As interest rates continue to rise off historically low levels, a key concern for income investors is how to generate income while also minimizing principal losses on their investments. A common approach is to pare back on fixed-rate securities, which tend to have more interest rate sensitivity, known as duration. Instead, investors today are favoring floating or variable rate issues. These securities offer both lower duration risk and the potential for higher dividends and coupons as rates rise.

In this piece, we explore variable rate preferreds in particular as an income solution based on their resilient characteristics in a rising rate environment. We also compare the performance of variable rate preferreds to other fixed income asset classes historically in rising rate environments. In addition, we highlight how variable rate preferreds can be used in the context of investors’ portfolios.

Key Takeaways

- Variable rate preferreds tend to offer an attractive mix of higher yield potential and lower duration than other income-oriented asset classes.

- In analyzing historical performance during rising rate environments, we found that variable rate preferreds typically outperformed broad fixed income.

- We continue to remain positive on the outlook for variable rate preferreds given that yields are now above long-term averages, issuance has been very low in 2022 thus far, and correlations to other fixed income asset classes could make these securities an attractive portfolio diversifier.

What Are Variable Rate Preferreds?

Variable rate preferred stocks, specifically fixed-to-floating rate preferreds, are equity securities that pay a fixed dividend amount for a specified period, typically 5 or 10 years. Thereafter, they switch to a floating rate dividend on a predetermined schedule, hence the name fixed-to-floating. Typically, the duration for variable rate preferreds is close to the number of years remaining until they convert to floating rate dividends¹.

Given that this adjustable dividend payment is typically based on prevailing interest rates, variable rate preferreds tend to have lower durations than fixed-rate preferreds, mainly because of the fixed rate leg of the preferred’s life. As of May 31, 2022, the duration profile of variable rate preferreds was 1.90 years, and securities in the floating rate period had a duration of 0.08. The securities in the fixed portion of the fixed-to-float cycle had a duration of 2.15.2

In contrast to this, floating rate preferreds pay adjustable dividends for the life of the preferred security or a minimum rate (‘floor’). The dividends adjust on a set schedule, typically every 3 or 6 months. The dividend payment is commonly determined by the 3-month London Interbank Offered Rate (LIBOR) – or an alternative such as a Treasury yield or SOFR (Secured Overnight Financing Rate) – plus a fixed spread, which is primarily a reflection of the issuer’s credit risk.3 As interest rates rise, so too should the dividend payment amount to investors, unless it’s subject to a minimum rate that is above the interest rate plus spread. Conversely, if rates fall, the dividend should decrease.

LIBOR is in the process of being discontinued due to concerns over past manipulations of rate setting. New issues of floating rate securities will be based on alternative reference rates and existing securities will gradually transition from LIBOR to alternative rates, such as SOFR. This transition has been underway for several years and central banks, regulators, and company executives have been working toward a smooth and orderly transition to the new reference rates.

