By Shira Gonen

Analysts provided earnings previews for stock giants Apple Inc. AAPL and Nokia Corp (ADR) NOK with cautious outlooks going forward. While one analyst believes Apple is losing its long-term growth trajectory due to various near-term challenges, the other updates his estimates on Nokia due to weaker than expected growth regarding the Alcatel-Lucent Merger.

Nokia Corp (ADR)

Analyst Michael Genovese of MKM Partners expressed his views on Nokia prior to Q1:16 its earnings release in a few weeks. Specifically, the analyst comments on how he believes the January Alcatel-Lucent merger will affect earnings, and updates his estimates accordingly.

The analyst raises his 2016 and 2017 EBIT estimates to €1.96 billion and €2.4 billion, respectively, higher than his previous estimates of €1.55bn and €1.63 billion, respectively. Despite this increase, he decreases his operating margin forecast for 2016/2017 and predicts "mixed" EPS results believing the company will post 2016 EPS of €0.28, compared to prior estimates of €0.32, and 2017 EPS of €0.35, compared to previous estimates of €0.31.

The analyst also provides an updated sales forecast post-merger of €23.33 billion due to "meaningful revenue dis-synergies" resulting from the merger. Genovese notes this figure is 12% lower than previous forecasts for both companies' combined. The analyst cites various reasons for his "cautious top line view." First, the analyst fears overlap in both companies' Wireless access products, which he notes constitute 40% of the newly combined companies. Second, he cites "weak global demand for wireless access products" and points to industry trends of a middle point between 4G and 5G radio cycles. Third, the analyst cites "weak competitive and secular trends" in Alcatel's Wireline products, which he believes competitors will take advantage of as the two companies integrate.

In order for Genovese to have a more optimistic outlook, the company would need to show "more substantial cost and expense synergies…and/or more aggressive cash return," citing over 10 billion Euros in net cash on the balance sheet.

The analyst maintains his Neutral rating on the company with a $6.75 price target. He states, "We still view the Alcatel deal as only moderately accretive to the company's bottom line."

According to TipRanks, Michael Genovese has a 43% success rate recommending stocks with an average return of 3.3% per recommendation. Out of all the analysts who have rated NOK in the past 3 months, 64% gave a Buy rating, 9% gave a Sell rating, and 27% remain on the sidelines. The average 12-month price target for the stock is $8.23, marking a 34% upside from where shares last closed.

Apple Inc.

Deutsche Bank analyst Sherri Schribner weighed in on Apple prior to its Q2:16 earnings release at some point. Although the analyst believes investors will purchase the stock near-term due to "anticipation trade" related to the launch of the iPhone 7, she provides a cautious view and believes Apple is losing its growth momentum. She states, "We remain focused on the long-term fundamentals for Apple, which suggest top-line growth will be more challenging going forward."

The analyst cites several reasons why she believes the company may be in hot water longer-term. First, the analyst notes a saturation of the smart-phone market in developing countries, resulting in slower sales. As a result, "refresh cycles are elongating", forcing the company to focus more on developing markets. A major hurdle Apple faces in developing markets, according to the analyst, is price. The analyst notes a steep difference in disposable income, particularly in China and India, than that of U.S. and European consumers, resulting in significantly lower priced smart phones. She explains, "We expect this price sensitivity to limit Apple's ability to gain share in these markets given their high price points.

Another challenge for Apple, according to Schriber, is its Services segment, which represents 9% of sales. The analyst points out that "the remaining 91% of Apple's sales are in decline or seeing slower growth." Schriber notes that new offerings such as Apple Pay and Apple Music are not significantly impacting sales, as average annual sales per device decreased 10% y/y in FY10. She states, "Without clearer evidence that Apple can increase per device sales, and given its small size, we believe Services is unlikely to be a major growth driver."

The analyst maintains her Hold rating on the stock with a $105 target. She explains, "With valuation currently reflecting long-term growth challenges, balanced by expectations for a trade into the iPhone 7 launch, we view shares as fairly valued."

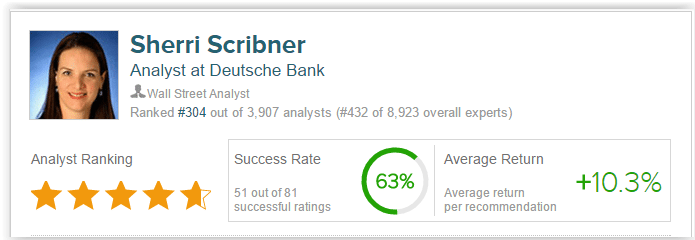

According to TipRanks, Sherri Scribner has a 63% success rate recommending stocks with an average return of 10.3% per recommendation.

Out of all the analysts who have rated Apple in the last 3 months, 92% gave a Buy rating while 8% remain on the sidelines. The average 12-month price target for the stock is $136.42, marking a 27% upside from where shares last closed.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.