The incredible stock market run to all-time highs continues, fueled in part by rising oil prices. Monday marked the first time since December 1999 that all four major stock indices closed at record levels, and stocks looked set to extend their rally early Tuesday.

Can the current strength develop into a so-called “Santa Claus” rally as the winter holidays approach? We’ll have to wait and see. But in the near term, it wouldn’t be surprising to see pressure creep in later today as people start winding things down ahead of Thursday’s Thanksgiving holiday. That’s pretty typical in a holiday week, and volume wasn’t heavy yesterday. Pressure may not come until the end of the day, but it’s still worth watching.

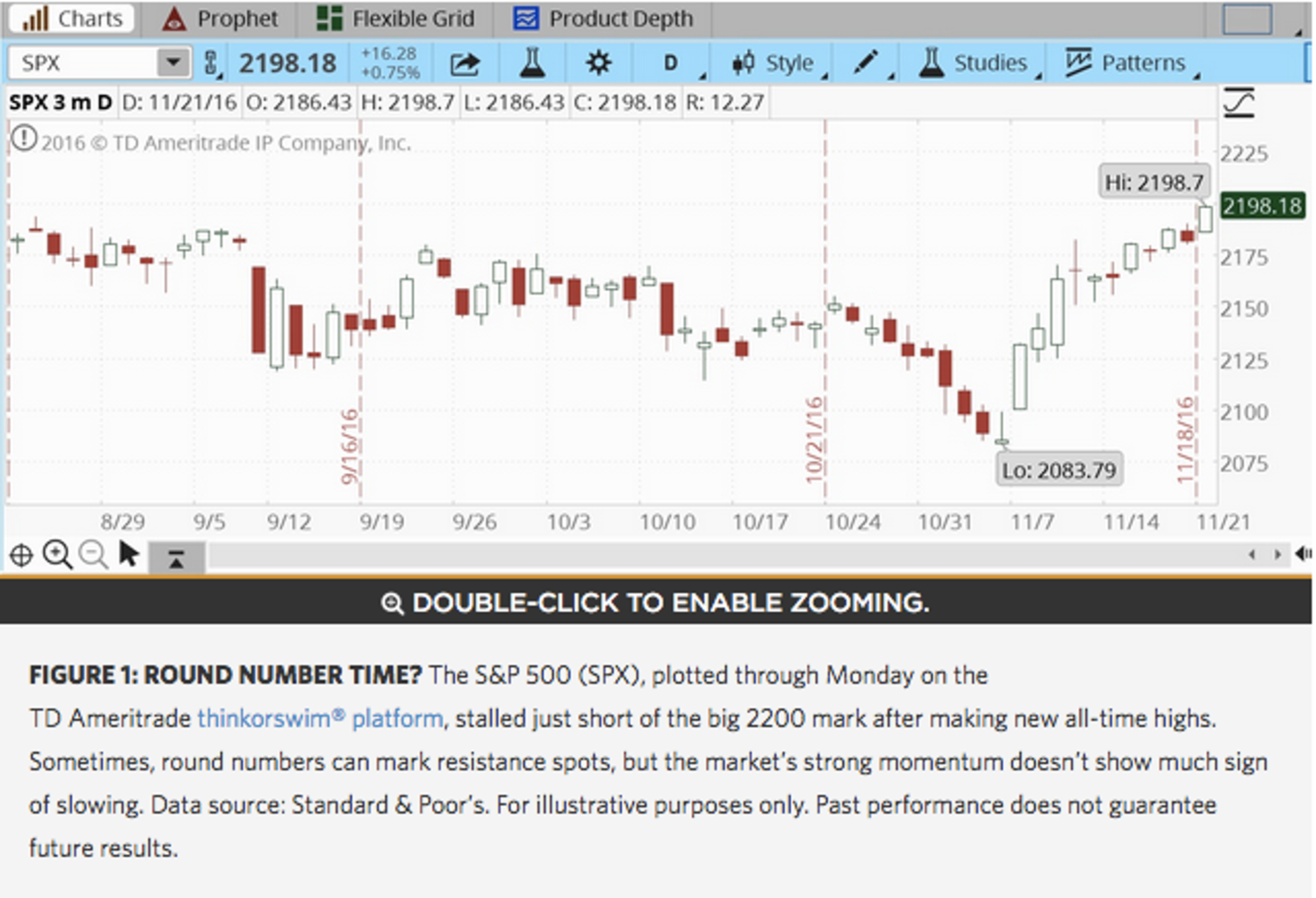

From a technical standpoint, tracking resistance can be a bit foggy at record levels, but keep an eye on the 2219 mark for the S&P 500 Index (SPX), as that may represent a resistance area.

Oil was a major component of Monday’s drive to record highs, but crude oil prices leveled off a bit early Tuesday. There’s starting to be a common thought that OPEC could cut production when it meets next week, so keep an eye on the $50 a barrel level, which has represented a psychological resistance point for nearby U.S. crude futures. Meanwhile, the energy sector of the stock market keeps galloping higher, posting 2% gains on Monday.

VIX futures, which measure volatility, fell below $13 for the S&P 500 index (SPX) early Tuesday, the lowest level in nearly a month. Meanwhile, oil volatility, as measured by the CBOE’s OVX, fell from the seven-month highs it posted last week.

Utilities and info tech, both under pressure since the election, are enjoying a slight rebound. The recent strong rally in the dollar had weighed on info tech, an export-focused industry, but the dollar retreated a bit Monday. Rising bond yields had utilities on the defensive, but are down a little early Tuesday. Monday’s rally in the two sectors doesn’t mean the pressure just goes away, but it may indicate some buying interest for both.

