Investors, traders, savers, and home-buyers are fixated on Federal Reserve decision-making, especially in the wake of summer market volatility. The Ticker Tape asked Chris Larkin, Managing Director, Fixed Income at TD Ameritrade, for his take on the potential impact of higher rates on bonds, bond portfolios, and credit markets.

TT: Generally, what role do interest rates play in our lives?

CL: We’ve been living in a time of historic lows in interest rates. That’s great news for borrowers, not so great for savers. Student loans, auto loans, and mortgages are just some of the beneficiaries of these low interest rates. Just 15 years ago, according to Mortgage News Daily, mortgage rates on a 30-year-fixed mortgage was about 8%. Today, they average around 4%. On a $250,000 mortgage, that equates to a yearly difference of $10,000, or $300,000 over the life of your loan.

As for savers, this low-rate environment has been painful. That’s especially true for retirees who depend heavily on the income they generate to sustain the lifestyle they worked so hard for. In the year 2000, five-year CD rates averaged about 7.5%. Today you can get 2.25% at most on a five-year CD.

TT: What could rising rates mean to fixed income investors?

CL: A rise in interest rates does not impact all fixed income investments equally. Generally, the longer the maturity—or duration—of your bond or bond funds, the greater the rate impact will be. For investors who hold bonds to maturity, a rise in rates will not have an effect on the coupon payment that you receive, or the principal you receive when that bond matures, barring any credit event (such as default) that may occur. However, your bond will likely fall in value when rates rise. So if you need to liquidate your bond prior to maturity, you may incur a loss on your investment. This matters in the current climate because, hungry for yield in a low-rate environment, some investors bought bonds with maturities that weren’t consistent with their liquidity needs and risk tolerance. We strongly recommend understanding the impact of a rate rise on your own portfolio with the help of a TD Ameritrade professional.

As for bond funds, investors might expect a loss in principal in a rising-rate environment. However, for long-term investors, those bond funds will likely target new investment in bonds with higher rates as the bonds with lower yields in their portfolios begin to mature. Over time, long-term investors could ideally recoup short-term losses with the higher yielding bonds that are in their bond funds.

TT: With interest rates where they are today, is it better to wait until rates rise to buy a bond?

CL: In a low interest rate environment, many investors play the “waiting game” hoping to take advantage of future, presumably higher interest rates. Although it may not be advisable for investors to always be 100% invested, waiting to invest will almost always result in lost income. The longer your money sits static, the higher the rates will have to grow to make up for what you missed while waiting.

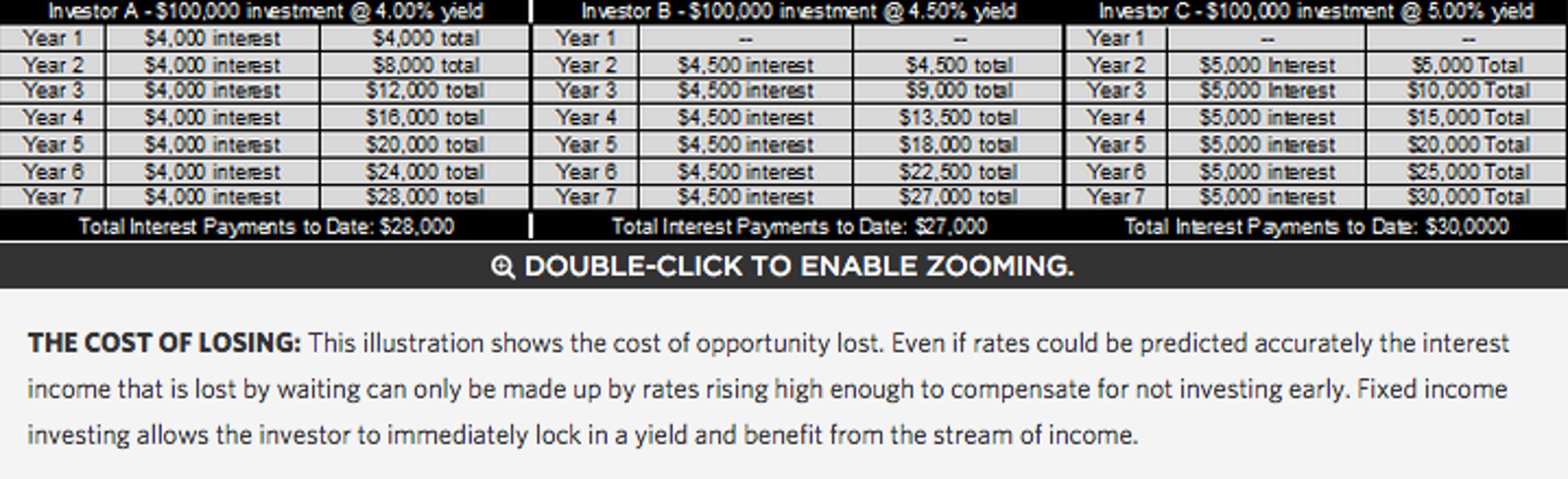

Below is an example of three investors who purchase bonds with similar features at different times:

Investor A purchased a 7-year bond at the current market rate of 4.0% and Investor B decided to wait until the following year and purchased a 6-year bond when rates were at 4.5%. In this scenario it would take Investor B more than six years for his income to catch up to Investor A. Investor C also waited one year and income caught up to Investor A after five years when the income would surpass that of the other two investors. To realize this advantage, interest rates would have risen a full percentage point in one year. These scenarios assume the investors hold the bonds to maturity.

TT: What personal finance actions might make sense with interest rate increases?

CL: Most important is that you have a plan before interest rates rise. A well-diversified portfolio is typically the best defense against market movements. The average investor is not able to time the market effectively.

Investments in fixed income products are subject to liquidity (or market) risk, interest rate risk (bonds ordinarily decline in price when interest rates rise and rise in price when interest rates fall), financial (or credit) risk, inflation (or purchasing power) risk and special tax liabilities.

Market volatility, volume, and system availability may delay account access and trade executions.

Past performance of a security or strategy does not guarantee future results or success.

Options are not suitable for all investors as the special risks inherent to options trading may expose investors to potentially rapid and substantial losses. Options trading subject to TD Ameritrade review and approval. Please read Characteristics and Risks of Standardized Options before investing in options.

Supporting documentation for any claims, comparisons, statistics, or other technical data will be supplied upon request.

The information is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade. Clients must consider all relevant risk factors, including their own personal financial situations, before trading.

TD Ameritrade, Inc., member FINRA/SIPC. TD Ameritrade is a trademark jointly owned by TD Ameritrade IP Company, Inc. and The Toronto-Dominion Bank. © 2015 TD Ameritrade IP Company, Inc. All rights reserved. Used with permission.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.