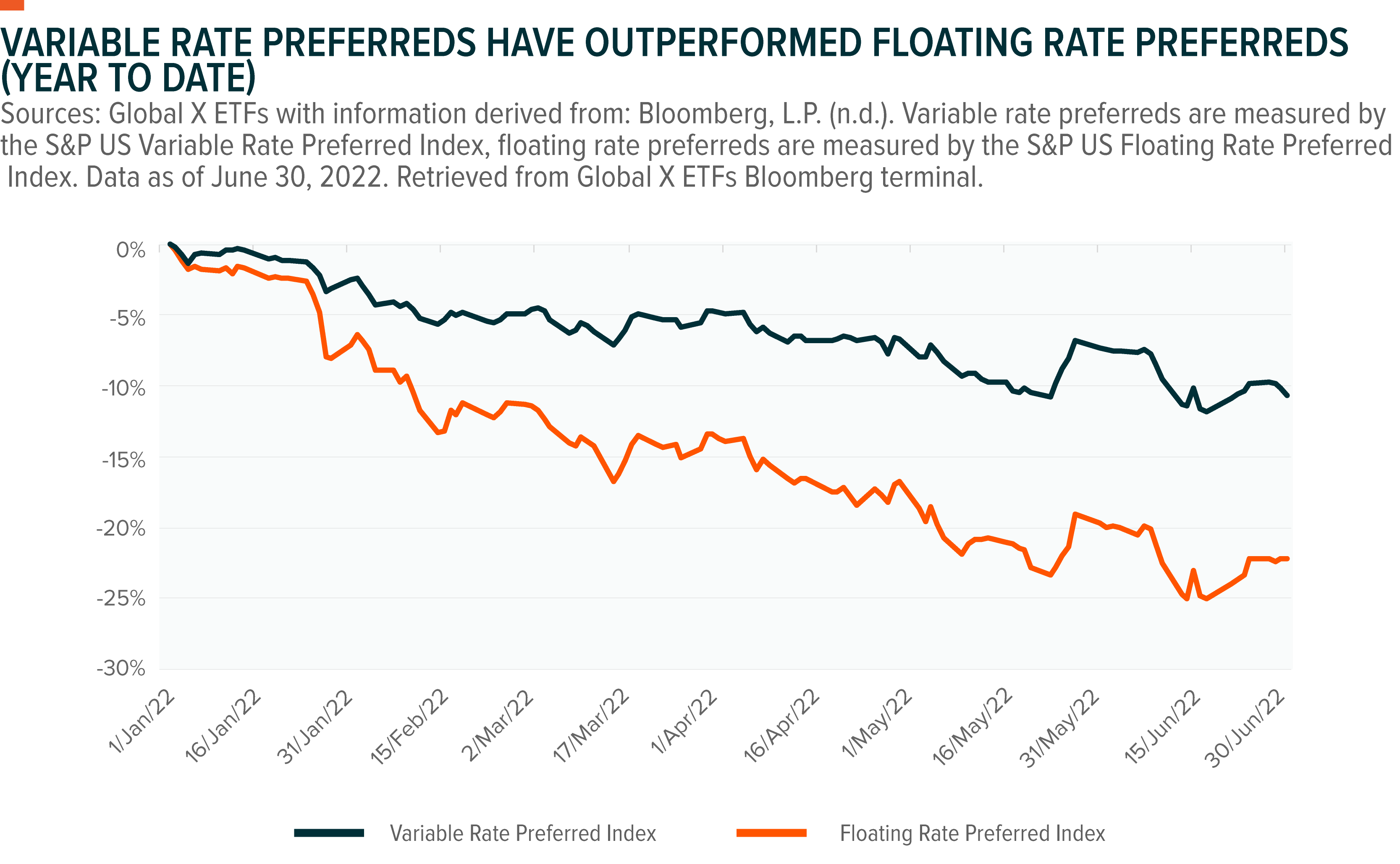

On floating rate preferreds, it is worth noting that currently this pocket of the market is very small, with only 11 securities currently in the S&P US Floating Rate Preferred Index.4 Also, while these securities have negligible duration risk, the tradeoff is the elevated credit risk they carry, due to the potential for rising coupon payments. As we can see below, eschewing duration risk doesn’t necessarily equate to outperformance in a rising rate environment.

