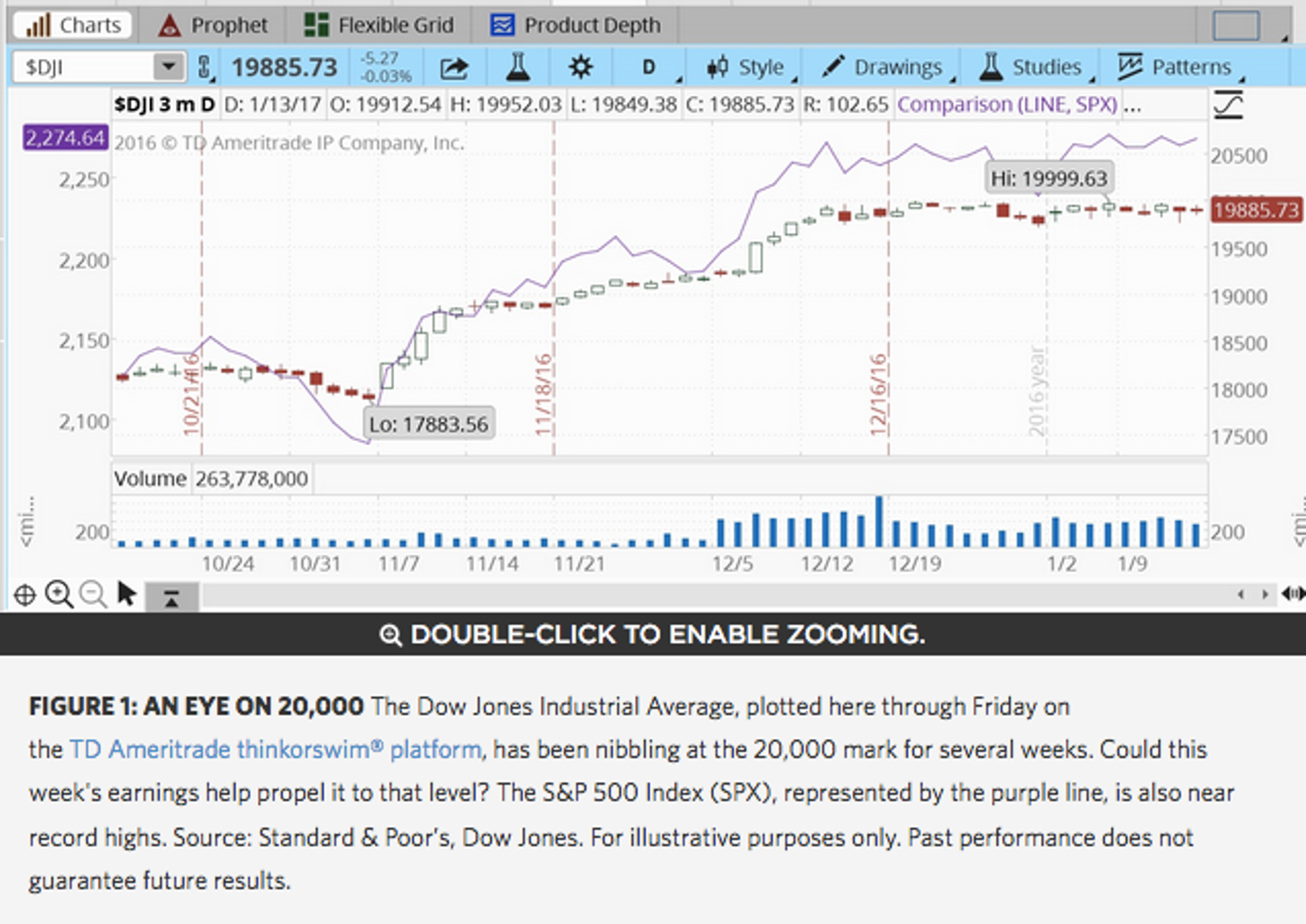

This week, the rubber hits the road as more big banks report and other industries also begin to enter the earnings picture. But stocks looked likely to open lower Tuesday, hurt in part by Brexit concerns.

