By Shira Gonen

Brean Capital and UBS analysts shed light on tech giants Apple Inc. AAPL and HP IncHPQ, following the launch of the iPhone SE and meetings with management, respectively. While one analyst remains bullish on Apple, he lowers his price target due to excess inventory and uncertain volume estimates. The other remains on the sidelines for HPQ, believing that a weak PC and printer market weighs more heavily on the stock than long term opportunities. Let's take a closer look.

Apple Inc.

Analyst Ananda Baruah of Brean Capital commented on Apple following the iPhone SE launch, a more moderately priced version of the iPhone 6 with a smaller screen. The analyst begins by mentioning iPhone SE volume, believing that consensus estimates for revenue and GM, as well as unit volume for the June Q, are not completely accurate. Instead, the analyst believes that "it may not be until we enter August that AAPL estimates have appropriately digested its various nuances."

The analyst goes into deeper detail regarding unit estimates, believing the company will ship around 50 million iPhones for its March quarter, potentially reaching between 51-52 million depending on the final week, and between 46 and 48 million for the June quarter. As a result, Baruah is decreasing his GM and EPS estimates through 2017 to reflect the anticipated unit builds. He states, "We believe that builds for the Mar Q and Jun Q remain ‘softer' than shipments…"

The analyst continues by noting that while the company has excess iPhone inventory, about 18-20 million units for March and June Q compared to around 45 million builds, the company is working to decrease this number to around 10 million prior to September's iPhone 7 launch. Baruah explains, "We believe that excess iPhone inventory will be essentially extinguished exiting the June quarter." The analyst reiterates that he does not believe the company has had any supply chain improvements. Rather, he notes "stabilization" following lower than anticipated iPhone 6 demand in the October-January quarter.

Baruah highlights that last week, retailers reported 3.4 million pre orders for the iPhone SE in China, believing this figure is "net positive." He explains further, "We believe pre-order volume is at least as strong in the U.S than in China (so to say at least 6M-7M preorders world-wide)." As a result, the analyst believes the company is on track with the product. He states, "We believe that the early iPhone SE tea-leaves point to CY16 shipments aligned with the higher end of our original 20M – 25M CY16 view."

The analyst reiterates a Buy rating on the stock and lowers his price target to $150 from $170.

According to TipRanks, Ananda Baruah has a 51% success rate recommending stocks with an average loss of 0.6% per recommendation.

Out of the 38 analysts who have rated the company in the past 3 months, 33 gave a Buy rating, 1 gave a Sell rating, and 4 remain on the sidelines. The average 12-month price target for the stock is $133.18, marking a 20% upside from current levels.

HP Inc

UBS analyst Steven Milunovich explains his opinion on HP Inc, citing near term challenges and long term potential. The analyst explains that HPQ "has had a rough first two quarters" since it spun off from parent company HP. According to the analyst, its main challenges were printer and PC sales. Milunovich states that company EPS guidance for the current quarter of $1.59-1.69 "depends on an unusually strong second half." While "easier comparisons and actions to stabilize supplies" increase the likelihood, the analyst has a "cautious" EPS outlook for the quarter of $1.57.

The analyst echoes company views of it's the decline in its core PC and printer markets, predicting a 3-4% annual decrease. He notes that the company must turbocharge efforts in other sectors to compensate, such as Ink and managed print services. He states, "With printers providing 80% of company profit, the priority is stabilizing supplies revenue by the end of F17." The analyst is confident in management's ability to effectively handle this challenge.

While some investors prefer a focus on cash flow and shareholder return rather than growth, the analyst agrees with CEO Dion Weisler, who "does not just want to milk the installed bases." The analyst believes that a focus on coping and 3D printing is the best choice for the company at this point. He states, "While we have near-term reservations we are intrigued by HP's potential in copying and 3D printing." Specifically, Milonovich believes these two segments are "realistic adjacencies" with the Copying business potentially doubling the company's TAM. He also notes a shift in business model, moving from consumables to "hardware, services, and fusing agents."

The analyst maintains a neutral rating on the stock with an $11 price target.

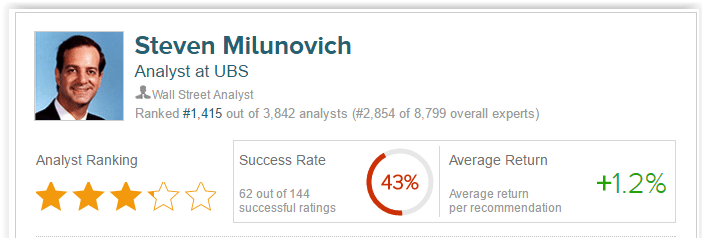

According to TipRanks, Steven Milunovich has a 43% success rate recommending stocks with an average return of 12% per recommendation.

Out of the 11 analysts who have rated HPQ in the past 3 months, 4 are bullish while 7 remain on the sidelines. The average 12-month price target for the stock is $13.18, marking a 9% upside from current levels.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.