Callability Gives Variable Rate Preferred Issuers Optionality

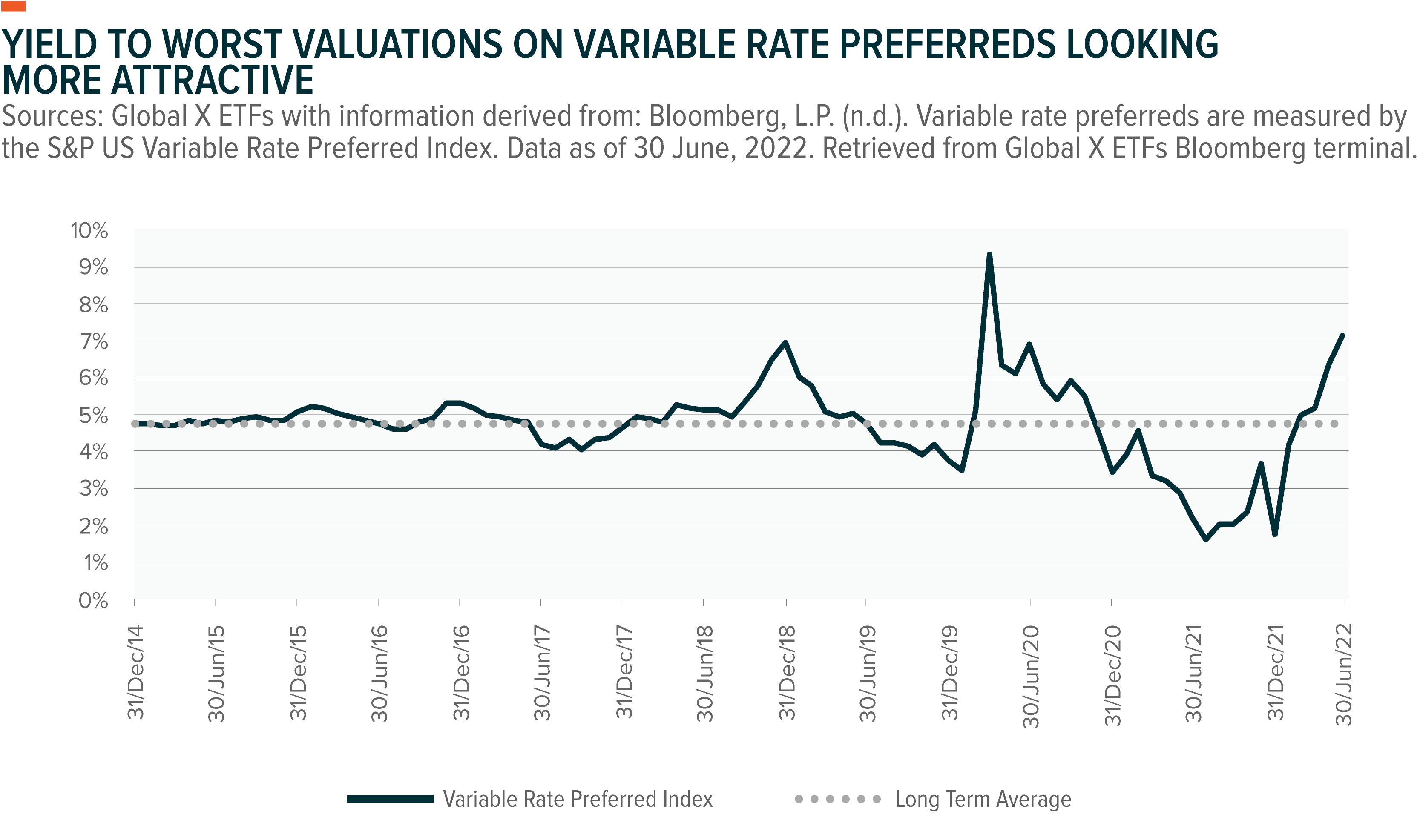

Variable rate preferreds often have features that are not common in other types of securities. For example, variable rate preferreds typically have a call option when they switch from paying fixed rate dividends to floating rate dividends. This option allows the issuer to buy back the preferred at a predetermined price, typically at or just above par value. As a result, the price of these securities reflects the yield offered and the risk of them being called. The yield on these securities is usually higher than securities without this feature, to compensate investors for this embedded call risk. For investors, this means the ‘yield to worst’ metric is important in assessing relative valuations of variable rate preferreds as this incorporates the risk of the security being called.

The below chart shows variable rate preferreds yield to worst over time, and the underperformance in 2022 so far has resulted in yields now being higher than their long-term average of 4.74%.

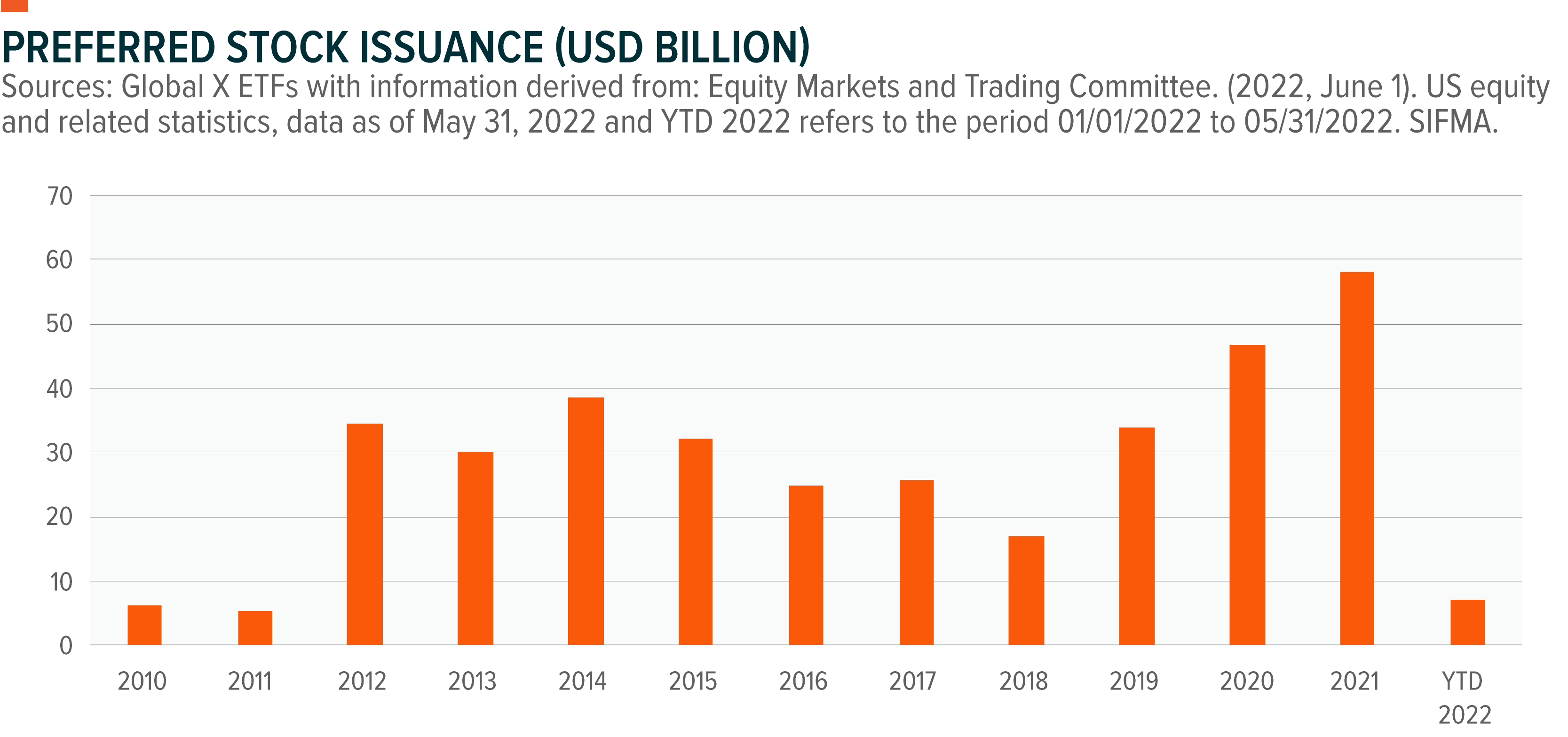

With interest rates rising, this makes re-financing less attractive to companies that use debt or preferred shares for financing, as interest costs are likely to get higher. We view this as one reason that preferreds, which have a call option, are now less likely to be called by issuers. Following the Global Financial Crisis, preferred issuance has tended to have a close relationship with the direction of interest rates. Issuance is greater when rates fall because yields are lower, resulting in a lower cost to issuers.

