The following post was written and/or published as a collaboration between Benzinga’s in-house sponsored content team and a financial partner of Benzinga.

With 2020 fast approaching, investors are looking for real estate opportunities that can potentially measure up to the rapid growth rate the industry has experienced in recent years, while wondering whether this growth will last.

The past decade has seen commercial real estate values soar to new highs as individuals and institutions alike increase their alt exposure to hard assets. Green Street Advisors’ weighted Commercial Property Price Index shows that current composite property values are over 35% higher than they were a decade ago. However, this historical rise presents new challenges for investors who are now entering the market.

In order to bring more clarity to this process, we will explore three macro trends that investors should be mindful of as they consider their next commercial real estate investment.

Economic Uncertainty Boosts Existing Rental Properties While Slowing New Construction

Estimates from the International Monetary Fund indicate that the global economy is poised for its slowest growth rate since 2008, and the IMF argues that persistent issues such as the U.S.-China trade war have sown discord into global markets. But while this current climate of uncertainty may dampen or destabilize stock prices through 2020, we believe that this same uncertainty may play a role in buoying existing U.S. residential and multifamily rental properties.

This viewpoint is supported by the fact that tariffs the U.S. has leveraged on basic material imports like steel and lumber have dramatically increased property construction costs. To this point, the National Association of Homebuilders has argued that tariffs against China alone constituted a $2.5 billion tax against the homebuilding industry.

This increase in construction material costs has reduced the construction pipeline and available inventory for single-family units in the U.S., particularly smaller, lower market starter homes in and around cities. In fact, according to the U.S. Department of Housing and Urban Development, recent single-family home construction rates are significantly below the 60-year average. At the same time, data from the U.S. Census Bureau shows that the average national vacancy rate for rental units is lower than it has been in over 30 years.

