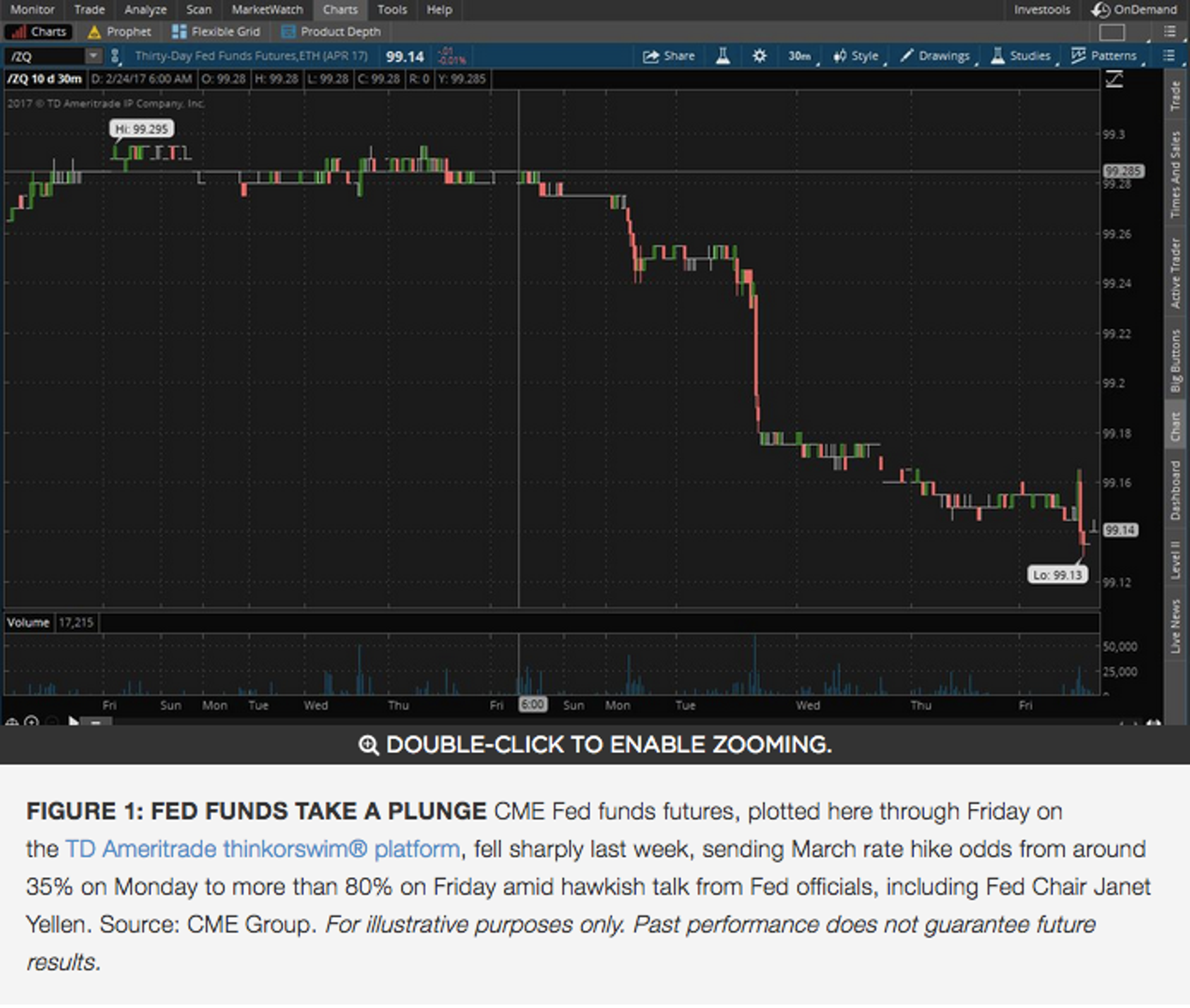

At one point last month, the futures market projected chances of a March rate hike at 8%. By early Monday, that estimate was above 80%.

It appears the Fed, led by Chair Janet Yellen, has set the table for a possible rate hike when it meets March 14-15, and all that may be left to do is pour the water and serve the appetizers. As Monday morning and a new week dawned, focus remained on the Fed, and on some geopolitical concerns. The futures market pointed toward a lower open, based in part on North Korea’s test of several missiles over the weekend.

Yellen said Friday, “At our meeting later this month, the Federal Open Market Committee will evaluate whether employment and inflation are continuing to evolve in line with our expectations, in which case a further adjustment of the Federal funds rate would likely be appropriate.”

