Expectations about future dividend payments by S&P500® corporations have been changing with equity prices, yet with some key differences. Equity prices have been strongly supported by the Federal Reserve’s (Fed) massive fixed income asset purchases, which have resulted in much lower long-term US bond yields, lowering the bar for equities. Arguably, dividend expectations are less impacted by Fed activity, and provide a robust view and different perspective on how equity market participants are viewing the likely pace of rebuilding the economy. It also helps to explain the apparent disconnect between the V-shape equity price rebound in Q2/2020 compared against a less optimistic view of what is happening in the real economy with many challenges emerging to the re-opening and re-building effort.

In this report, we track the history of dividend expectations through the pandemic period in 2020 and appreciate the context from the pre-pandemic era. We also examine the influence of Fed activities on equity prices and then discuss changes corporations are making to their business models that support these dividend expectations even if the economic rebuilding goes slower than hoped for. These insights will help us understand the divergence among equity prices, dividend expectations and the potential pace of the economic recovery.

Tracking Dividend Expectations

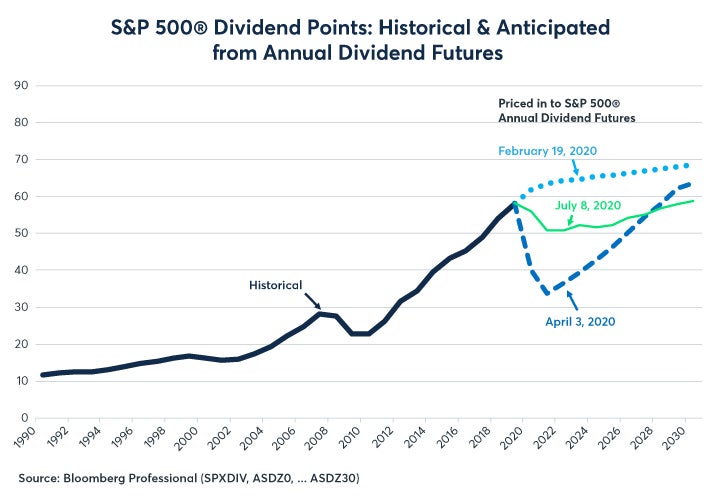

The US equity market hit a low on March 23, 2020, at 2220 on the settlement of June S&P500® E-mini futures. Two weeks later, on April 3rd, expectations for future dividend payments, implied by S&P500® annual dividend index futures, reached their lows. At that point in time, investors priced that dividend payments would fall from 58.22 index points in 2019 to 40.0 in 2020 and to 33.75 in 2021 – a 42% drop over a two-year period and roughly twice as big as the decline in dividend payments that occurred between 2008 and 2010 in the wake of the global financial crisis.

When expectations hit bottom in early April, investors expected a steep fall in dividend payments. Yet they also anticipated a substantial rebound as the decade wore on. At the bottom on April 3, 2020, annual dividend index futures priced dividend payments reaching their 2019 high watermark of 58.215 points again by 2028 and that they would go on to new highs of 63.6 by 2030.

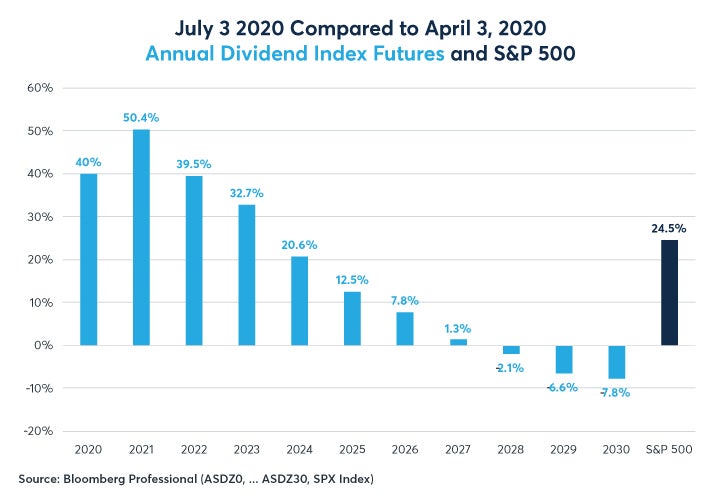

Between April 3 and July 6, the S&P 500® rebounded by 25.5%, approaching its record high from February. As stocks rallied, expected dividends rebounded as well, although only at the nearby part of the dividend futures curve. As of July 6, investors in S&P 500® annual dividend index futures priced that dividends would hit 55.8 index points in 2020 and 50.55 in 2021. Compared to the low point in investor expectations on April 3, that’s a 40% increase for 2020 and 50% increase relative to 2021.