For example, less issuance occurred in periods of rising rates like 2016–2018 and so far in 2022, while more issuance occurred in periods of falling rates like 2014–2015 and 2019–2020. In 2021, preferred issuance was high despite U.S. interest rates rising. However, we attribute the high issuance to the very low relative level of interest rates and very tight credit spreads resulting in a still-attractive environment for companies to issue capital. In the first five months of 2022, issuance was much lower than the 2019–2021 period. From a simple supply-demand view, less supply should balance preferreds’ prices.

Variable Rate Preferreds Have a Track Record of Mitigating Rising Rates

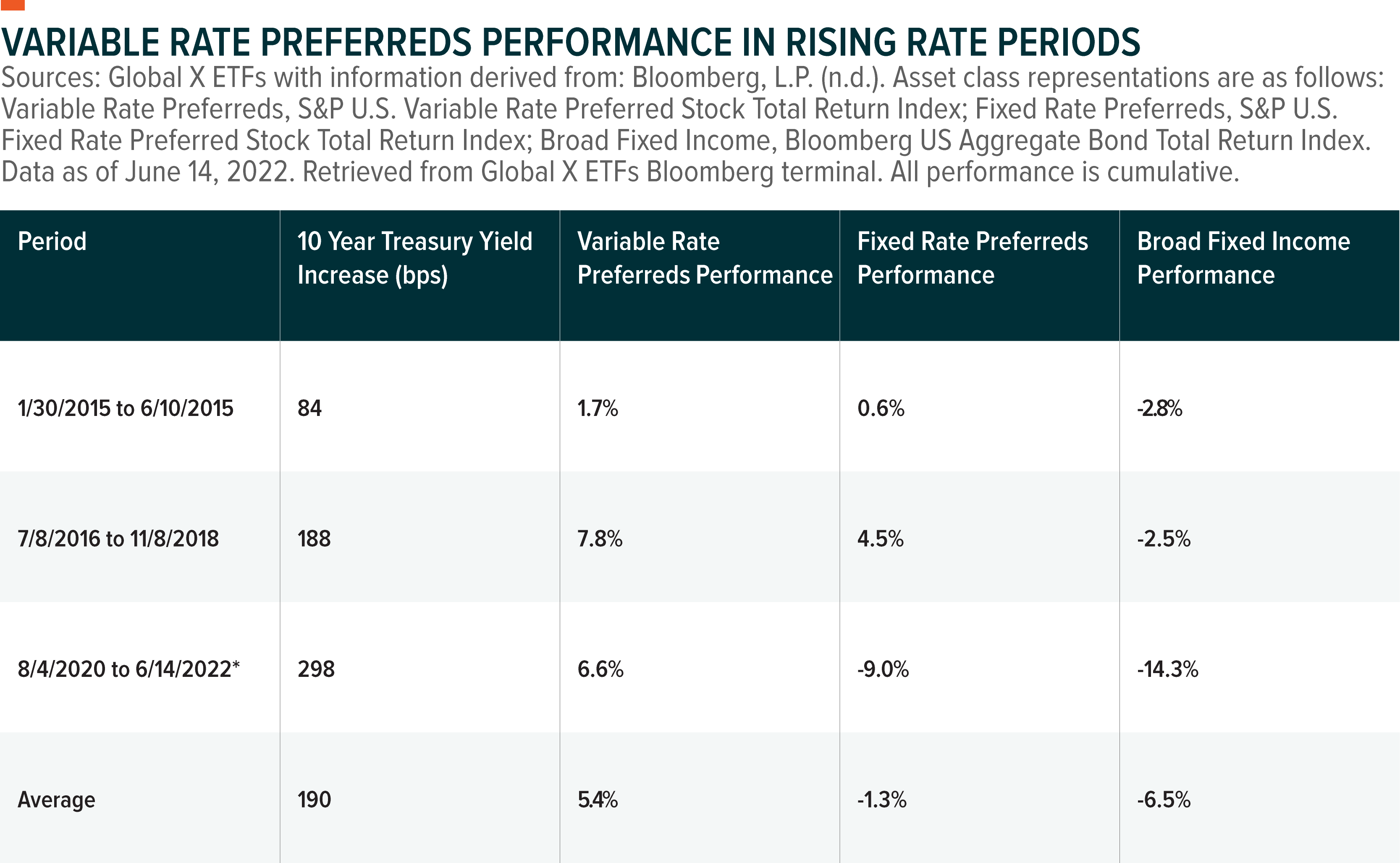

In analyzing past examples of rising rates, measured by 10-year US Treasury moves, we compared the performance returns of variable rate preferreds, fixed rate preferreds, and the broader fixed income market to gauge any trends in performance. Keep in mind, though, that past performance is not a guarantee of future performance trends.

