By Jonathan Kalin

Oppenheimer analysts remain bullish on Yahoo! Inc. YHOO and don't lose taste for Chipotle Mexican Grill, Inc. CMG after the announcement of a 15% downsizing plan and an infectious decline in revenue across the restaurant chain, respectively.

Yahoo! Inc.

Jason Helfstein of Oppenheimer is bullish on Yahoo following its fourth-quarter results. Specifically, the analyst refereed to the the company's plans of 15% workforce reduction and facilities savings to reduce cash expenses to $2.4-2.6 billion. Yahoo is closing five international offices and plans to end 2016 with annualized cash expense run rate of $2.5 billion at 25% plus EBITDA margins, equating to a 2-3-year goal of $1B of EBITDA vs. $949M in 2015.

Helfstein continues, "Mobile, Video and Native accounted for 38% of traffic-driven revenue, up from 33% last year." He estimates that BrightRoll (est. $40M) was responsible for a majority 4Q growth. Moving forward, Helfstein explains Yahoo's plan to develop advertising products around "content verticals (News/Sports/Finance/Lifestyle) and invest in mobile search; a decision that some may question.

Helfstein concludes that Yahoo shares are undervalued when comparing the company to Alibaba and Yahoo! Japan. Moving forward, he believes the company "needs to restructure its costs to leverage ad technology and reduce headcount." Yahoo, according to Helfstein, could be a "strategic value to a large media or communications company." The analyst affirms an Outperform rating with a price target of $49.00.

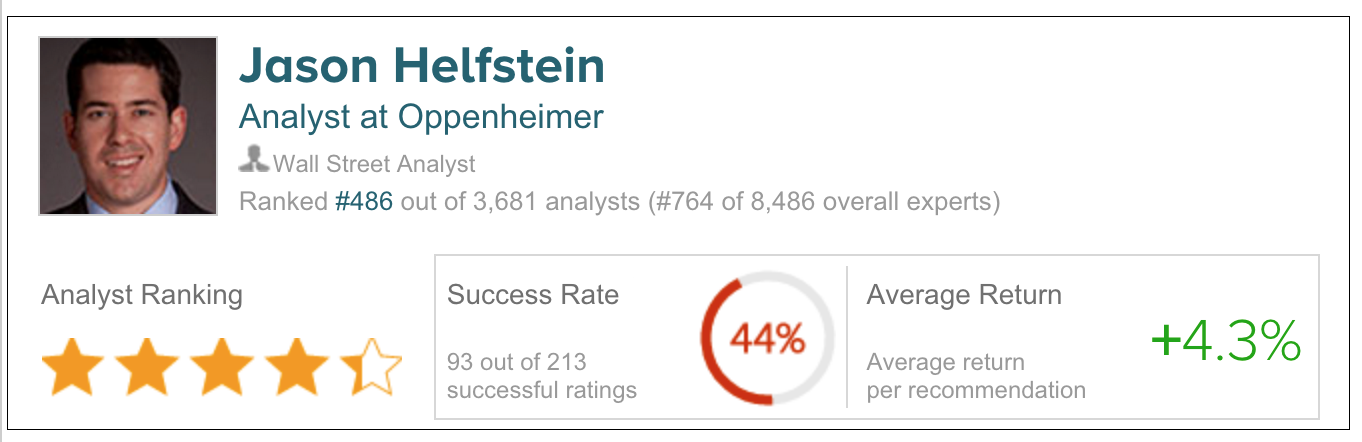

According to TipRanks.com, which measures analysts' and bloggers' success rate based on how their calls perform, analyst Jason Helfstein has a yearly average return of 4.3% and a 44% success rate. Helfstein is ranked #486 out of 3681 analysts.

Chipotle Mexican Grill

Oppenheimer analyst Brian Bittner maintains a Perform rating on Chipotle Mexican after the company reported quarterly results, posting EPS of $2.17, beating the Street's estimates of $1.84, despite an operational miss. Bittner says that the lower than expected tax rate helped boost EPS by $0.12, in addition to a "G&A well below consensus ($46.9M vs. $71.3M) owing to lower stock comp," boosting EPS by an additional $0.50.

Following Chipotle's earnings, Bittner is slashing EPS estimates as "sales trends remain well below expectations and cost ups are more intense than previously modeled. Bittner is lowering 16E/17 EPS to $6.80/$11.59 from $13.20/$16.75, due to lower comps and margins. Bittner continues, "A potential loss in 1Q could occur as '16 promotional/marketing investments are front-end loaded against a potentially down 20%-30%-ish comp." Restaurant margins were 19.6% compared to the Street's estimates of 20.4%. Bittner believes if Chipotle can gain back all the lost sales, margins can climb back to ~25% over time.

Bittner concludes that it is best to "continue to sit on the sidelines until visibility into sales/profit recovery improves."

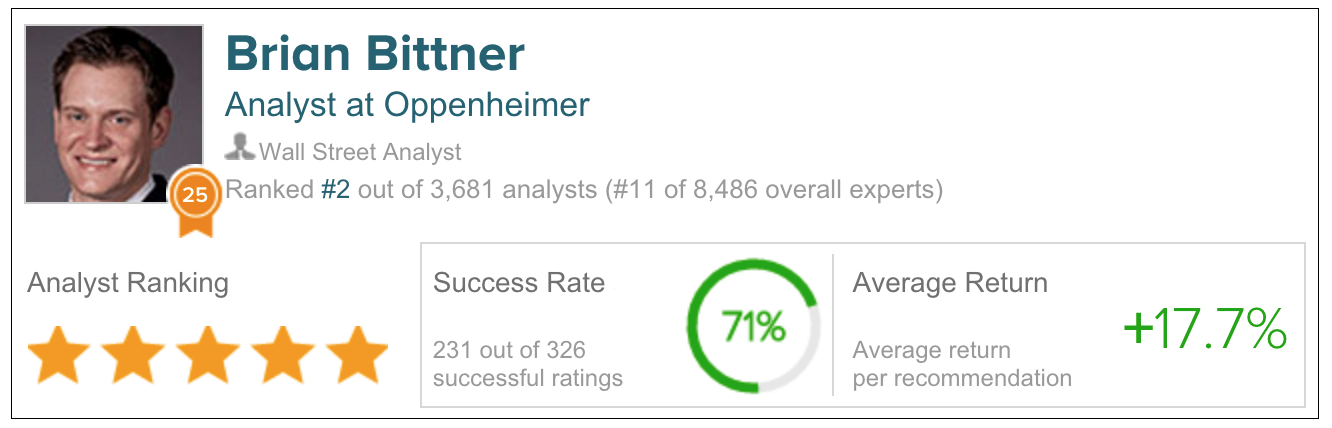

According to TipRanks.com, which measures analysts' and bloggers' success rate based on how their calls perform, analyst Brian Bittner has a yearly average return of 17.7% and a 71% success rate. Bittner is ranked #2 out of 3681 analysts.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.