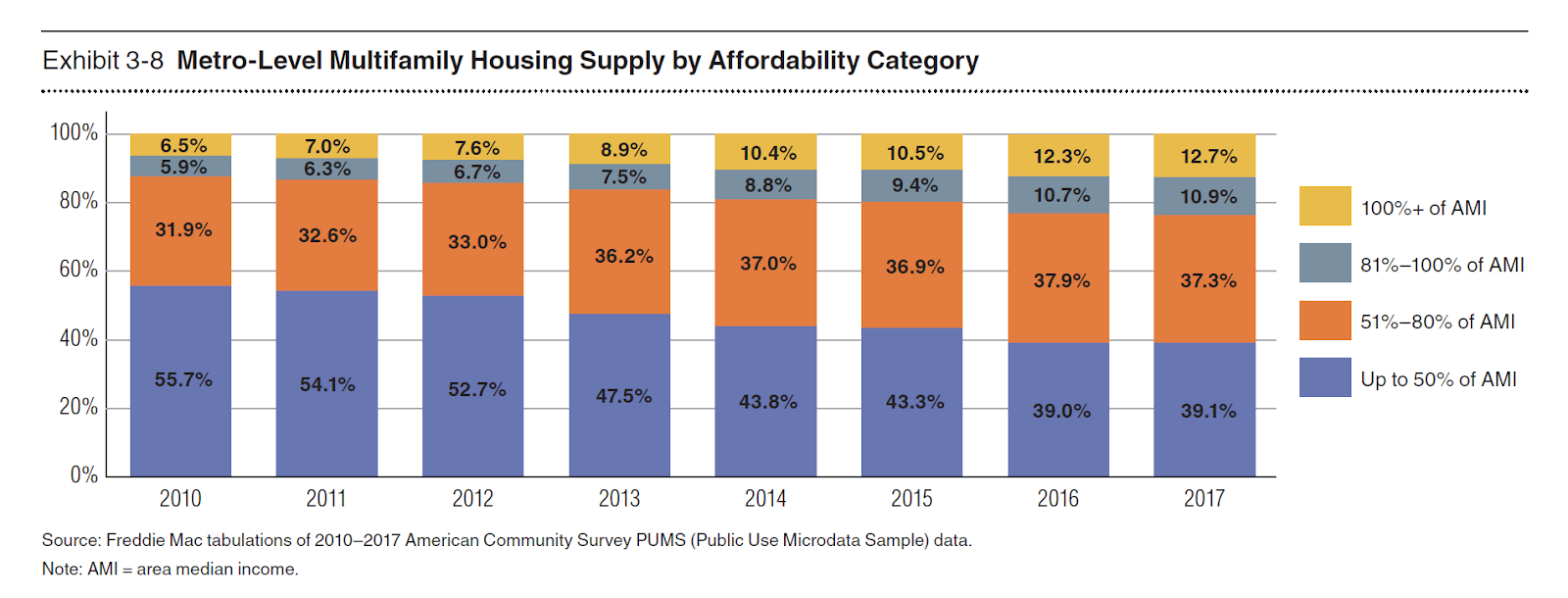

What this means is that prospective homeowners who can’t find suitable houses that match their purchasing power are continuing to rent at high rates. The trend has been most strongly felt in dense metropolitan markets, with cities like Denver, Seattle and Chicago seeing record-breaking absorption rates. Furthermore, as illustrated in the chart below, rent levels have continued to rise relative to households’ area median income, and households are having an increasingly hard time finding affordable housing options.

Metro-Level Multifamily Housing Supply by Affordability Category

The total effect of these influences is something of a perfect storm for multifamily developments, particularly for value-add projects which can effectively enhance a property’s appeal and rental rates while maintaining main street price accessibility. As economic uncertainties extending beyond global trade continue to impact households across the U.S., we believe investors should be looking at value-add projects which take advantage of these historically low rental vacancy rates and widespread tenant demand for convenient yet affordable multifamily units.

Influx of Private Capital Supporting Continued Real Estate Development

Private real estate investments may be better poised to weather ambiguous economic conditions relative to other asset classes thanks to an abundance of available capital from multiple sources, as institutional and individual investors alike increasingly turn to real estate.

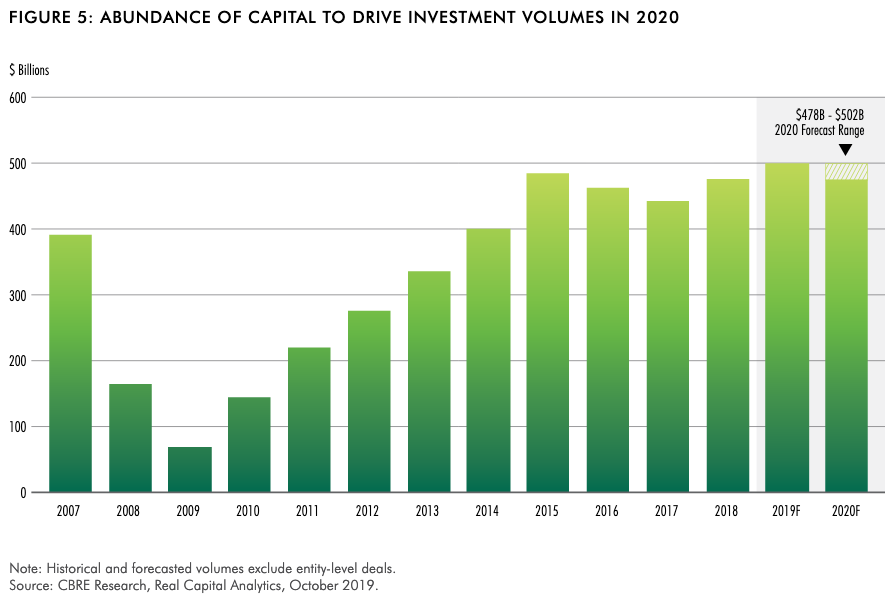

Current levels of commercial real estate borrowing are already at historic highs. A forecast from the Mortgage Bankers Association anticipates that by the end of 2019, the industry will see a record $652 billion in loans to income-producing properties, a 14% year-over-year growth rate. While this figure is anticipated to slow to about 7.4% in 2020, this projected growth rate remains impressive nonetheless, and with increased interest and accessibility private capital is expected to fill these potential funding gaps.

