Auto loan debt is the third largest source of debt in the United States. Auto loans are surpassed only by mortgages and student loan debt. For many Americans, paying for a car outright might be a break-the-bank purchase. Financing can make a car purchase a reality.

Many Americans inevitably choose that option, though it’s certainly possible to save for a car penny by penny.

First, Understand the Overall Cost of Buying a Car

Saving for a car goes beyond knowing all the best ways to save money. In fact, it’s a commitment that requires careful thought and planning. It’s important to budget for insurance, maintenance, monthly fees, a down payment, and fuel costs.

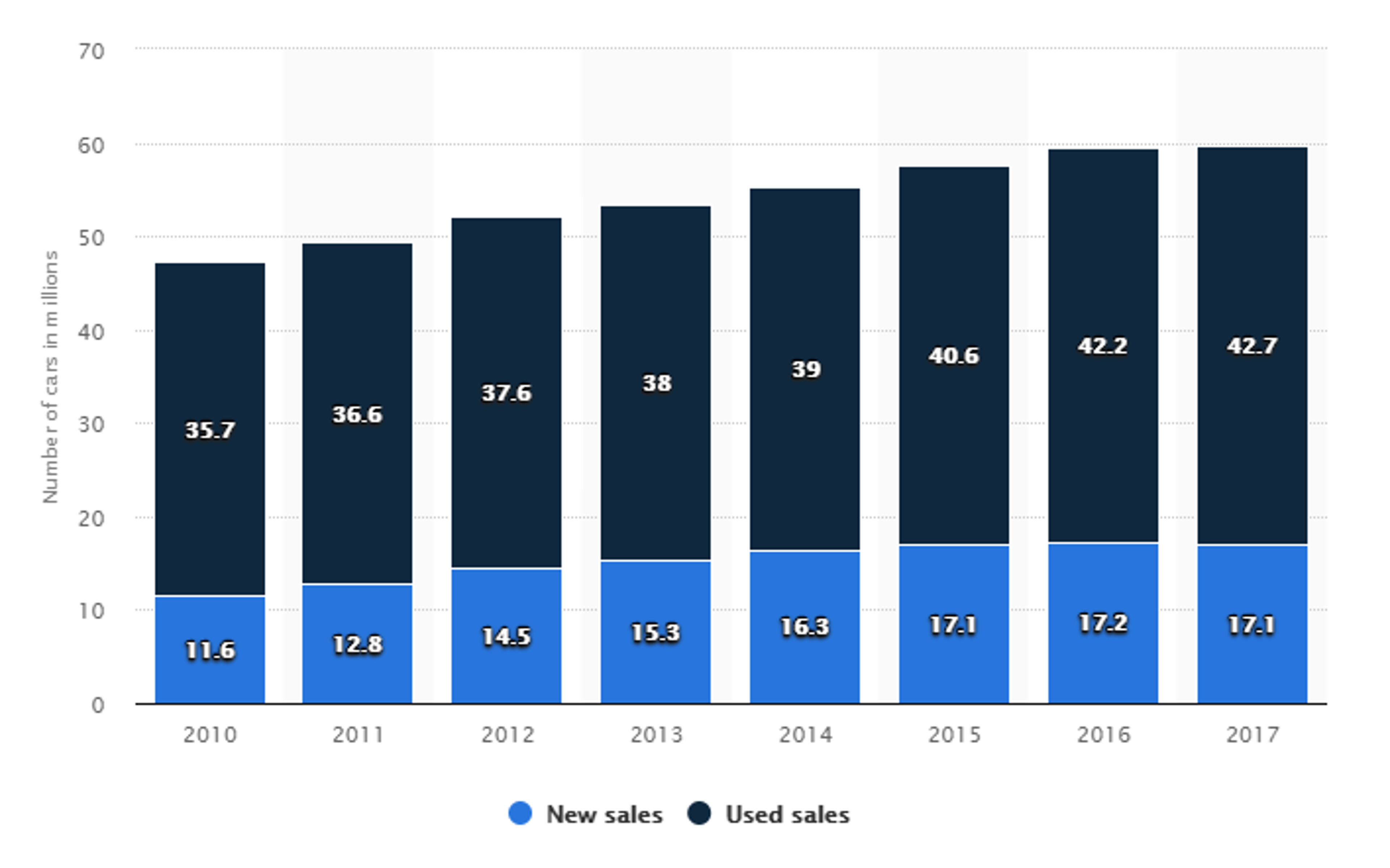

Number of new and used light vehicle sales in the United States from 2010 to 2017.

