A previous article examined the relationship between the S&P 500 and the cyclically-adjusted price/earnings ratio (CAPE) for the S&P 500. The ratio today is at a stratospheric level that has only been reached twice since 1871, first in September 1929 before the Great Depression, and again in December 1999, before the tech bubble burst.

In the previous article, we stated that the CAPE provides useful information when it is extremely high or low. We concluded that article by noting that, given current CAPE levels, perhaps now is a good time to think about reducing exposure to US equities. In this article, I want to explore other factors that support this decision.

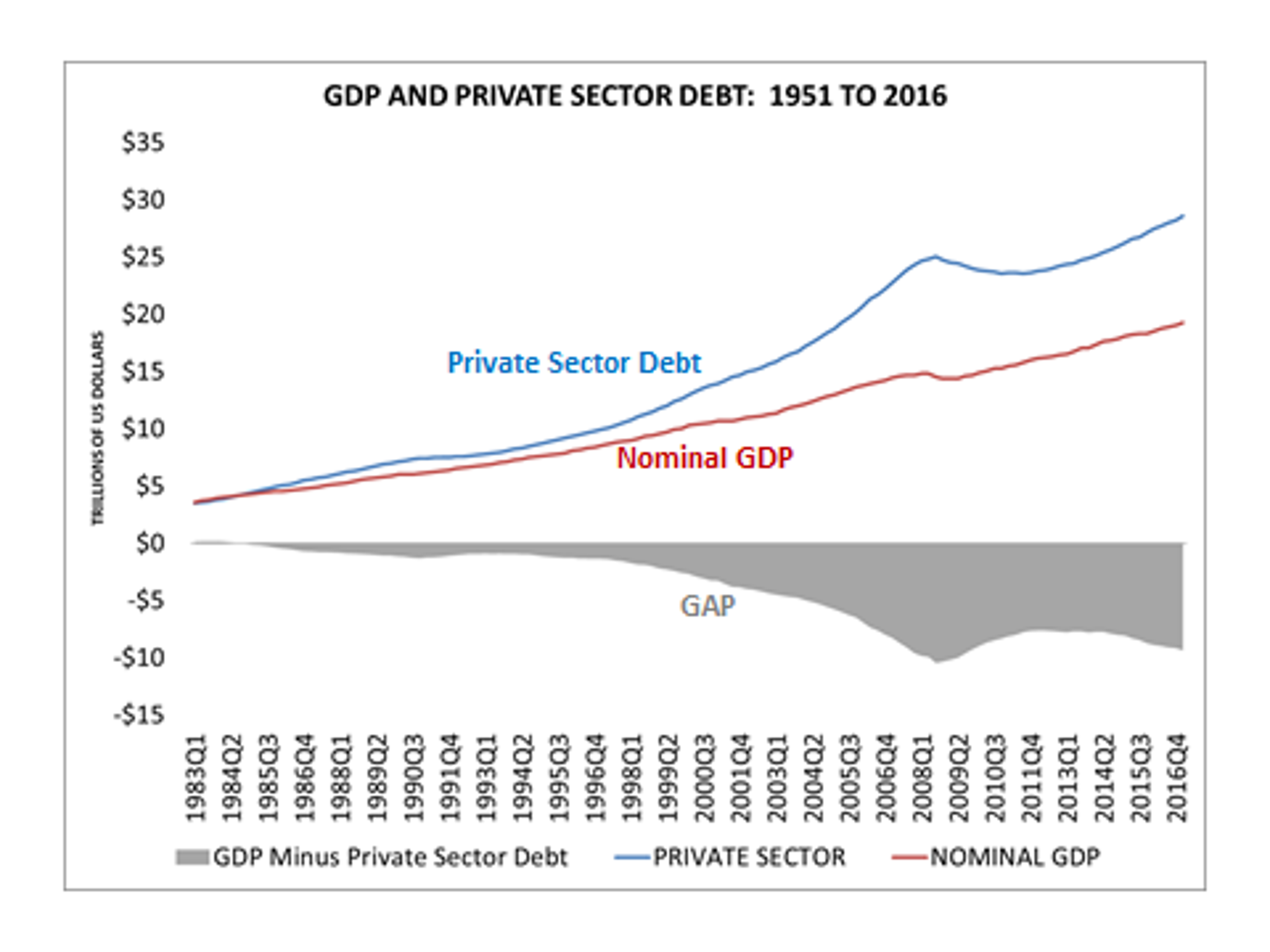

The deregulation and liberalization of the financial markets during the 1980's fueled the explosive growth in credit and asset prices (see chart below). Positive feedbacks between credit creation and asset prices generated a series of boom-bust cycles that resulted in a number of crises, including the stock market crash of 1987 (thirty years ago today!), the thrift crisis, Russia/LTCM and the tech bubble. The continuation of this pattern in part reflected the Fed’s decision to conduct an asymmetric monetary policy, leaving markets alone as prices appreciated, only to intervene when they threatened to collapse (“Greenspan Put”).