Abundance of Capital to Drive Investment Volumes, 2007-2020 (Projected)

An industry outlook report from PricewaterhouseCoopers asserts that “private capital will step in to fill the gap left by banks and insurers as a result of regulations that require reduction in their exposure to real assets.” The firm expects the share of institutional investment-grade real estate to expand by over 55% between 2012-2020. Further analysis done by commercial real estate analyst firm CBRE backs up this position, with the company’s 2020 outlook projecting that next year’s real estate investment volume will remain well above the 10-year average level and slightly below 2019’s high water mark of approximately $500 billion.

All this suggests that most institutional investors do not expect a substantial market downturn anytime soon, as banks and private investors continue to increase their exposure to real estate, albeit at a slightly slower year-on-year growth rate. As a result, we project the overall level of real estate investment to remain high, in large part due to the increasingly central role private capital will play in funding new projects.

A Sustained Shift Towards Smaller Metros

With more investors today realizing the potential advantages of investing in real estate, many of the major Tier 1 markets such as New York and San Francisco have gradually become oversaturated and increasingly difficult for the average investor to capitalize on. It’s no surprise, then, that many smaller investors have begun expanding their scope and actively pursuing deals in promising submarkets outside of the largest U.S. metros.

As a result, investment activity in Tier 2 cities such as Austin and Charlotte has surged in recent years due to these cities’ general affordability, regional economic growth, and lower levels of investment competition from institutional and foreign capital. Tier 2 cities with the strongest overall real estate prospects generally feature strong job and population growth, effective transportation infrastructure including walkable entertainment districts, and reputable educational institutions.