Variable rate preferreds had positive performance returns in all the periods that we analyzed, and on average they outperformed the two other asset classes that we selected.

*Note: this period we have identified is the current period to date.

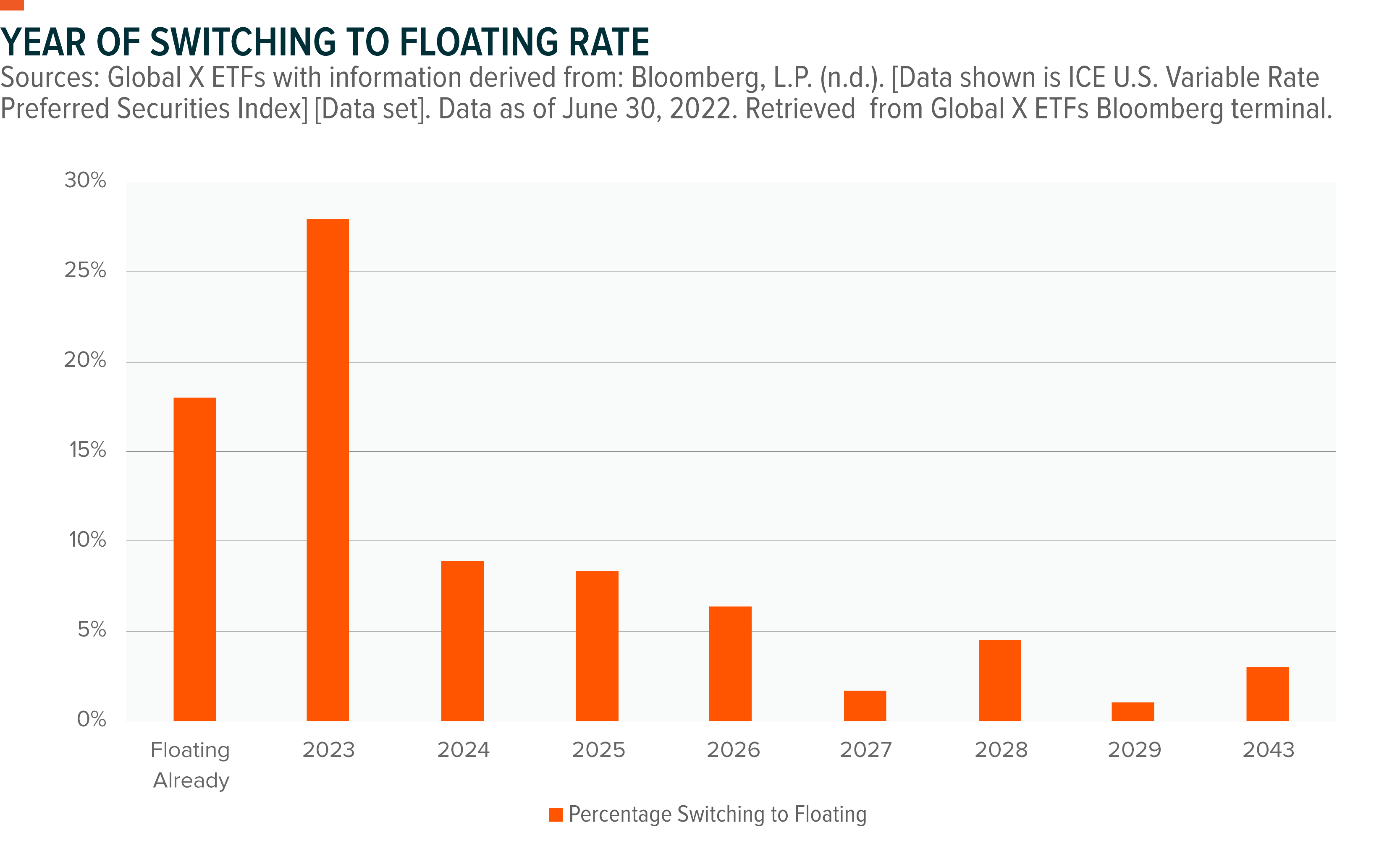

To gauge duration risk, it is also important to understand the time frames for fixed-to-floating preferreds to switch to floating rate securities. Issuance of these securities has not been uniform over time. A large proportion of variable rate preferreds were issued with 5-year and 10-year fixed rates in 2013/2014 and 2018/2019, when interest rates were low. The chart below shows a large proportion of securities switching to floating rate in 2023 and 2024.

Using Variable Rate Preferreds in a Portfolio

Variable rate preferreds have several key attributes that may make them an attractive asset class to include in a portfolio.

