By Ari Nazir and Christopher J. Keshian

Despite declarations made in the 1980’s that a vast “democratization of the stock market” was underway — wherein the masses gained significant shares of the market through investment vehicles such as mutual funds, IRAs, and 401(k)s — the share of the population owning stock is still shockingly low.

As stated by a 2012 Economic Policy Institute article by Heidi Shierholz:

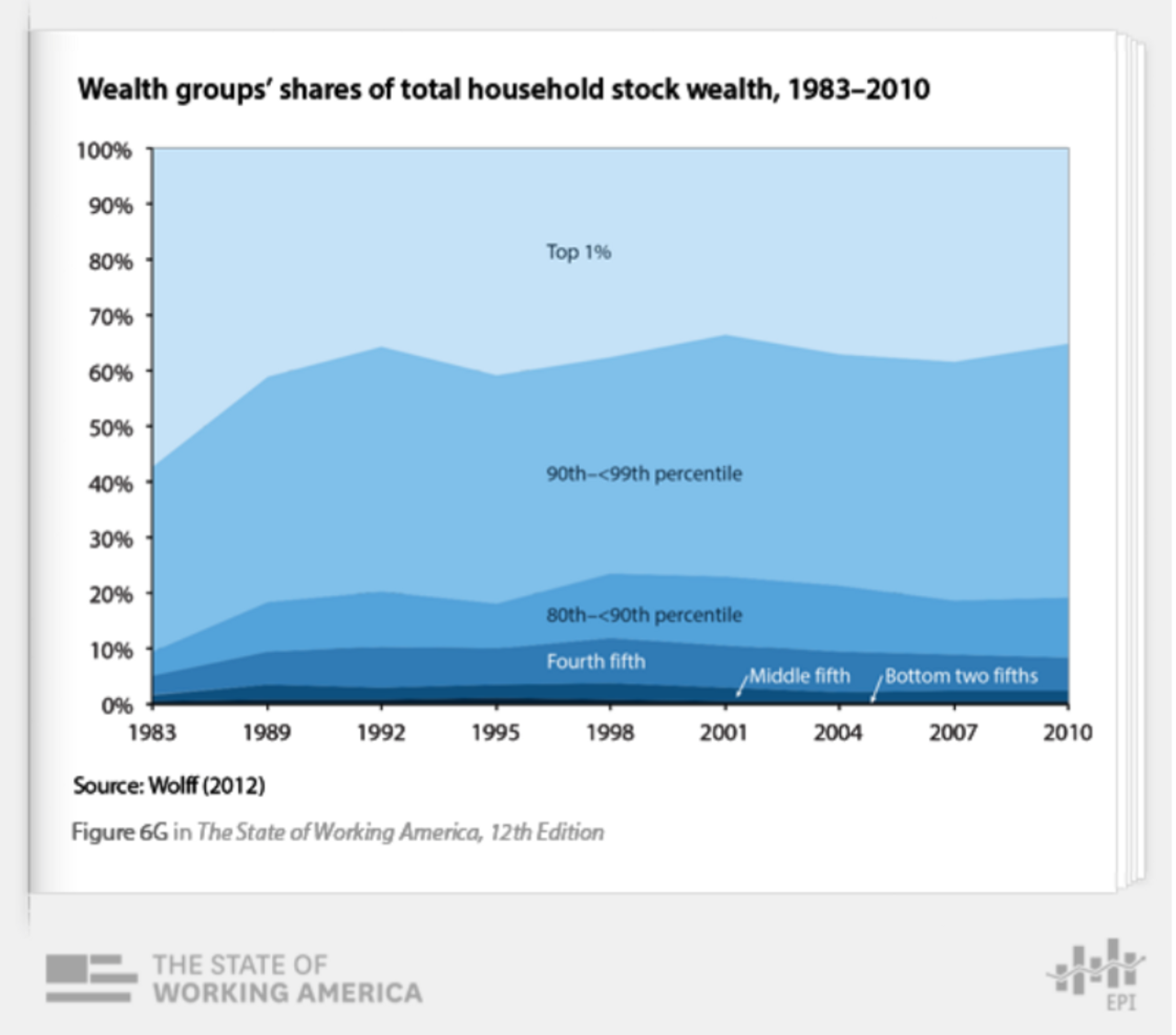

“In 2010, less than half (46.9 percent) of all households had stock holdings, and less than a third (31.1 percent) had stock holdings of $10,000 or more. The wealthiest 1 percent of households has never held less than one-third of all stock wealth. Since 1989, the top fifth of households consistently held about 90 percent of stock wealth, leaving approximately 10 percent for the bottom four-fifths of households.”

We’ve seen a continuation of this skewed stock-driven wealth redistribution since the financial crisis towards the top 10 percent. For example, of the 10 percent of families with the highest income, 92 percent owned stock as of 2013, which is slightly above the same levels as before the financial crisis. Meanwhile, for people in the bottom 50%, stock ownership decreased. Further exacerbating this gap is a divergence of how much dollar value in stock those groups own. As of 2013, the top 10 percent of Americans owned an average of $969,000 in stocks. For the bottom half of families, it was just under $54,000, or about 18 times less.

Moreover, this divergence in wealth is increasing. According to a recent study by the Congressional Budget Office (CBO), the wealth of families at the 90th percentile of the wealth distribution was 54 percent greater than the wealth at the 90th percentile in 1989 (adjusted for inflation). The wealth of families at the 25th percentile, however, was 6 percent less than the wealth at the 25th percentile in 1989.

Concurrently, the bottom 90% of households are reallocating a majority of household wealth to their homes. According to the Center for American Progress, homeownership as a percentage of household wealth has increased since the Financial Crisis. Moreover, total revolving credit- money that consumers can borrow and repay at their discretion, such as credit cards and lines of credit- has increased in value to re-approach pre-financial crisis levels. Furthermore, household wealth hasn’t increased substantially since the crisis.