Used car purchases exceed new purchases year after year by a wide margin. Whether you want something new or used is entirely a matter of preference and financial feasibility. Used cars may need more maintenance and have a shorter economic life.

Newer cars, on the other hand, are more expensive and could require you to take out a loan to purchase.

Lease vs. Buy

Leasing has become the norm for those who may not be able to afford to purchase a new vehicle. If you aren’t able to make a very big down payment. Leases can be more affordable than buying. According to Consumer Reports, monthly lease payments are almost always lower than auto loan payments.

The process of leasing and buying are pretty similar. To buy a new car, you have to pay the full price of the vehicle to

Leasing requires you to only pay the amount of depreciation the vehicle is expected accrue.

You lose some of the freedom you get with a lease compared to when you own. Part of being a leasee is that you must be cognizant of how many miles you put on your vehicle as well as general wear and tear.

You’re also locked in for a term and will have to pay substantial fees if you end your lease early. You’ll also incur some other fees, including money due at signing, a security deposit, down payment and even acquisition fees.

Many costs can be negotiated and the amount of money due at signing is typically fixed by the dealership beforehand.

Down Payments and Monthly Payments

Twenty percent of the total purchase price of the vehicle is considered an ideal amount for a car down payment. The price range of used cars varies, but the average cost of a new car is $35,742. A good benchmark for an ideal down payment of $7,148.

Monthly lease payments are more likely to be lower than monthly loan payments.