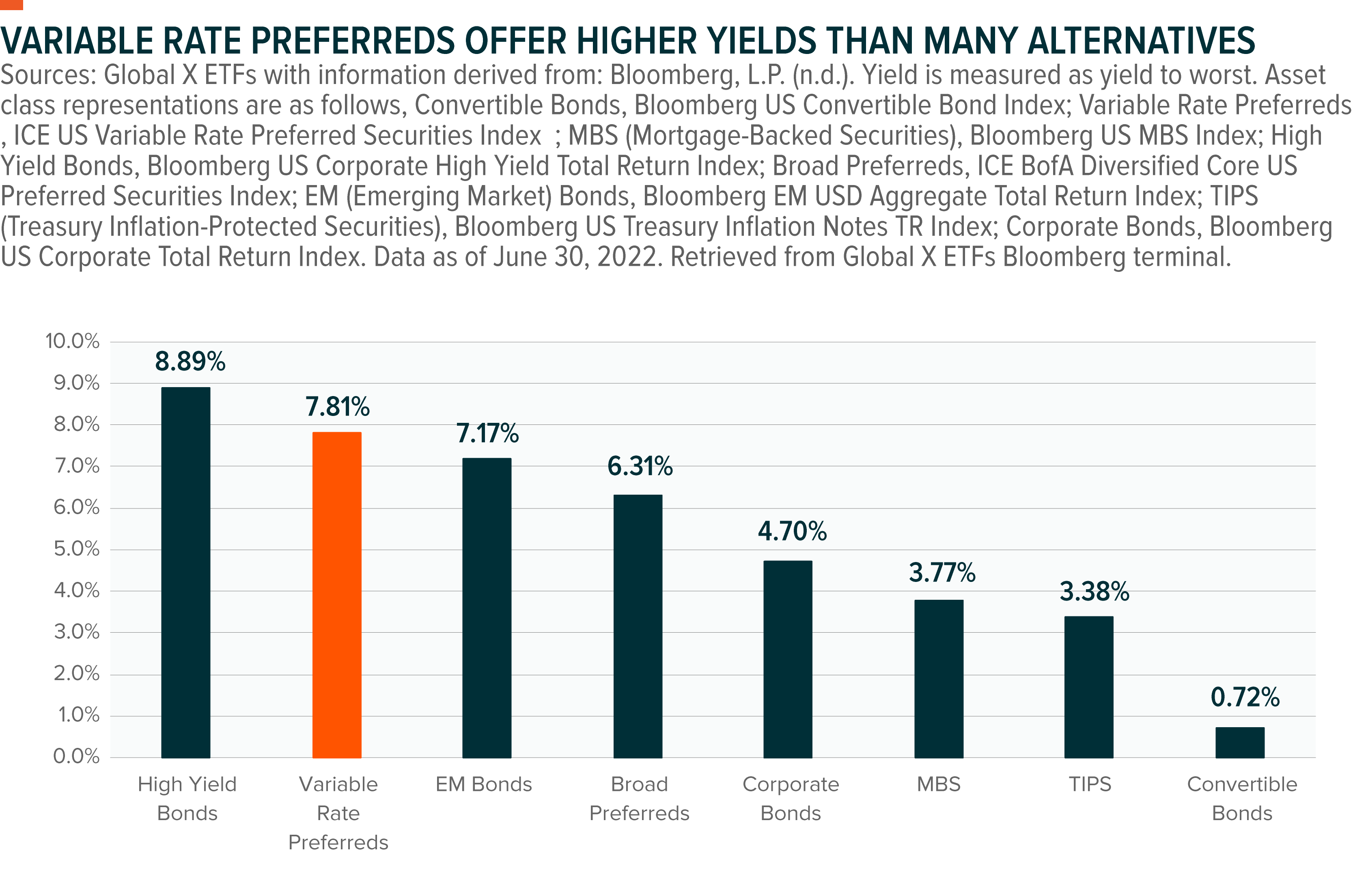

Variable rate preferreds historically offer a high yield compared to other income producing assets, as seen in the chart below.