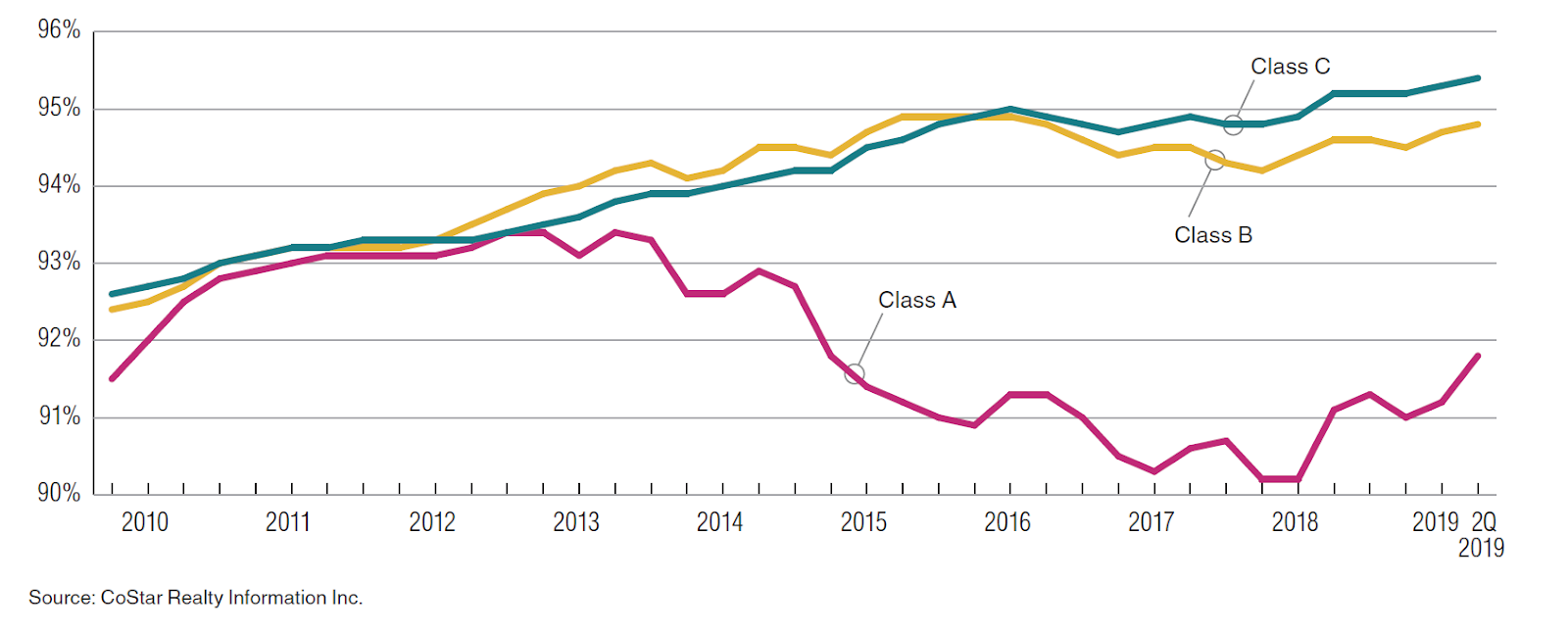

As a result, there has been a deluge of in-migration to other regions of the country such as the Sunbelt and other regions which can offer not only a more affordable cost of living but also an increasingly vibrant life marked by local urban renewal initiatives and community-oriented development. Taking a look at U.S. multifamily occupancy rates over the past decade in the below graph from CoStar, a global leader in commercial real estate research, we can see a precipitous drop in Class A occupancy rates while Class B-C levels gradually climb. This suggests that middle-market assets and less cost-prohibitive submarkets have the potential to outperform the wider market in 2020.