Looking further ahead, even with S&P500® stock prices 25% off their lows and nearing a record high, investors were less optimistic about dividend payments in 2028, 2029 and 2030 than they had been in early April. As of early July, investors priced 2030 dividends at 58.1, slightly lower than they had been in 2019 and about 9% less than where investors had anticipated them when the market hit bottom in early April (Figures 1 and 2).

Figure 1: Investors price flat dividends for the 2020s decade after a near-term dip

Figure 2: Since expectations hit bottom in April, investors expect a smaller dip, slower recovery

Overall, what we have seen is a flatlining of dividend expectations going further out in time. For the moment, investors appear to believe that dividend payments for 2020, 2021 and 2022 will be much better than they had feared three months earlier. However, investors also anticipate that subsequent growth in dividend payments will remain extremely weak for the rest of the decade.

Putting Dividend Expectations in Context

In fairness, dividend payments are coming off a spectacular decade. Dividend payments by S&P500® companies grew by 37% during the 1990s. They grew a further 37% between 1999 and 2009. However, between 2009 and 2019, they expanded by 155%. Exceptionally high corporate profit margins of around 10% of GDP combined with a decade-long expansion that began in 2009 propelled their growth. Even when the equity market peaked in February 2020, investors did not expect that dividends would keep pace with this past decade’s rate of advance. At that point investors expected about a 20% further rise in dividend payments between now and 2030. Now they anticipate that dividend payments will be fairly flat in nominal terms and will, in fact, decline after inflation is taken into account.

One might look at the 2020s dividend payments implied by annual dividend index futures in a rather pessimistic light, suggesting slow growth and an L-shaped economic recovery. Remember, however, that dividend payments began the 2020s at records highs after unprecedented growth in the 2010s. But there is much more to this story of how equity prices and dividends relate to the real economy when one considers both the actions of the Fed as well as the adjustments that corporations are making to repair bottom lines in the post-pandemic era.

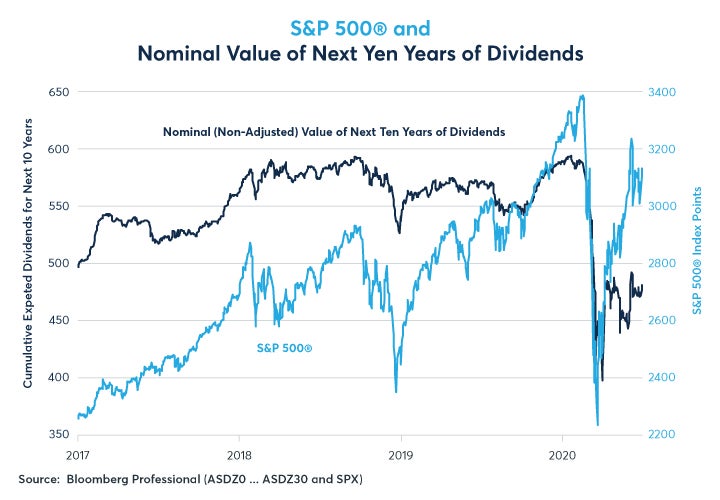

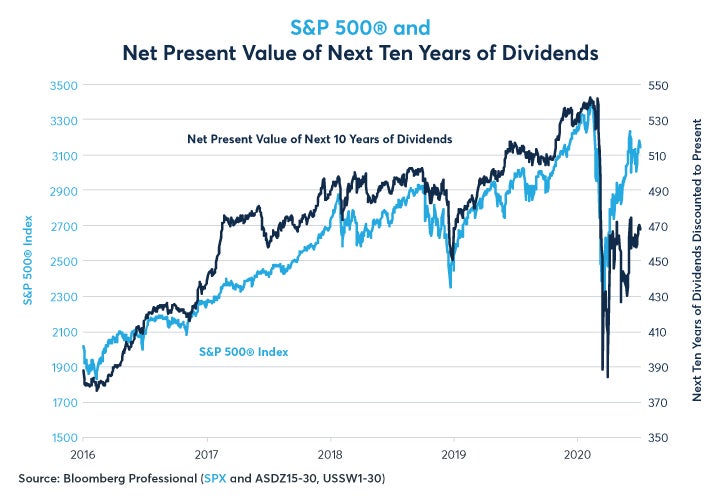

The S&P 500® index has dramatically outperformed the sum of dividends in the next 10 years’ worth of S&P 500® annual dividend index futures since the beginning of 2017. In fact, compared to three years ago, when the sum of the next 10 years’ worth of dividends came to around 500 S&P index points, investors are actually less optimistic now than they were then. As of early July 2020, the next 10 years of dividend payments is expected to sum up to about 480 S&P 500® index points, or about 4% less than they were 3-1/2 years ago. Meanwhile, the S&P 500 has gone from 2,250 to nearly 3,150 (Figure 3). How can stocks go up so much when expected future dividend payments are, at best, stagnant?