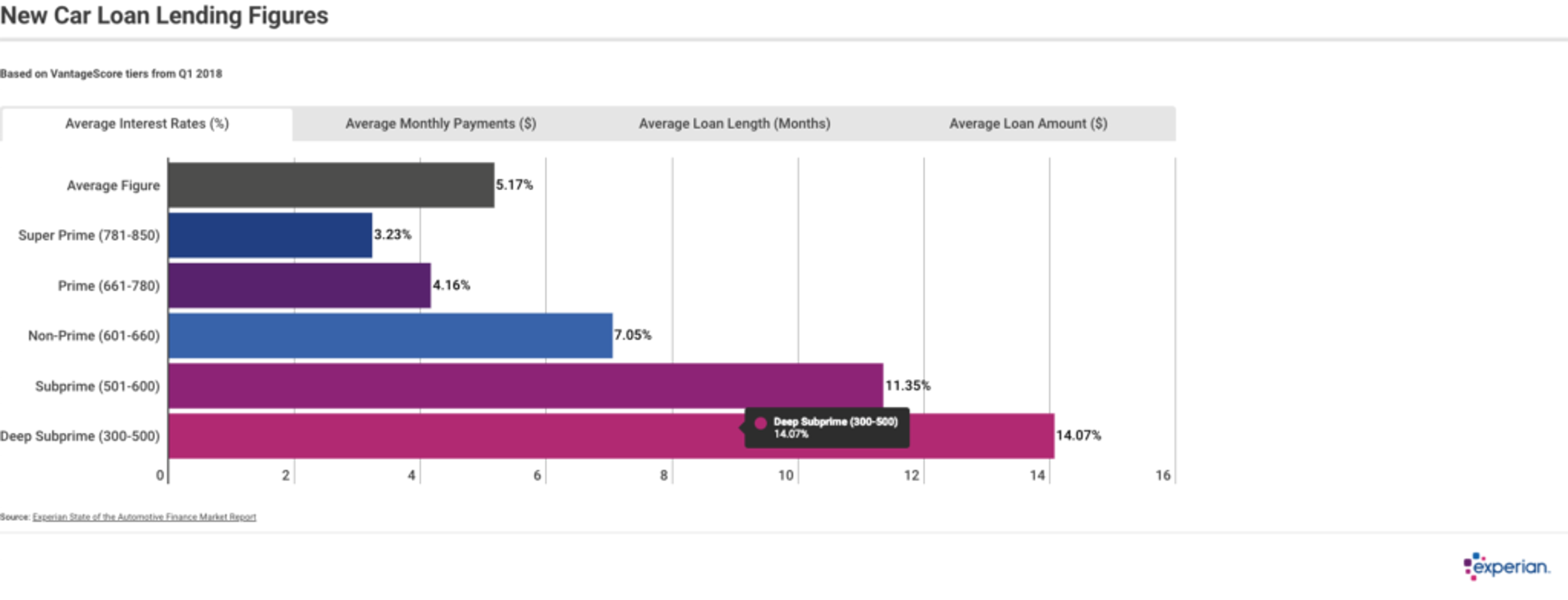

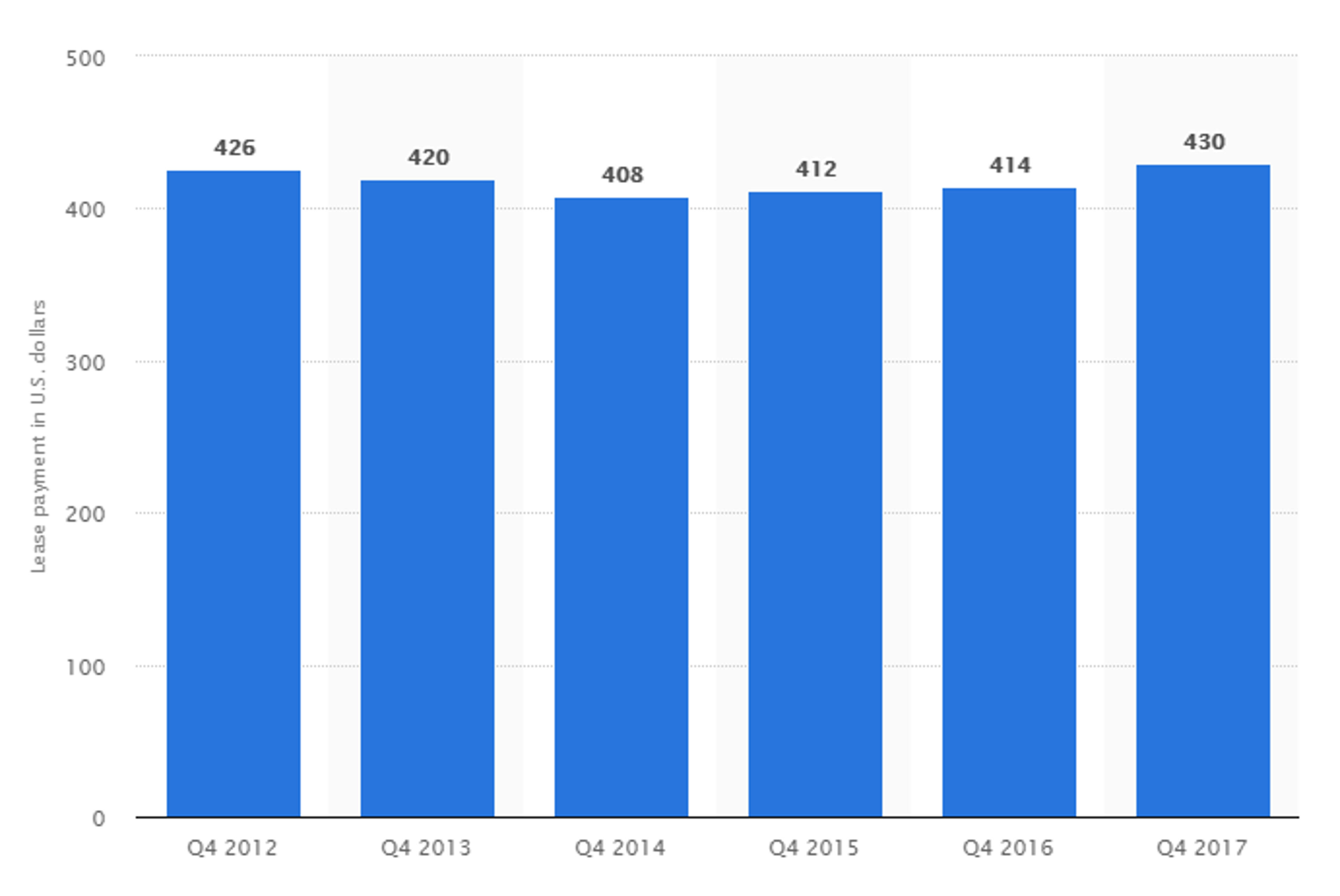

The Experian infographic above shows how the average monthly payment for a car loan has exceeded $500, whereas a lease payment in 2017 was $430.

Car Insurance

When you finance a vehicle, you can expect to pay for full coverage auto insurance, and it is important to factor in this monthly cost.

AAA reports that the average annual cost for auto insurance is roughly $1,115, or $93 a month. Luckily, insurance is one area where you can shop around, and there are many companies such as Progressive which allow you to shop and compare car insurance rates.