Whether this imbalance is due to the general lack of financial education of the lower socioeconomic classes, a lack of access to one fact is certain: the barriers to entry posed to the common person are still far too high. Investing in traditional markets necessitates a broker and requires a cumbersome process that is not uniformly accessible to the average person. Instead, the gains earned from investing in the stock market are reserved for the few who are already well off.

This imbalance is particularly acute in the hedge fund space, where investing in the best performing funds are often impossible for the lower socioeconomic groups, as they are either “closed funds” (e.g. Citadel), or have ‘minimum investment’ requirements typically starting at $125,000 but can often be closer to $5–10 million. Obviously, these barriers prevent the vast majority of the population from capitalizing on this method of wealth accumulation.

Dawn of a New Investment Era: With the advent of a blockchain, we now have the ability to fully realize the democratization of markets

Marc Andreessen accurately describes blockchain technology as “a way for one Internet user to transfer a unique piece of digital property to another Internet user, such that the transfer is guaranteed to be safe and secure, everyone knows that the transfer has taken place, and nobody can challenge the legitimacy of the transfer.”

Introduced by the birth of Bitcoin (current market cap: $39.4 Bn) in 2009, blockchain technology provides a unique protocol that facilitates the secure, transparent transfer of value across the internet, and has given rise to an emerging asset class that has seen unprecedented growth over the last five years. With the ongoing growth and development of Ethereum (current market cap: $21 Bn), the rise of decentralized applications, the augmentation of the Initial Coin Offering (“ICO”), and the continued application of blockchain technology across industries, we will continue to see an upward trend in this space.

This emerging digital asset class does not necessitate a broker, and is completely accessible to anyone with a computer an internet connection. These assets are secured via a blockchain and smart-contracts, which don’t just “automate” processes, but also universally “enforce” and “regulate” them.