Figure 3: Since early 2017, the S&P 500 is +37%; expected dividends in the next 10 years are down 4%

Taking Fed Asset Purchases into Consideration

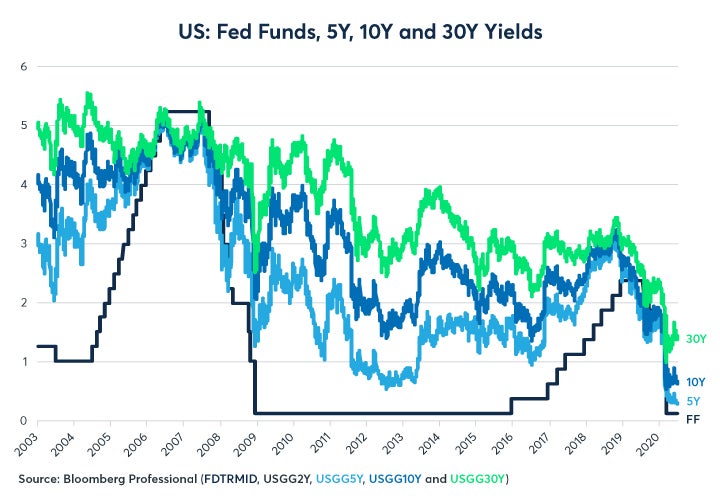

Much of the rise in stock prices has to do with falling interest rates. Since early 2017 interest rates have fallen across the curve. Short-term rates, which rose throughout 2017 and 2018, are back to near zero. Ten-year yields have fallen from 2.5% to around 0.65% and 30-year yields have dropped from 3% to around 1.4% (Figure 4).

Figure 4: Interest rates have fallen across the yield curve

Falling long-term rates boost the net present value (NPV) of future dividend payments when those payments are discounted back into the present moment. In fact, from early 2017 until May 2020, the NPV of future dividends closely tracked the value of the S&P 500 index (Figure 5). As interest rates plunged, the NPV of future dividends rose, taking the equity market higher along with it. In May and June 2020, however, the NPV of dividends stopped advancing and stocks have gone higher anyway.

Figure 5: NPV of dividends and the S&P 500® moved together until May and have diverged since

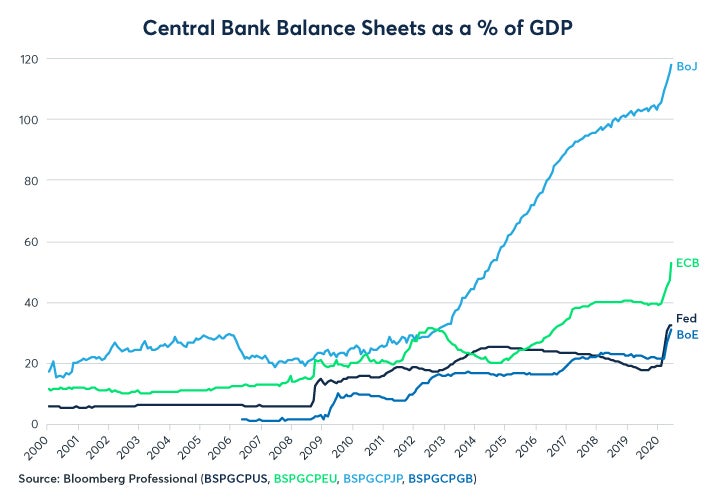

This sort of divergence has no precedent in the past 3-1/2 years. More than likely, the divergence is related to the expansion of central bank balance sheets in the US and elsewhere. The Fed has not pushed long-term US Treasury note and bond yields toward zero or negative rates as in Europe and Japan. Yet the Fed is doing much more than purchasing US Treasury securities. It is buying corporate debt, including “fallen angel” high-yield bonds, along with municipal bonds and mortgages. As the Fed has purchased more and more credit products, this narrows the spread between Treasuries and non-investment grade corporate debt, further encouraging investors to buy equities in search of return.