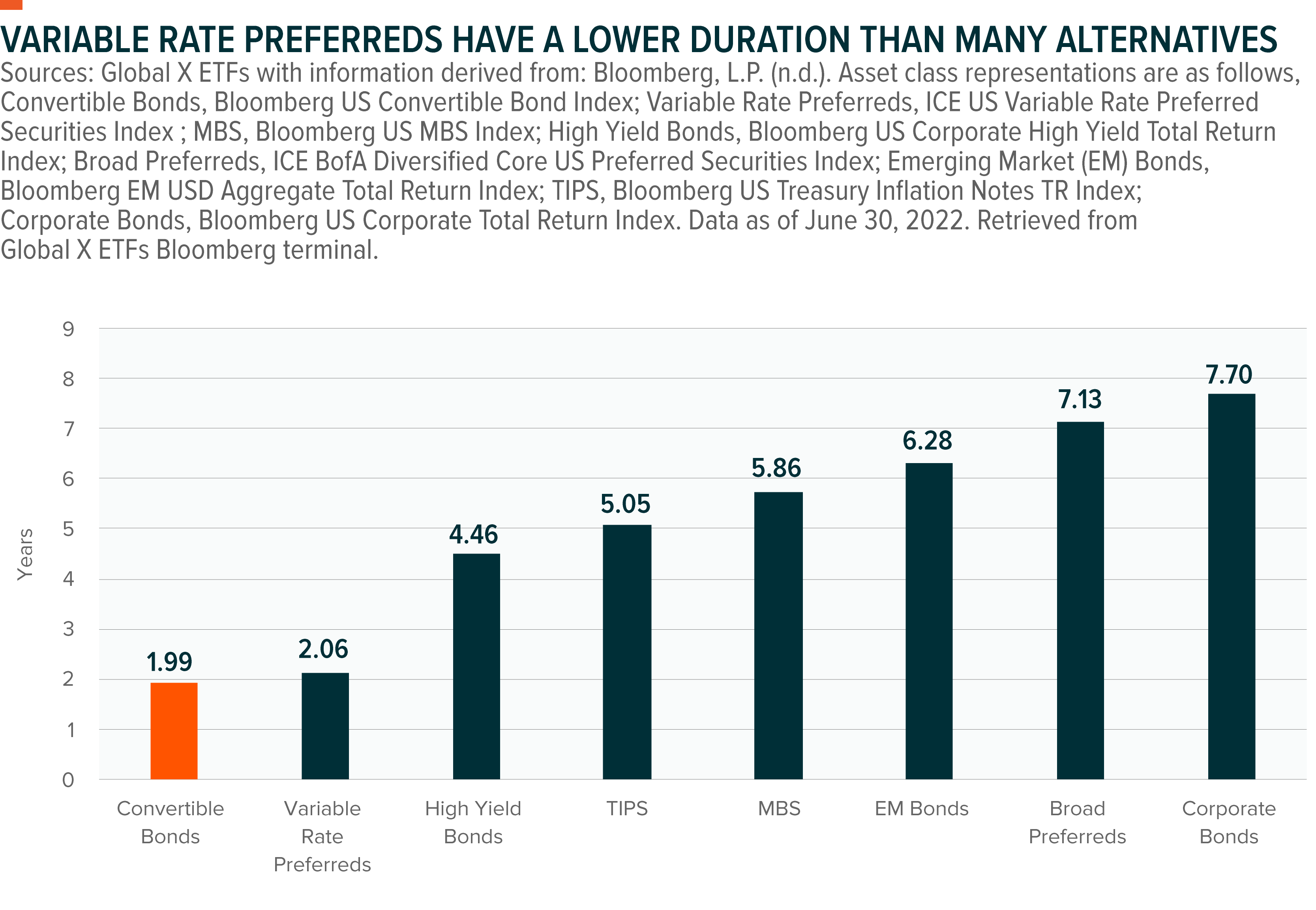

As discussed earlier, variable rate preferreds have performed well in rising rate environments due to their low duration.