That may sound nuanced, but in “Fed-speak,” it’s a pretty blunt sign that the Fed wants investors to get ready for a possible hike. And Yellen’s speech followed hawkish remarks by a number of Fed officials, including some who have dovish reputations on Wall Street.

Perhaps only one thing stands between now and a March 15 rate hike: This Friday’s non-farm payrolls report for February. If you’ll recall, it seemed like the Fed was heading for a rate hike going into its June meeting last year, only to pull back at the last minute after a woeful May jobs report. There’s no indication yet of what Friday’s report might bring, and job growth has been pretty strong in recent months. Even if February jobs came in weak, it’s highly unlikely a jobs report would derail a rate hike, barring an outright disaster.

Perhaps more interesting than Yellen’s signal to prepare for a possible hike was her observation that the economy has basically reached the Fed’s objectives, making it more appropriate to adopt a “neutral” policy after more than eight years of monetary stimulus characterized by low rates and quantitative easing. “The economy has essentially met the employment portion of our mandate and inflation is moving closer to our 2 percent objective,” Yellen said

Look that over for a minute. It could mean that the long-term environment many market participants are so familiar with has changed. Younger investors who were in college back in 2008 and are approaching age 30 now may not even remember a time when the Fed wasn’t trying to stimulate the economy. This long-term stimulus corresponded with the massive rally that started in March 2009 and hasn’t stopped yet. The question is whether the stock market can continue this sort of performance if rates go back to a more neutral level.

Now even Yellen admitted she doesn’t know exactly what a neutral rate would be, only describing it as “one where monetary policy neither has its foot on the brake nor is pressing down on the accelerator.” The neutral rate may now be on the low side historically, Yellen said, but she expects it to rise in coming years back to its “longer-run” level to keep the economy from overheating. A decade ago, rates were in the 5% range. That doesn’t mean they’ll necessarily head all the way back to that level, but Yellen did add that “the process of scaling back accommodation likely will not be as slow as it was during the past couple of years.”

The Fed raised rates in December 2015 and again in December 2016.

For this week, the focus is on Friday’s jobs report and whether that gives the Fed the last push it needs to decide on a hike. Economists expect 190,000 jobs and an unchanged unemployment rate of 4.7 percent, according to Thomson Reuters. They expect average hourly earnings to rise 0.3 percent. The 190,000 level would be in line with or a little above many recent jobs reports, but below the big gains seen in January.

Stocks remain near all-time highs, so it’s important not to do any “all in” or “all out” type of trades. There’s some concern that when details on the President’s tax plan hit, it might be difficult for the market to sustain its current remarkable pace upward.

From a data perspective, factory orders are due at 10 a.m. ET. And later today, the monthly Investor Movement Index, or the IMXSM, from TD Ameritrade, is scheduled. The IMX is a tool that shows what hundreds of thousands of retail investors were doing in February across all markets.

Beyond Roads and Bridges

Possible tax cuts under the new administration may be among the key factors supporting the market. But don’t forget another one: President Trump’s continued support for more infrastructure spending. And when we think about infrastructure, it’s important to remember that infrastructure doesn’t just mean roads and bridges. It could mean technology infrastructure, which sometimes gets overlooked. If Trump can engineer a repatriation plan that allows some of the big tech companies to bring money back to the U.S. from overseas, that conceivably could inject renewed vigor and muscle into U.S. technology infrastructure. Investment in technology infrastructure often has payoffs for the stock market, most notably the Internet boom of the 1990s.

More Retail Woes

Another retailer missed earnings expectations late last week. This time it was Costco Wholesale Corporation COST, which posted revenue and earnings per share that both were below Wall Street analysts’ consensus. Same-store sales growth also missed expectations, and COST said it would raise the price of membership. Earlier last week, Target Corporation TGT and Best Buy Co Inc BBY missed earnings expectations. But the retail weakness isn’t universal; Lowe's Companies, Inc. LOW, which also reported earlier this week, came in better than expected. With most earnings now out of the way, it could be interesting to check back next quarter to see how retailers did, as Internet sales continue to be a struggle for some.

Strong Q4 Earnings Season Wrapping Up

Almost all major companies are now done reporting Q4 earnings, and the quarter lived up to expectations and then some. It now appears that companies in the S&P 500 delivered Q4 earnings growth of nearly 6%, compared to predictions before earnings season of just over 4%, research firm CFRA reported. CFRA expects strong earnings growth to continue, ultimately coming in at 10.7% for the full year of 2017. Looking back at Q4, eight sectors appear likely to post earnings gains, CFRA said. The only exceptions are energy, industrials, and telecom. The firm expects double-digit 2017 earnings growth from financials, materials and info tech, with all sectors except utilities seen up for the year from an earnings perspective.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.