An unanticipated consequence of the massive Fed asset purchases, and an implication of the divergence between the S&P 500 and NPV of future dividends is that equities are carrying a greater degree of duration risk than in the past. That is, the massive expansion of the Fed’s balance sheet increases the risk in both fixed income and equity markets should the Fed change course down the road. Specifically, there are heightened long-duration risks for equities later in the decade when the economy has largely recovered as to whether the Fed will allow its balance sheet to shrink (or not), and whether the Fed will adjust short-term interest rates higher at some point.

Figure 6: Central bank balance sheets have expanded and the BoJ is leading the way

Corporate Adaptations for a Post-Pandemic World

The story of the divergence of longer-term dividend expectations relative to current equity prices is not complete without appreciating the strategic steps that corporations are taking. The mega-corporates in the technology sector have mostly benefited from the pandemic-accelerated shift toward online activity. Across the rest of the economy, some companies are holding their own while many others in the transport, hospitality, and tourism businesses have been hurt badly.

What we have observed, though, is that the pandemic-induced economic shutdown forced virtually every company to react quickly to the changed circumstances. Both consumers and corporations will behave differently from the past in the post-pandemic world. Stressful periods, like the pandemic shutdown raise serious challenges and bring out the best in problem-solvers. Many lessons that were learned during the pandemic shutdown crisis are now being applied as long-term strategic adjustments to allow corporations to adapt to our changed world. The lessons learned may lead to an era of innovation and increased corporate efficiency. We will note just a few examples to highlight this insight.

Work from Home. Where it was possible to work from home (WFH), many companies have seen increases in productivity. Meetings are shorter. There is more focus on tasks at hand. The qualified success of WFH is likely to lead to more flexible time schedules where possible, a reduced need for office space, a reduction in business travel compared to past practices, among other changes. As these lessons are implemented by companies, there will be efficiency gains.

Supply Chain Redesign. The pandemic shutdown disrupted supply chains around the world, many of which were already suffering from the US-China tariff tensions. Supply chains are complex and cannot be redesigned overnight. Companies may choose to diversify their supply chains, seek shorter routes, locate parts manufacturing and assembly plants a little closer to the where the products will be sold, etc. The dependability of supply and transportation logistics will be more carefully balanced against seeking the location with the lowest cost of production. While this may be seen a step back from globalization, any supply chain redesign is more likely to reflect increased global diversification. Some countries may see some new job creation, such as Mexico due to its proximity to the US, as well as a few of the smaller Asian countries that may pick up some production that was formerly inside China.

Just in Time Inventory. Keeping inventories as slim as possible did not work as anticipated in the pandemic shutdown due to supply chain disruptions. Balancing inventory planning with a heightened expectation of potential swings in demand will get considerable attention in the post-pandemic era to protect revenue streams against input shortages.

Leaner executive decision structures. The speed of economic upheaval from the pandemic shutdown was unprecedented. Many companies had to streamline decision structures so they could react faster than they ever knew they could. Less bureaucratic decision-making offers a chance for improved adaptability and increased innovation.

Essentially, many corporations are facing some tremendous headwinds to rebuild their earnings as the re-opening of economies goes slower than initially hoped and anticipated. Set against the reality of slower re-opening prospects are the strategic steps corporations are taking to adapt. Corporations are likely to emerge several years down the road as significantly more efficient, meaning that they can right-size their businesses to meet the dampened demand from cautious consumers and still rebuild earnings. Dividend expectations are telling us that this path will be difficult, yet as corporations improve their operations earnings growth may outperform economic growth. Monitoring dividend expectations can give us insights into how these developments are evolving and help us understand the disconnect between equity prices and prospects for the real economy.

Bottom Line

- Expected dividends for 2020-2022 have rebounded 40-50% off of April lows.

- Anticipated dividends have fallen for 2028-30 since stocks hit Feb-March lows.

- Equities have risen in part because long-term bond yields are much lower than pre-pandemic levels.

- The dividend expectations gap with equity prices suggests that equities may carry significant duration risks akin to those of long-term bonds.

- Corporations are not sitting idle; they are implementing lessons learned from the pandemic-induced shutdown to right-size their companies in ways that may lead to a faster recovery in earnings than the recovery in economic activity.

To learn more about futures and options, go to Benzinga's futures and options education resource.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.