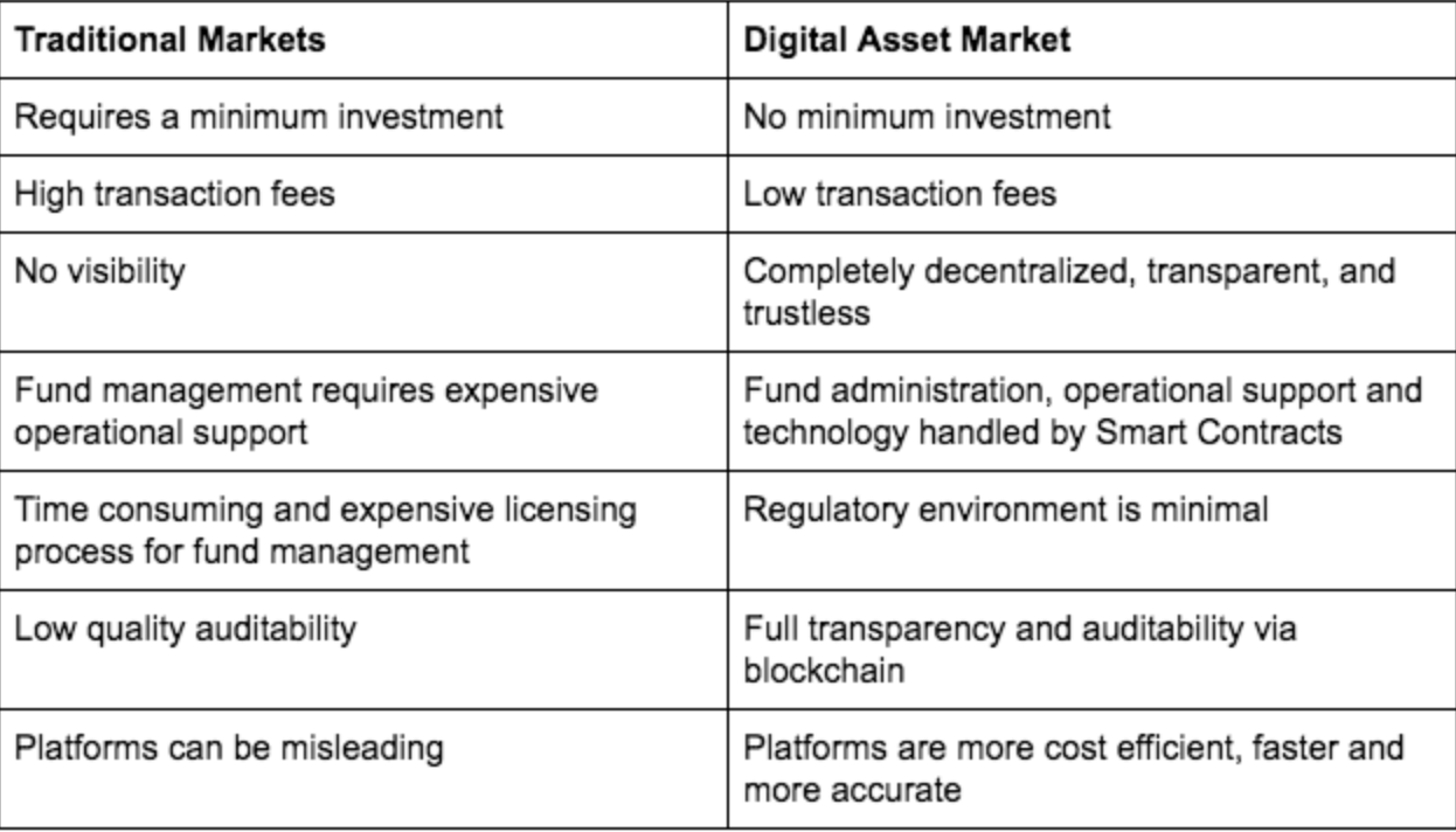

This asset class provides a myriad of benefits over traditional markets, covered in the table below.

