By Shira Gonen

Roth analysts weighed in yesterday on Canadian Solar Inc. CSIQ and Yelp Inc YELP post a stock price drop and pre-earnings, respectively. While one analyst remains bullish on Canadian Solar, citing upside catalysts for the stock despite the recent drop, the other remains bearish on Yelp due to increasing competition from major players.

Canadian Solar Inc.

Analyst Philip Shen of Roth Capital recently weighed in on CSIQ, selecting the company as one of his "top picks." First, the analyst notes the stock is trading below is pre-ITC extension levels, which he views as "an attractive buying opportunity." The analyst attributes the falling stock price to its grouping "with other China-based stocks and overall macro concerns." However, he states that CSIQ is "one of the best-positioned solar companies in [his] universe" due to its leading global position, strong downstream pipeline, and "limited exposure to China."

The analyst is also bullish regarding the company's access to debt financing, as the company was able to fund various project in the U.S. and abroad through loans. He believes that success in U.S. utility projects, "potentially improved economics in the company's existing U.S. pipeline as a result of the ITC extension," and "a successful yieldco launch" are all upside catalysts for the stock.

On February 1, 2016, the analyst reiterated a Buy rating on CSIQ with a $40 price target. Philip Shen has a 30% success rate recommending stocks with an average loss of 14.1% per recommendation on TipRanks.

According to TipRanks' statistics, all 5 analysts who rated the stock in the past 3 months gave a bullish rating. The average 12-month price target for the stock is $32.70, marking a 60% upside from where shares last closed.

Yelp Inc

Analyst Darren Aftahi of Roth Capital recently expressed bearish sentiment on Yelp prior to its Q4:2015 earnings, set to release on February 8, 2015. While the analyst expects revenue to be in in-line with Street expectations, he will "continue to focus on decelerating mobile user growth and local ad sales," which he believes are "the best measures of the health of the businesses." The analyst predicts growth in these two metrics to fall at around 33%/26% y/y, respectively, compared to last year's estimates of 60%/37%. He also "remains cautious" regarding the company's user levels, as Quantcast, a digital marketing company, reported a decline in users y/y and in the fourth quarter.

Aftahi predicts below consensus FY'16 sales and EBITA estimates for the company, as a result of lower sales and increased marketing and sales costs as the company tries "to combat an increasingly competitive playing field." He notes that major competitor Facebook "is targeting YELP's market, local small business advertising, in a big way," realizing a "big opportuning in monetizing these Business Page users." He states that Facebook has a higher visitor rate than Yelp, and believes YELP provides less of an incentive to use their site "as both Facebook and Google continue to roll out an identical product to a worldwide audience, and show no signs of slowing down."

He comments on the company's Eat24 food delivery service, which is competing with "new, deep-pocketed entrants" such as Amazon Prime, Uber, and "established players" GrubHub and Postmates. The analyst is cautious on this segment as Eat24 represents between 8% and 9% of Yelp's total sales.

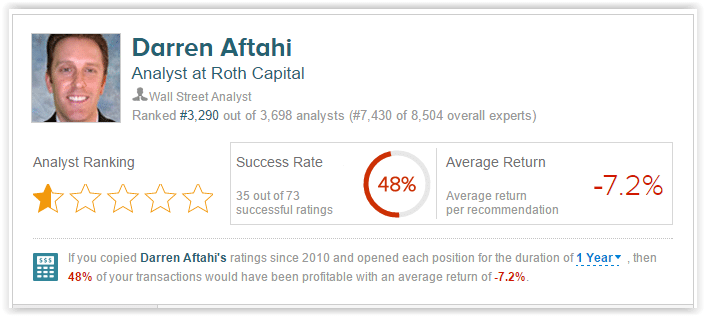

On February 1, 2016, the analyst reiterated his Sell rating for the company and lowered his price target to $15 from $17.50 as a result of potentially slowing key metrics, rising competition, and increasing expenses. Darren Aftahi has a 48% success rate recommending stocks with an average loss of 7.2% per recommendation on TipRanks.

According to TipRanks' statistics, out of the 8 analysts who have rated YELP in the past 3 months, 4 gave a Buy rating, 2 gave a Sell rating, and 4 remain on the sidelines. The average 12-month price target for the stock is $30.20, marking a 43% upside from where shares last closed.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.