A holiday mood seems to be settling into the markets, with low volatility and another flat open Wednesday amid little news of note. That said, stock indices remain near recent record highs as the post-election rally rolls on.

In yesterday's action, strength into the close helped drive the Dow Jones Industrial Average (DJIA) to yet another record, and the S&P 500 (SPX) also rose on strength from the financials and telecoms. Keep watching the 2219 area for signs of technical resistance in the SPX.

Asian stocks continued to climb earlier Wednesday, but there was a bit of a stumble in Europe as UK manufacturing data badly missed expectations. An expected 0.2% rise instead came in as a decline of 0.9%. This led to a sell-off in the pound of more than 0.6%. The dollar index has slipped a little over the last few days, but remains near recent highs.

Early in the day marked the release of data showing mortgage applications falling 0.7% from last week, and 10 a.m. ET brings the scheduled release of the JOLTS job opening numbers (see below). The other interesting note today will be the CEOs of AT&T Inc. T and Time Warner Inc TWX appearing on Capitol Hill to discuss their proposed deal in front of a congressional committee.

Although we’re done with the election, President-elect Trump has continued to use Twitter as a way to communicate with the rest of the world. He has, in an unconventional move, taken the last few days to comment on some individual stocks such as Boeing Co BA and United Technologies Corporation UTX. The odd thing is, the market has brushed off any negative backlash, as these stocks stayed stable despite this spotlight. The broader market also rallied. Judging by other indicators such as VIX, the market seems to be forgiving and in a honeymoon period with what may come as the new administration prepares to take office.

Speaking of the VIX, that popular measure of S&P 500 Index (SPX) volatility fell back toward its August lows below $11.70 early Wednesday. We’re going into the last weeks of the year, traditionally a quieter time in the markets, and the low VIX would seem to indicate that investors don’t expect sharp price movements in the days and weeks ahead. But a couple events, including Thursday’s European Central Bank (ECB) meeting (see below) and next week’s Fed meeting, could interrupt any holiday siesta, perhaps causing volatility to climb a little.

Crude oil fell back toward $50 a barrel early in the day. Last month’s OPEC production agreement is supposed to take effect in January, but in the meantime, OPEC members and Russia continue pumping oil in a major way, keeping world markets well supplied. On the other hand, U.S. stockpiles fell 2.2 million barrels last week, the American Petroleum Institute (API) said late Tuesday, a bit more of a drop than expected. The official government data are due later today. The energy sector was among the worst performers in equities Tuesday.