Melonport leverages the strength of blockchain technology and democratizes investing for the common person

Melonport is the first application to enable open, competitive, and decentralized digital asset management solutions, as well as quick visibility and access to the performance of other asset managers. Built on Ethereum, Melonport facilitates distributed digital asset management by allowing anyone to set up, manage, and invest in [digital] assets via a customized portfolio. Fund performance is easily demonstrated and audited, and permits anyone to invest in other portfolios or open their invest to others.

Melonport Smart Contracts automate operations such as:

- Clearing and Settlement of transactions

- Performance Monitoring of investments and portfolio

- Broadcasting

- Validated Track Record

One parameter for analyzing the efficacy of digital assets is to assess the team behind the decentralized application that houses the asset. In this case, the strength of the Melonport team is particularly strong and is a good indicator of the eventual success of the Melonport token.

Melonport’s team is composed of two co-founders and several advisors.

Reto Trinkler is the developer behind Melonport and the CTO of Melonport. He studied mathematics from ETH Zurich–a prestigious technical university in Switzerland–and began developing Ethereum smart contracts in 2015. He helped develop software for blockchain consultancy Brainbot Technologies and developed a trading algorithm for sport betting.

Mona El Isa is the CEO of Melonport. She is a former star trader at Goldman Sachs, worked at Geneva-based macro fund Jabre Capital in 2011, and launched a hedge fund in Geneva before moving to the blockchain world.

Advisors include well-known blockchain developer Dr Gavin Wood, Swiss entrepreneur Dr. Andreas Glarner, and Hong Kong-based venture capital partner Jehan Chu.

Melonport raised $2.9 million in its token sale in February 2017. It hit its cap of 227,000 Ether in under 10 minutes, highlighting the popularity of the Ethereum protocol, ICOs, and the momentum Melon’s team has generated to date. Melonport tokens are now available for trading across leading exchanges, such as Kraken. Factoring in increased adoption and digital asset market growth, we believe the token is ripe for investment and should see a significant increase in value over the next 9 months. Furthermore, we view the Melon token as one of the select ICOs to merit a significant investment due to the product’s long-term use case and defensibility.

At a high level, the project is composed of two sets of smart-contracts; Melonport Core and Melonport Modules to tackle Protocol Tokens, such as Ethereum, and Traditional Asset Tokens, such as Decentralized Capital’s ERC20 Euro.

Melonport Core is the part of a portfolio (or fund) that provides Portfolio Managers with a tool to set up and interact with the functions that a Portfolio Manager may want to perform adhering to the specification of the Melonport protocol.

Melonport Modules correspond to all the functions that a Portfolio Manager might want to have available in their portfolio and are optional (e.g. price feeds, volatility calculations, NAV calculations, daily P&L calculations etc).

Melonport modules are conducive to outside development; independent developers can build modules openly on Melonport and earn tokens for their technical contributions per usage of their modules. This creates a great incentive model where value creators are rewarded for their contributions this increasing the value of the protocol both financially and in terms of (technical) user growth and eventual compounding network effects.

To be clear, our team is bullish on projects with developer-driven protocol developments in big markets. We’re also impressed by the current team, including new developer additions, Jenna Zenk and Simon Schmid.

In practice, the team’s go-to-market seems particularly sharp. By focusing on the exponentially growing digital asset space — currently at a $88Bn combined market cap, up from $1Bn in 2013 — Melonport can potentially create a monopoly in serving as the asset management software for digital assets while slowly moving into more traditional markets.

Moreover, we like that Melonport lowers much of the encumbrances of the wealth management software in the market today, which should allow anyone to be able to manage an investment fund based on investing talent and skill instead of access to resources. It is our belief that this lower friction will lead to lower costs for wealth preservation and growth, and these savings will be passed onto the bottom 50% of the population which has been ignored and left behind by the current solutions.

Note: This content is provided for informational purposes only and it is not intended to be, and does not, constitute financial advice or any other advice.

Image source: Wikimedia Commons

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Your update on what’s going on in the Fintech space. Keep up-to-date with news, valuations, mergers, funding, and events. Sign up today!