These financial cycles persisted until eventually, they ended in tears during the global financial crisis of 2007-2008. When the financial system threatened to collapse in 2007-2008, the Fed chose to bail out various financial institutions and markets, effectively becoming the market-maker of last resort. It then implemented Quantitative Easing (QE) policies in late-2008. These policies (see chart from Ed Yardeni below) fueled a renewed surge in US equity prices that coincided with QE1, QE2 and QE3.

Quantitative Easing policies boosted asset prices and lowered the cost of borrowing, but ultimately had very little impact on real economic growth (aka, Main Street). When the economy is depressed (in a balance sheet recession), lower interest rates do not spur borrowing to finance real economic activity (capital formation and production of goods and services), given the generalized reluctance to borrow or lend. Lower interest rates instead stimulated asset prices (e.g., US equities, bonds, etc.). These policies benefited households that owned financial assets, primarily the top 20% of the income distribution, which as of 1983 (according to the Fed’s Survey of Consumer Finances) owned 81% of all wealth. By 2013, their share of ownership had increased to 89%.

What was badly needed (as pointed out by Amir Mian and Atif Sufi in their book, House of Debt) was a substantial fiscal expansion that targeted reductions in the debt ratios of the bottom 80% of households in the economy. Reportedly, 60% of the wealth held by the bottom 80% was in its principal residence, and housing prices declined by 30%, leaving many homeowners indebted without little in the way of an offsetting asset. Given that this segment of the population has a much higher marginal propensity to consume than the top 20%, reducing their debt levels would have more effectively stimulated aggregate demand and real economic growth. However, such a plan was not deemed politically acceptable at the time.

The biggest challenge the US economy faces today is the legacy of financialization, namely the continued excessive debt burden carried by the bottom 80% of households. Historically, this segment of the population consumes most of what it earns. However, encumbered today by high levels of debt, this segment is unable to fulfill its historic role. QE policies did nothing to address or mitigate the burgeoning debt stock within the bottom 80%, other than possibly providing a temporary respite, via lower debt service costs. These households remain unable to drive aggregate demand, which explains why real economic growth remains so weak.

US Equity Valuations: Downward Pressure

There is an old saying: “If I were you, I would not start from here”. I am exceedingly cautious about exposure to the US equity market, given the factors described above, and recently have been reducing exposure, while taking profits.

I am intrigued by comments from people that “this time is different,” that there is "no recession in sight" and that "interest rates will not rise too quickly," not because they are necessarily incorrect, but because current prices for US equities make them V-U-L-N-E-R-A-B-L-E to many things we may not be able to anticipate. Yes, market declines often accompany recessions, and yes, the Fed is not likely to be too aggressive in raising interest rates. This time is always different, but never entirely so. With equity valuations where they are today, prices can reverse simply because investors become risk averse, or for any number of reasons. Are we really willing to risk 30% of our capital for a 10% gain? Are we really that good at playing the game of "chicken" with the financial markets? With US equities priced where they are today, I believe they are definitely VULNERABLE to a reversal. So I for one do not take much comfort in reading these types of analyses. It is the tails that keep me awake at night!

The Fed is in uncharted waters having to unwind QE policies; this introduces another unknown unknown that only heightens uncertainty Given its record in addressing financial crises in the past, there appears little reason to expect the Fed to get this right. Bernanke may have done right by intervening aggressively after the crisis hit, but apparently no one at the Fed saw the crisis coming, in part given the use of macroeconomic models that intentionally ignore credit and money. And Bernanke himself, in 2004, refused to recognize the possibility of a nationwide housing bubble. The Queen of England’s question resonates: “why did no one see it coming?” Fortunately, some did (Steve Keen, Wynne Godley and Dean Baker, to name three), though they were well outside mainstream macroeconomics.

So once again I pose the following question: Does it make sense to risk a potential loss of 30% to generate an additional 10% in return? Are we really that good at playing the game of “chicken” with the financial markets? Investing is not a game that can be won – in fact, it can only be lost, in terms of failing to meet our long-term investment objectives.

Liberalization of the financial markets during the 1980s was accompanied by a fundamental change in the nature of economic activity. In the earlier economic Golden Age of capitalism, wages were closely linked to productivity growth and the financial system more or less shared in the successes of its business clients, with relatively long horizons. However, as liberalization ensued, resort to speculative activities accelerated -- new ways of making money. These activities have little real economic foundation, and largely depend on capital gains (a zero-sum game). The post-crisis phase of this juxtaposition between the financial sector and the real economy is nicely illustrated in the chart below. Asset prices have ballooned while real economic growth has lagged.

Asset Allocation Implications

I have increased my allocation to non-US equities, with a tilt toward emerging markets, based on several reasons. First, the financial cycles in many of these economies have lagged that of the US. And second, QE policies are continuing in Europe and Japan (where signs of growth finally appear to be improving!). Other asset classes, including high-yield bonds, emerging market debt, corporate bonds and commodities, do not appear attractively priced. Given current valuations across-the-board, we prefer to be patient and wait for a more attractive entry point.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.