Real estate stocks, however, fell again Monday, as rising mortgage rates take their toll. October existing home sales data are due later this morning, and consensus among Wall Street analysts is for a seasonally-adjusted annual rate of 5.4 million, down slightly from 5.47 million in September. Last month showed first-time buyers as an important driver of sales activity, representing 34% of sales, the highest level since July 2012. Keep an eye on that indicator in today’s report, because, as Briefing.com notes, increased participation from first-time buyers is a hopeful sign for the home-selling market. Note, however, that the October data won’t reflect the kind of mortgage rates we’re seeing now.

Earnings season may be over, but that doesn’t mean a break from earnings. Some of the big firms reporting today include Medtronic PLC MDT, HP Inc HPQ and Campbell Soup Company CPB.

Small-Cap Stall?

Since the election, small-cap stocks have soared, boosted by hopes of less government regulation, less chance of a minimum wage increase, and a possible increase in infrastructure spending, among other factors, according to S&P Global. The S&P SmallCap 600 surged nearly 11% between Nov. 8 and Nov. 18, compared to just a 2% rise for the S&P 500 during that time span. However, S&P Global doesn’t think this dramatic rally can continue at the same rate in the near term, and a breather may be coming. Prices “have gotten ahead of themselves,” S&P Global wrote, but the firm remains bullish looking farther out, noting that the S&P SmallCap 600 could see earnings per share growth of nearly 19% in 2017, vs. around 12% for S&P 500 stocks.

Hitting the High Notes:

Monday’s ascent to new all-time highs marked the first record high for the S&P 500 Index (SPX) since mid-August. That’s an accelerated pace compared to the more than a year the SPX took to break its spring 2015 high. What the SPX didn’t do Monday was penetrate the psychological barrier of 2200, though it seemed fairly likely to do so at Tuesday’s open. As an aside, 2200 is the level that one major investment-banking firm predicted the SPX would reach… at the end of 2017! Is the market getting ahead of itself, or will some analysts be forced to go back to their drawing boards? We’ll see.

Still Waiting for that Treasury Rally:

Despite the sharp tumble Treasuries took over the last two weeks, the low prices aren’t drawing much buyer interest, Briefing.com notes, adding that the Monday’s $26 billion 2-year Treasury auction was met with mediocre demand, helping flatten the yield curve somewhat.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.