By Erik Norland

The 1980s and 1990s often featured Fed Chairs Paul Volcker and Alan Greenspan advising the U.S. Congress that if they wanted to lower interest rates, they needed to rein in budget deficits.

Fast forward three decades, and we see that mantra flipped on its head. Now, Fed Chair Jerome Powell tells Congress that the economy needs more fiscal support to offset the pandemic, even as the US budget deficit is already at a record 14% of GDP.

There are currently several proposals for a pandemic relief bill ranging from the “skinny” $500 billion Senate proposal to the $1.8 trillion White House offer to the $2.2 trillion stimulus advocated by the majority in the House of Representatives. Every $200 billion in additional stimulus adds about 1% of GDP to the deficit. As such, either the proposal from the White House or the House of Representatives could bring the deficit to 23-25% of GDP (Figure 1).

Figure 1: Certain proposals could take the deficit to 23-25% of GDP or higher

This raises questions for bond investors that relate to the Fed. When the first stimulus package passed Congress in March, the Fed bought much of the newly issued debt and that helped to keep long-term bond yields low and stable (Figure 2). But would the Fed buy such a large portion of a second round of stimulus? And, if not, will bond yields rise?

Figure 2: Fed buying probably depressed bond yields in the face of unprecedented debt issuance

A case can be made either way. On the one hand, equity prices had fallen 30% and credit spreads were widening back in March. The Fed bought bonds not just to absorb rising Federal debt but also to stave off a credit crunch. Now, stocks are near record highs and credit markets are functioning well, so the Fed might be less inclined to do a second massive round of QE. On the other hand, between 2009 and 2014, the Fed did three successive waves of QE and the last two came about even as equity prices were rising and the economy recovered (Figure 3). In addition, looming consumer and business defaults could also justify more Fed buying.

See also: How to Invest Your $1,400 Stimulus Check

Figure 3: Would the Fed buy as many bonds from a second fiscal stimulus?

Essentially bond investors face several layers of uncertainty:

- What kind of stimulus bill might eventually be signed into law?

- When might Congress and the White House reach an agreement?

- How much of the newly issued debt might be absorbed by the Fed?

- How much would the yield curve steepen if the Fed doesn’t buy a significant portion of the debt?

In the meantime, bond investors will watch closely for signals from Washington. And it’s not just bond investors who will be impacted. A steep rise in long-term bond yields could push investors away from stocks and precious metals.

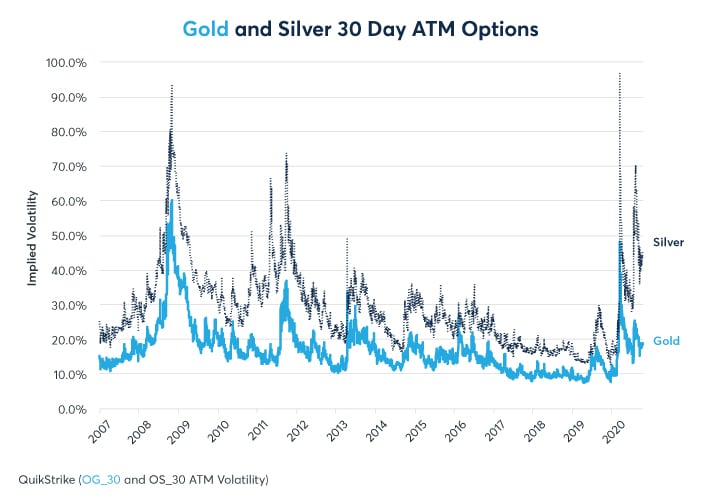

Options prices also are reflecting investor concerns. As the stimulus talks in Washington continue, implied volatility on long-term bonds has begun to rise from recent lows (Figure 4). Equity and precious metals implied volatility also remains high by historical standards (Figures 5 and 6).

Figure 4: Implied volatility on long-term bonds has been rising again

Figure 5: Equity index implied volatility remains high despite stocks being near record highs

Figure 6: Gold and silver implied volatility remains at elevated levels

Bottom Line

- Outcome of fiscal talks remains unclear

- Deficit could expand to 23-25% of GDP or more

- Not clear how much more debt the Fed would absorb on its balance sheet

- A steeper yield curve could hamper stocks, gold and silver

- Options prices remain elevated

To learn more about futures and options, go to Benzinga’s futures and options education resource.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.