potential upside by more than you specify. The algorithm to scan for optimal collars was developed in conjunction with a post-doctoral fellow in the financial engineering department at Princeton University. The screen captures above come from the Portfolio Armor iOS app.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.