Car Maintenance

The same AAA report found that when surveyed, one-third of Americans reported that they would be unable to pay for an unexpected repair for their vehicle at least once in their lives.

The average reported annual cost of routine (and unexpected) maintenance averages $1,186. Maintenance staves off depreciation and assures that your used vehicle retains more value if decide to trade it in or sell down the road.

Fuel Costs

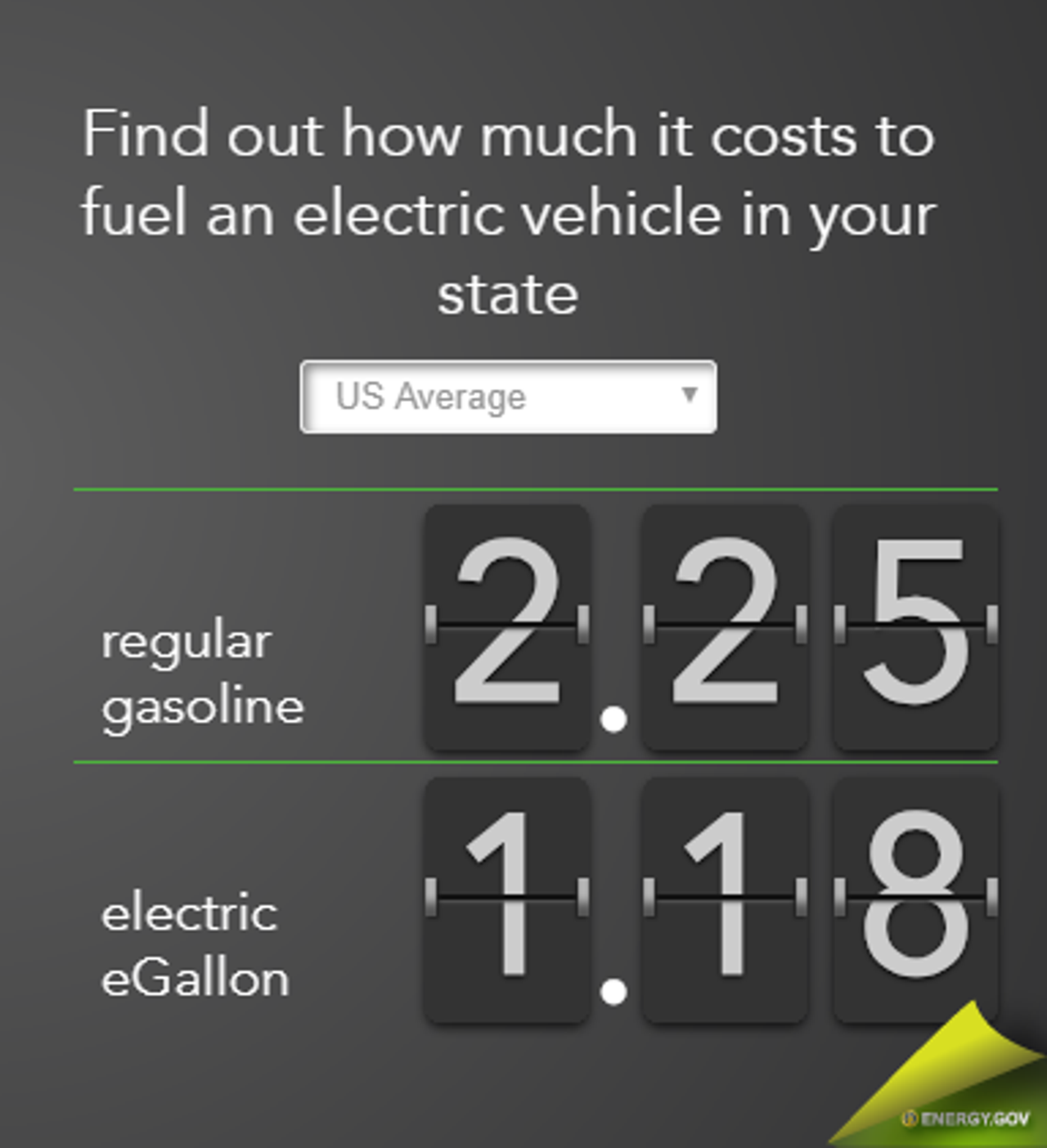

You’d be hard pressed not to see electric cars or flex-fuel vehicles driving down any road in any major city. It might be time to join the club or at least consider alternative fuel vehicles.