Multifamily Occupancy by Building Class, 2009–2019

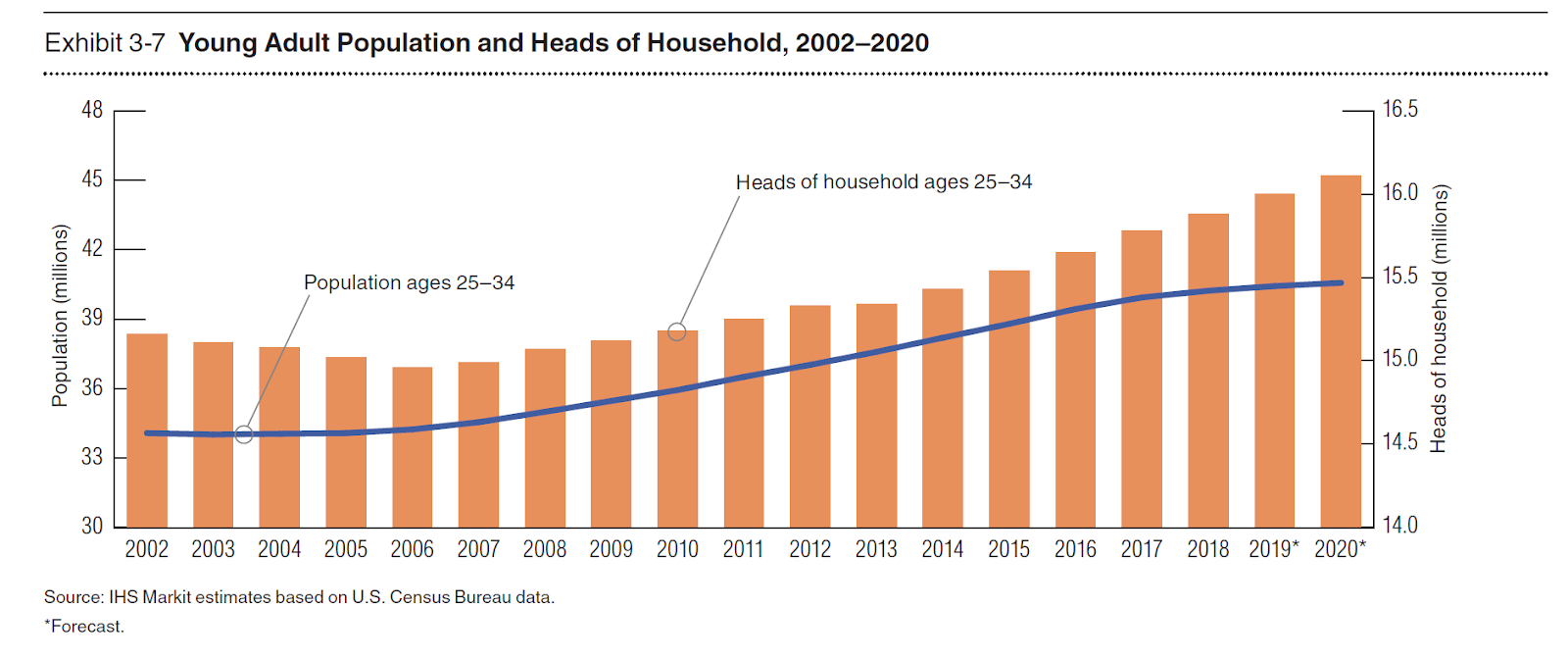

As a result, it shouldn’t be surprising to find that investors are placing an increasingly strong emphasis on multifamily properties in smaller metros with a population of less than 600,000, as stated in a recent CBRE report. This trend has also been driven in large part by macro shifts in population age, and according to IHS Markit estimates based on U.S. Census Bureau data, the proportion of households headed by younger individuals aged 25-34 has risen dramatically, as shown in the below graph. With the proportion of younger individuals leading households rising substantially over the past decade, many of these families are being priced out of the U.S.’s main urban centers.

Young Adult Population and Heads of Household, 2002-2020

Given these demographic shifts, it’s no coincidence that many major employers such as Google, IBM, and Accenture are expanding their local presence in mid-sized metros at the same time young and educated demographics flow into the same areas. Many smaller cities offer favorable tax policies for businesses and individuals alike in order to kickstart a virtuous cycle of local development, and individuals looking to invest in commercial real estate should consider looking at these smaller but potentially more rewarding markets as they continue to expand their economic and cultural clout.

Selective Investing & Cautious Optimism

While the efficacy of real estate investing relies on highly local conditions, the overall market is also subject to cyclical market conditions. The issue is, forecasting future market conditions is a notoriously imperfect science, and the U.S.’ economic environment remains a Rorschach test for market watchers.

What we can say with some certainty, however, is that while public-sector development and policy-creation are necessary for fostering a healthy real estate sector, private placements can also play a positive role in reallocating resources to projects which generate value for investors and local communities alike. In our opinion, this is especially true for the acquisition and repositioning of middle-market multifamily properties, which can cater to average Americans across all seasons and economic circumstances.

Investing in real estate? Visit iintoo for the latest offer

At iintoo, we focus on identifying value-add opportunities run by experienced sponsors who are willing to work with iintoo to create business plans that make sense for our investors. Our real estate investing platform gives individual investors the chance to directly invest in a broad range of pre-vetted properties spanning the entire U.S. and receive ongoing support and project updates throughout their entire investment lifecycle.

As we enter a new year, it’s important for individuals and companies alike to take stock of past portfolio performance and remain cautiously optimistic when assessing future prospects. iintoo wants to help bring clarity to this process and help you better understand your options and whether the investments you’re considering align with your risk profile and specific investment goals.

This is an advertisement for iintoo.com. Securities offered through Dalmore Group LLC, a registered broker-dealer and member of FINRA/SIPC. This is not an offer to buy, sell or trade securities. Investments are not FDIC insured, have no bank guarantee, and may lose value. For more information please read our full disclaimer.

The preceding post was written and/or published as a collaboration between Benzinga’s in-house sponsored content team and a financial partner of Benzinga. Although the piece is not and should not be construed as editorial content, the sponsored content team works to ensure that any and all information contained within is true and accurate to the best of their knowledge and research. This content is for informational purposes only and not intended to be investing advice.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.