Another afternoon; another earnings report from a big tech company. On Wednesday, it was Facebook FB rather than Apple AAPL, but once again, the results looked pretty good. Nevertheless, the stock market appeared likely to open lower Thursday.

FB beat analysts’ estimates on both the top and bottom lines. Advertising revenue rose more than 50% during the quarter, and the social media giant continued adding users. Like AAPL the day before, FB saw its shares jump 3% in pre-market trading. AAPL shares ended up climbing more than 6% yesterday, so it could be interesting to see if FB gains any further momentum as today’s session advances.

One other thing to consider as we leave AAPL earnings behind for another quarter: AAPL sells some very expensive products, and it saw sales of those products beat Wall Street’s estimates for a quarter that included the holiday season. Some stocks, AAPL among them, can serve as decent proxies for consumer sentiment, and AAPL’s results do seem to indicate a relatively healthy consumer. We’ll get another indicator after today’s close when Amazon AMZN puts out its earnings, and the Feb. 15 retail sales report could transmit an even broader sense of consumer sentiment.

As we noted in yesterday afternoon’s update, the Fed leaving rates unchanged was no surprise. But the Fed’s statement did contain some interesting nuggets, including observations that inflation will rise to 2% “over the medium term,” economic activity will expand “at a moderate pace” and labor market conditions “will strengthen somewhat further.” While all this appears positive, it didn’t sound particularly hawkish or seem to indicate the Fed feels any need to speed up the rate hike process.

In fact, expectations fell after the meeting for any near-term rate hike, with Fed funds futures pricing in a 13% chance of a rate hike next month, and about a 35% chance in May. As was the case before this week’s meeting, June appears to be the most likely month for the next rate move, but there’s a lot of time between now and then, so it’s definitely not set in stone.

Looking at the present economy, the Fed said, “Measures of consumer and business sentiment have improved of late.” So there you have it.

With the Fed meeting out of the way and a bit of a decline in the turbulence coming out of Washington, at least from a business standpoint, volatility pulled back at midweek. VIX fell back below 12 by late Wednesday. What stood out about VIX, however, was what some called a “flash crash” reminiscent of what happened to the Dow Jones Industrial Average ($DJI) back in May 2010. VIX briefly fell below 10 on Wednesday afternoon before quickly bouncing back. By Thursday morning, it had climbed back above 12.

