Paycheck to paycheck is a stressful way to live. Many Americans claim they have too much “month at the end of their paychecks,”and unfortunately, they’re not alone. According to a CareerBuilder survey, almost 80% of Americans live paycheck to paycheck.

Luckily, banks offer overdraft protection to bridge the gap between bills due on Thursday and Friday payday.

When banks charge customers a small fee to cover account overdraws, it’s called overdraft protection. Though it’s not ideal to “bank” on using overdraft protection to cover your expenditures, it’s often better than letting bills go unpaid or dealing with late fees or bounced checks.

At most banks, you can opt to use overdraft protection. It’s also possible to use a backup credit card or a savings account and link it to your checking account just in case your spending exceeds your income.

Don't bank on it

Most financial institutions charge $35-40 per overdraft item. In the past, banks reordered debits and credits and charged more overdraft fees, unleashing even more financial burden on their sometimes already-strained customers.

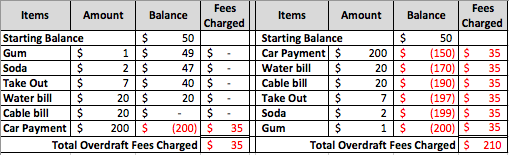

Here’s an example: Paul has $50 in his checking account. He buys a pack of gum for $1. Later, he purchases lunch for $7. He buys a soda on the way home. Simultaneously, his cable bill and water bill (both $20) are due and his car payment of $200 is auto-paid from his checking account. The bank could use the order of transactions to charge Paul more. See the chart below for an illustration:

When you’re living paycheck to paycheck, the extra $175 in overdraft fees can be stressful, and these past overdraft practices ultimately created an outpouring of complaints from bank customers. According to a report by the Consumer Financial Protection Bureau, financial institutions were earning over $15 billion in overdraft or non-sufficient fund fees in 2016.

Lawsuits were filed against banks over these types of overdraft charges, and banks were forced to issue refunds for their mishandling of overdraft fees. Most banks settled and issued refunds for any transactions that could have been resequenced to incur fewer fees.

Nowadays, if you start the day with an overdraft, as long as you deposit funds before the end of the day, your overdraft fees should disappear.

An alternative you'll want to avoid

Compared to payday loans, the overdraft protection program looks like an awesome deal. Payday loans, which are small, short term unsecured loans, are one really expensive way to bridge the gap between paychecks. Payday loans charge anywhere from 36% to 39% in interest charges. If you need $100 to get you to the next payday, do whatever you can to avoid a payday loan. Overdrafting your account is a much cheaper alternative.

Small business overdraft protection

If you’re a small business owner, it’s imperative that you have small business overdraft protection. After all, it’s inevitable: A huge supply bill may come through at the same time payroll is due. Instead of scrambling for extra funds, your bank will cover you with its overdraft protection program.

Most banks have automation for moving funds around when needed. You can apply for a credit card as well, which will be linked to your checking account. If your checking account is overdrawn, it will draw funds from the credit card. Some overdraft protection programs will charge a low fee ($10 or 3% of the transaction).

Personal checking overdraft protection

Personal checking accounts also offer opt-in overdraft protection. If you see a pattern of $35 overdraft fees each month, you may want to consider overdraft protection. You can open a savings account linked to your checking account as another source to withdraw funds.

If there’s typically nothing in your savings account, however, there’s a solution: Link a low line of credit to your checking account. Typically, the fee to transfer funds to cover a deficit in your account is only $10 instead of $35.

Final thoughts

If you discover that your spending habits, bill cycles, and paydays do not align, consider having a conversation with your credit card company, car loan credit union or other creditors. You may be able to shift your due dates move your due date to a few days later to avoid late fees or overdraft fees altogether.

Hire a Pro: Compare Financial Advisors In Your Area

Finding the right financial advisor that fits your needs doesn't have to be hard. SmartAsset's free tool matches you with fiduciary financial advisors in your area in 5 minutes. Each advisor has been vetted by SmartAsset and is legally bound to act in your best interests. If you're ready to be matched with local advisors that will help you achieve your financial goals, get started now.