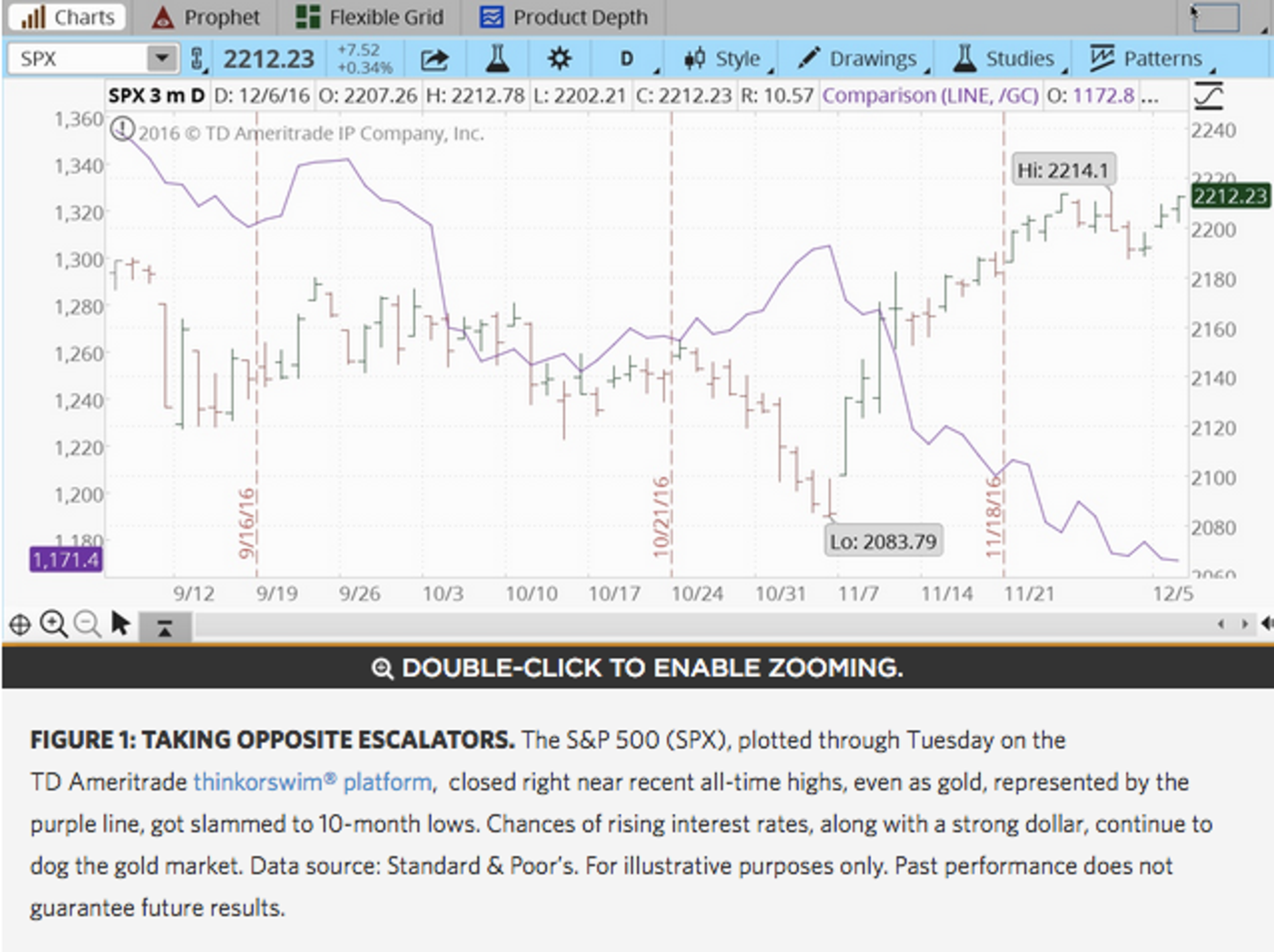

Gold Takes a Panning

As stocks continued to trade near all-time highs early this week, gold skidded to its lowest level since February. Gold is an investment people often turn to during uncertain times. But considering the performance of stocks and bonds over the last month, it appears investors remain confident in the markets. Additionally, if the Fed raises rates as expected next week, that could put more strength into the dollar, perhaps bringing additional pressure to bear on gold. The combination of higher rates and a stronger greenback are enemies of the metal, though gold remains well above the year-ago lows of under $1,100 an ounce. Gold’s recent decline isn’t just hurting the metal itself. Gold-mining stocks are also taking it on the chin.

Get Ready for ECB Meeting

Though last weekend’s Italian referendum is out of the way, Europe could be back in focus tomorrow as the European Central Bank's (ECB) Governing Council meets. At that time, we might get further insight into the ECB’s plans for its 80 billion-euro-a-month asset purchase program. The question is how much longer the plan might last, with some analysts predicting a six-month extension, according to Briefing.com. The failed Italian referendum last weekend could increase the odds of such an extension, some analysts told the media this week.

Job Openings Data Ahead

Later this morning comes the JOLTS jobs openings report for October. Last month, the report showed layoffs at record low levels during September, with job openings that month at 5.486 million. The report is a bit time lagging, showing activity that’s now two months old. Weekly unemployment claims have been trending near 43-year lows recently, and the U.S. economy created 178,000 jobs in November. Other economic indicators continue to show strength, with factory orders rising 2.7% in October, up significantly after just a 0.3% rise the previous month. However, the monthly factory orders data mask an overall sluggish long-term performance, with orders down 2% on a year-over-year basis, Briefing.com noted.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.