British Prime Minister Theresa May appeared to put the United Kingdom on path toward a sharp break from the European Union, saying this morning, “What I am proposing cannot mean remaining in the single market,” The New York Times reported. Stock futures tumbled after her remarks. The dollar came under pressure too, apparently hurt by President-elect Trump’s comments over the weekend that the dollar was too strong. All this early excitement helped inject volatility into the market, with VIX rising 10% to 12.36.

On the earnings watch, Morgan Stanley MS appeared to hit the ball out of the park, reporting an 83% jump in quarterly earnings due in part to a year-end surge in trading revenue associated with the post-election rally. Bond trading revenue looked especially strong. Quarterly profit increased to 81 cents a share, up from 39 cents in the same quarter a year earlier and above Wall Street analysts’ consensus of 65 cents a share. Sales increased 17% to $9.02 billion.

That followed generally strong results last Friday from major financial names, particularly JPMorgan Chase & Co. JPM and Bank of America Corp BAC. On a side note, MS announced cuts Friday in its investment banking units, so it could be interesting to see how that plays out over the longer haul, as investment banking places high in the business models of both MS and Goldman Sachs (GS).

Tomorrow brings two more financial behemoths in GS and Citigroup Inc C, and then most of the big financial names are out of the way until next quarter. Once again, it may be wise for investors to look beyond the quarterly numbers and listen to what bank CEOs have to say about the economic outlook. With a new presidential administration taking office, it may be more important than ever to get a sense of what key executives think.

Another major report is from managed health care company UnitedHealth Group Inc UNH, which released earnings before the open today and beat Wall Street’s estimates on both top- and bottom-lines. Health sector investors may want to listen for signals from UNH about the possible effects of the new administration and Congress, particularly what the company thinks of the possible repeal of the Affordable Care Act (ACA). UNH executives may also pinpoint trends in general medical spending.

Wednesday morning brings the December consumer price index (CPI), after producer price index (PPI) data that came in pretty much as expected last Friday. Analysts on Wall Street expect a 0.3% rise in overall CPI, but just a 0.2% increase in the core number, according to Briefing.com. The November readings were 0.2% for both. There’s no major data on the calendar today.

Beyond Banks

The earnings season hit full stride last Friday when three big banks reported, and more major financial sector names are on the calendar this week. But now we start seeing some other industries come into the picture, with Netflix, Inc. NFLX reporting on Wednesday, International Business Machines Corp. IBM on Thursday, and General Electric Company GE on Friday. NFLX is the first of the so-called “FANG” stocks to report, and the other members of this fraternity are Amazon.com, Inc. AMZN, Facebook Inc FB and Alphabet Inc GOOG. Some of these big names came under pressure after the election, but have shown more strength lately. NFLX says it’s now available in 190 countries, and grew its domestic subscribership in Q3. But some analysts point to increasing competition. The company’s Q3 earnings report was better than expected, so we’ll see tomorrow how NFLX follows that up.

Singing the Biotech Blues

The Nasdaq Biotechnology Index, which crumbled at one point last week after remarks on drug pricing from President-elect Trump, managed to recover some losses by Friday. Still, there remains a lot of concern about how biotech might perform, as the industry has been under fire from both parties during the last year. Market performance reflects those concerns, with the index up a little more than 3% over the last three months, compared with a nearly 7% gain during that time period for the Nasdaq as a whole. Some of the biggest biotech stocks are flat or lower since the election.

Consumer Sentiment In Line

Initial January consumer sentiment slipped a touch to 98.1, the University of Michigan said Friday, down from 98.2 in December and a little under Wall Street analysts’ expectations. Still, sentiment remains at its highest level in more than a decade.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.