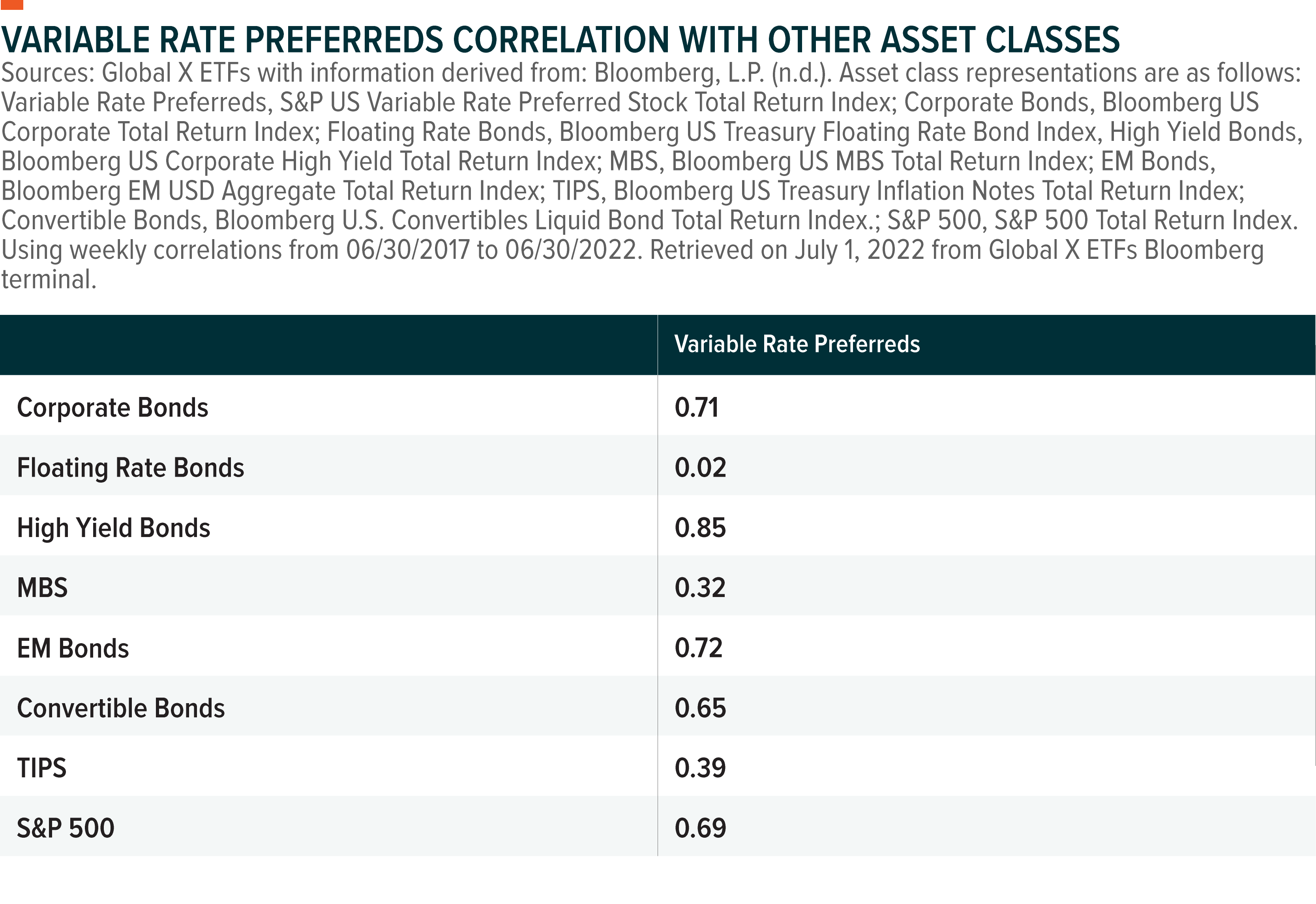

Variable rate preferreds can be used within an existing fixed income allocation due to their relatively low correlation to traditional bonds. For fixed income portfolios consisting of assets like floating rate bonds and TIPS, variable rate preferreds can be added to a portfolio in an effort to both increase portfolio yield and provide diversification benefits due to the low correlations seen in the figures below.

While preferreds are considered lower rated/ higher yielding securities, they do in fact tend to have a higher overall credit rating than US high yield bonds. Variable rate preferreds have an average credit rating of BBB-, compared to high yield bonds average credit rating of BB-.5 Variable rate preferreds could be a substitute for higher yielding fixed income segments with a relatively high correlation, such as high yield bonds, for investors wanting to maintain the higher income potential and reduce duration risk.

Conclusion

The current macroeconomic environment of high and persistent inflation has seen the US Federal Reserve (Fed) and other central banks hike interest rates, and consequently many fixed income investments fall sharply in value in 2022. Interest rate risk has therefore become a large consideration for investors still wanting to achieve a high level of income on their portfolios. We view the interest rate hiking priced in by markets as aggressive and leaves some upside risk to income investors if inflation starts to recede, or if the US Fed believes it needs to slow down on raising rates. We have a positive outlook on variable rate preferreds given the attractive yields they now offer as well as a low duration profile.

Financial services companies like major banks, which are large issuers of preferreds, generally have strong balance sheet positions, and regulators such as the Fed sign off on the overwhelming majority of banks’ capital ratios. In June the 2022 Federal Reserve Stress Test Results were released, showing that the 33 largest banks which were subject to the stress test all had more than sufficient capital levels for the stressed scenario.6 Following the Global Financial Crisis, banks have been improving their capital ratios over time, and there have been few issues with companies in this respect. The average S&P issuer credit rating for US Financials is A, which highlights the financial strength of these companies at the issuer level.7

For investors looking for higher yield potential and the diversification potential that variable rate preferreds can offer relative to traditional fixed income assets, we believe it may be appropriate to consider variable rate preferreds as an income solution.

Related ETFs

PFFV: The Global X Variable Rate Preferred ETF invests in a broad basket of U.S. variable rate preferred stocks, providing benchmark-like exposure to the asset class.

PFFD: The Global X U.S. Preferred ETF invests in a broad basket of U.S. preferred stocks, providing benchmark-like exposure to the asset class.

SPFF: The Global X SuperIncome Preferred ETF invests in 50 of the highest yielding preferred stocks in North America.

1. Bloomberg, L.P. (n.d.). [S&P US Variable Rate Preferred Index] [Data set]. Retrieved on May 31, 2022 from Global X ETFs Bloomberg terminal.

2. Ibid.

3. Ibid.

4. Bloomberg, L.P. (n.d.). [S&P US Floating Rate Preferred Index] [Data set]. Retrieved on May 31, 2022 from Global X ETFs Bloomberg terminal.

5. Bloomberg, L.P. (n.d.). [Variable rate preferreds measured by ICE US Variable Rate Preferred Securities Index, high yield bonds measured by Bloomberg US Corporate High Yield Index] [Data set]. Retrieved on May 31, 2022 from Global X ETFs Bloomberg terminal. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest)

6. Board of Governors of the Federal Reserve System. (2022, June). 2022 Federal Reserve stress test results. U.S. Federal Reserve.

7. Bloomberg, L.P. (n.d.). Financials represented by S&P 500 Financials GICS Level 1 Index. ‘Average’ calculated as weighted average of Long Term Issue Credit Ratings. Retrieved on May 31, 2022 from Global X ETFs Bloomberg terminal.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.