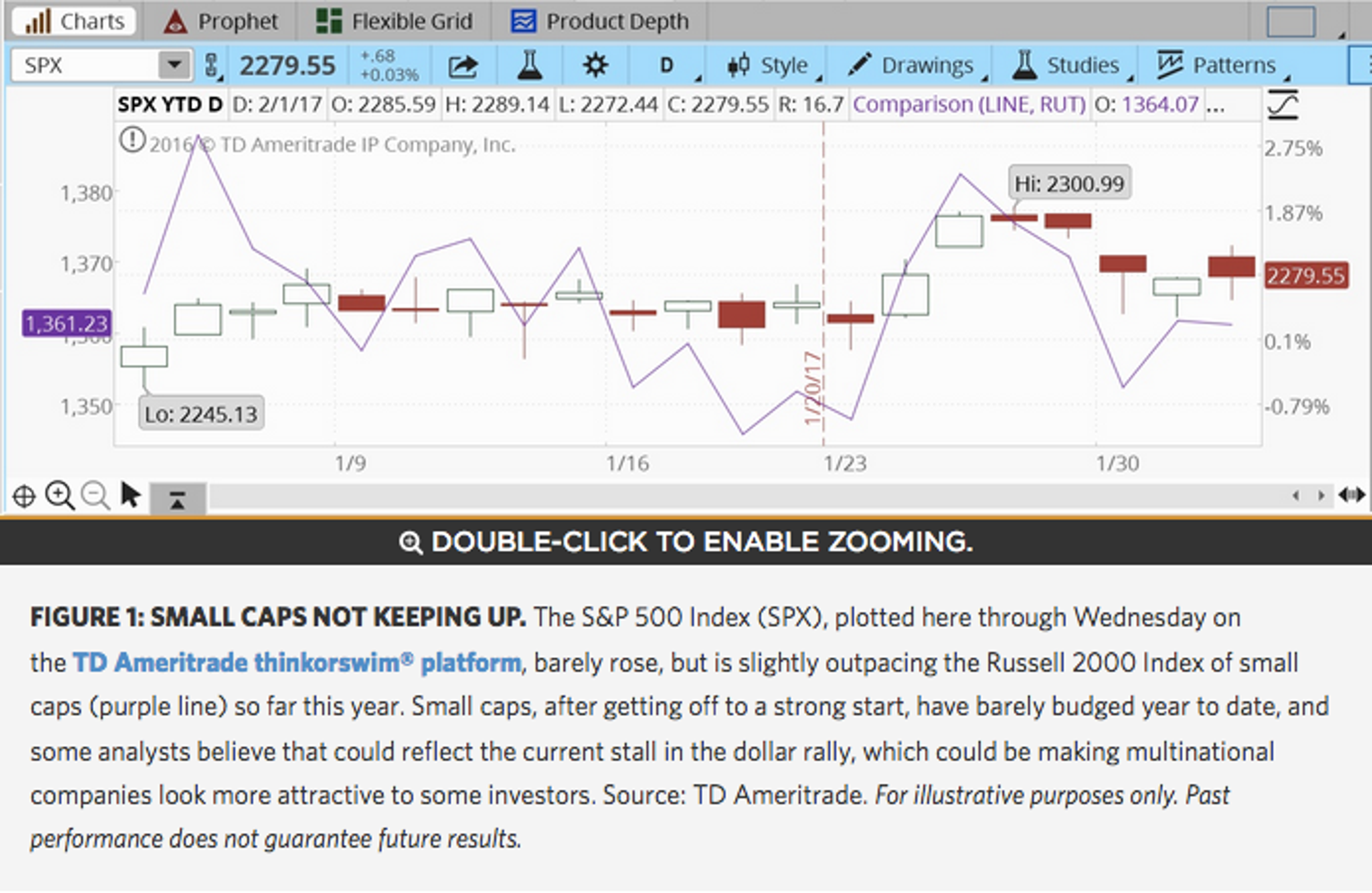

The S&P 500 Index (SPX) broke its four-day losing streak Wednesday, but just barely. Healthcare led advances, while utilities and real estate fell to losses. Utilities are considered a safety sector, and seeing utilities decline while materials and info tech advanced could mean investors getting a bit more aggressive here late in the week, but we’ll see if that continues.

On the economic data front, there were mixed indications Wednesday, with ISM Manufacturing beating expectations but construction spending and auto and truck sales a little on the disappointing side. Today looks like pretty quiet on the data watch, but everyone is gearing up for Friday’s Non-farm Payrolls report (see below). Jobless claims Thursday came in at 246,000, which was near expectations.

The dollar has been waffling around lately, with the U.S. Dollar Index holding slightly below 100, down from highs of around 103 in early January. The strong dollar might have helped small-cap stocks during the post-election rally, as a sector rotation out of multinationals and into stocks with less overseas exposure may have appeared to be a solid bet at the time. Now, with the dollar rally stalling a bit, small caps are lagging the SPX (see chart and caption below).

It All Leads Up to Jobs

All the data this week just leads up to one big report: Tomorrow’s monthly Non-farm Payrolls for January. The consensus of Wall Street analysts is for the report to show January job growth of 170,000, said Briefing.com, up slightly from December. But remember, in December analysts had expected 175,000 jobs but only got 156,000, and at the same time the government made a hefty revision to November’s report, raising job growth that month to 204,000 from the previous 178,000. It’s always helpful to keep an eye on revisions, so remember to check if the government makes any changes to that relatively tepid December number in tomorrow’s report. Private sector job growth in January rose a torrid 246,000, according to ADP, but the government’s report is broader and takes the public sector into account as well. Remember to closely watch where the new jobs are coming from. Although we all have probably waited a table, washed a dish, or served a drink at some time, the restaurant and bar industry is not the area we want to see as the leading area of job creation. We would like to see gains in sectors like manufacturing, construction, financial, and business.

But It’s Not All About Jobs

Wages arguably represent the other key factor in Friday’s jobs report. In December, wages rose 0.4%, and hourly earnings were up 2.9% year-over-year. When job growth slows and wage growth rises, as we saw in December, it can sometimes mean the labor market is tightening, which can have inflation ramifications. When inflation flares, the Fed fire truck often pays a call. Let’s see if tomorrow’s report adds any fuel to the inflation story. Consensus is for a 0.3% hourly earnings rise in December, Briefing.com said.

Meeting Over But Fed Not Done For the Month

The next big Fed event comes Feb. 15 when Fed Chair Janet Yellen is scheduled to appear on Capitol Hill for her semiannual monetary policy testimony to the House Financial Services Committee. Later that same week, she speaks to the Senate Banking Committee. This appearance at the Capitol is sometimes called the “Humphrey-Hawkins” testimony, and market participants tend to follow it closely. So stay tuned. And now that the February FOMC meeting is out of the way, Fed speakers can once again prowl the country, speaking their minds about the economy. We always miss them so much on those days when they’re muzzled leading up to meetings. Welcome back!

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.