At any rate, it’s a good idea to pay close attention to price trends to make sure the fuel you burn won't burn a hole through your pockets.

To better understand the cost of fuel, check your average price per gallon in your state with the U.S. Department of Energy’s eGallon tool.

Make a Budget to Save for a Car

It’s crucial to understand all the associated costs of car ownership if you want to save up for one. Decide what you expect to spend each month and plan your budget to determine how much you can comfortably save.

Know Your Timeline

Consider your timetable. It’s the first step you can take to create your budget. Want to have that convertible by the start of summer? Need that minivan before school starts back up? Then create a budget accordingly and have a decent amount of money set aside for a down payment.

Beyond these benchmark goals, it’s important to know when you plan to buy because it can guide you into the best way to save money in just a few steps.

Create a Budget

You know your costs, and you know your timeline — now is the time to sit down and plan how you will afford all these costs when the time comes.

The best way is to compare how much you bring in each month against how much you spend. If your hours are steady or you are salaried, then this is as simple as adding your paychecks and any supplementary income together. Look into how to set up direct deposit.

If you don’t receive steady paychecks, you may need to look back at bank statements and take into account any seasonal effects on income to get a good understanding of what you bring in.

Next, add your monthly bills and regular expenses together, taking into account regular expenses such as groceries. Pay close attention to what you spend money on. Could you benefit from brewing your own coffee more often? Do you really need the fastest internet speed?

Opportunities to save money are everywhere, and as you think about making a large purchase, many of your wants should be carefully considered. You may also want to save money for other things at the same time. If you’re saving for college, for example, know the best 529 accounts in addition to other investment opportunities so you don’t spread yourself too thin.

Figure out what you have left over at the end of the month and budget the rest into your car savings fund. Don’t budget yourself broke, and to be responsible, we recommend you leave about 10% of your monthly income free in case of emergencies. Learn more about how to create a budget.

Track your budget and keep yourself accountable, which can be the hardest part of budgeting. Technology has made many aspects of budgeting a breeze, and using one of any number of budgeting apps will ensure that your savings goals are met.

Stow Your Money Away

Your surplus of cash has to go somewhere, but are there more options than savings accounts? Opening up a CD is a definite possibility. Terms can be as short as six months, though this money cannot be accessed for the duration of the term.

The rates are not the highest, but you’ll find out that there are many low-risk options available to you if you’ve learned how to start investing.

Explore Side Hustle Opportunities

To save up for a car, consider doing a side hustle. A side hustle can provide you with additional income that can be specifically allocated towards your car savings goal. By taking on extra work, whether it's freelance gigs, part-time jobs, or selling handmade crafts, you can accelerate your car savings and reach your goal faster.

Trade In or Sell Your Old Car

Trading in your old car at a dealership can provide you with valuable credit towards the purchase of your new car. This can significantly reduce the overall cost of the new vehicle and make it more affordable for you.

Secondly, selling your old car privately can help you generate cash that you can put towards your new car fund. By listing your car on online platforms or advertising it locally, you can attract potential buyers who may be interested in purchasing your vehicle at a fair price.

Getting the Car You Need

All that’s left is to put your plans into action. No matter your financial situation, research and proper planning will help, but ultimately, the car you buy must be within your means. Follow these tips to cruise toward your new car and so your bank account doesn’t run on empty.

Frequently Asked Questions

How much money should I save before buying a car?

The amount of money to save before buying a car varies based on personal finances and preferences. Before buying a car, it is important to have enough savings to cover the down payment, taxes, registration fees and insurance costs. It is also wise to have an emergency fund for unexpected expenses. Assessing your budget and considering your financial situation and car model will help determine the appropriate amount to save.

How can I save money for a car easily?

There are several ways you can save money easily for a car. First, create a budget and track your expenses to identify areas where you can cut back and save more. Consider reducing unnecessary expenses such as eating out, entertainment, or shopping. Additionally, automate your savings by setting up automatic transfers from your paycheck to a separate savings account dedicated to your car fund. Another strategy is to look for ways to increase your income, such as taking on a side gig or selling unused items. Lastly, consider researching and comparing car prices to find the best deal and save money in the long run.

How long should it take to save up for a car?

The time it takes to save up for a car can vary depending on individual financial circumstances and goals. It could take several months to a few years, depending on factors such as income, expenses, and saving habits. It is important to create a budget, set saving targets, and consistently save a portion of your income towards the car purchase.