Loading...

Loading...

On August 12, Cowen & Company analyst James Sullivan published a research note, "Differentiated Strategy Justifies Premium Multiple," initiating industrial REIT Terreno Realty Corp.

TRNO at Outperform.

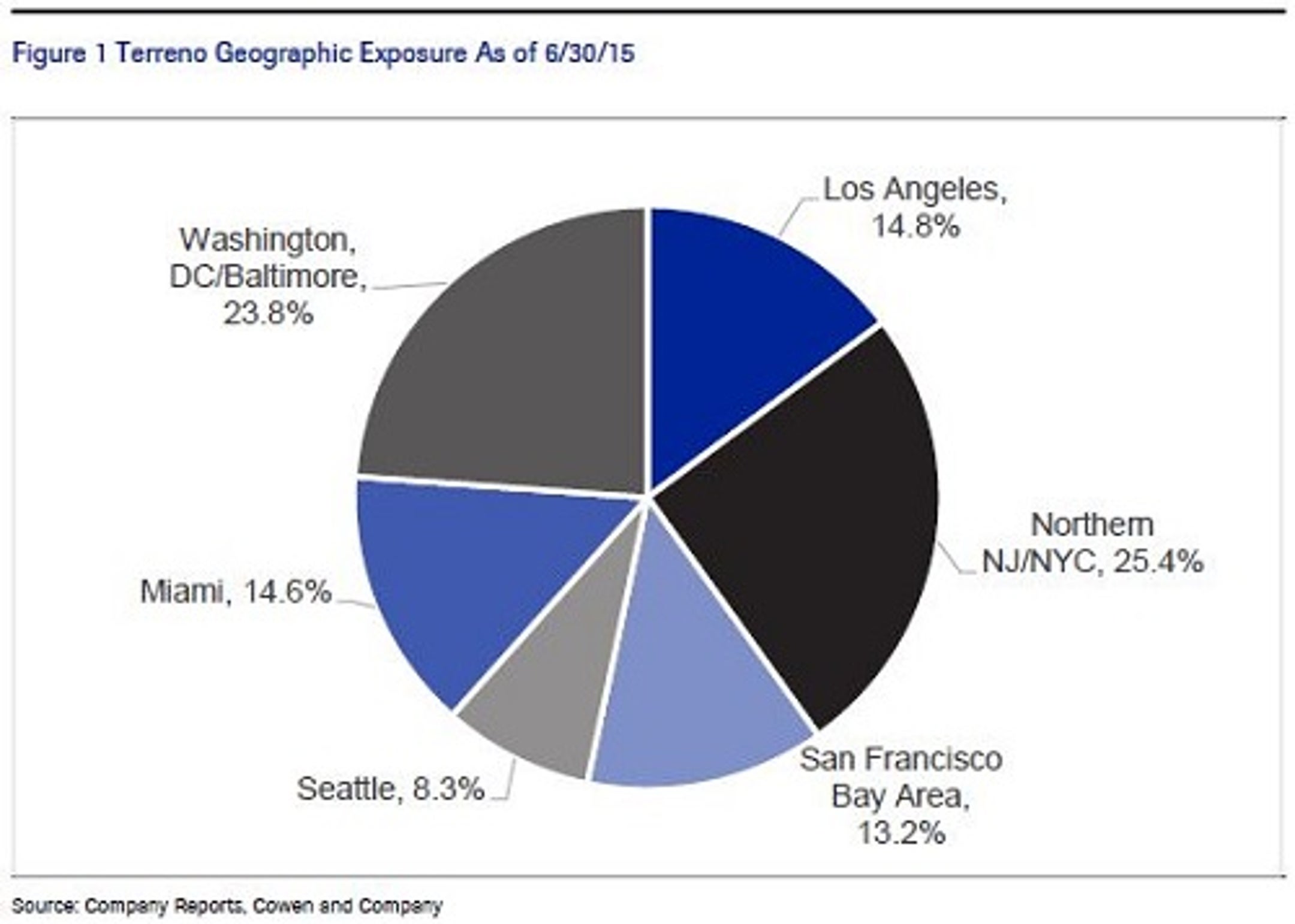

Terreno follows a unique strategy of targeting multi-tenant, infill, industrial properties located in six high-barrier to entry U.S. coastal/port markets.

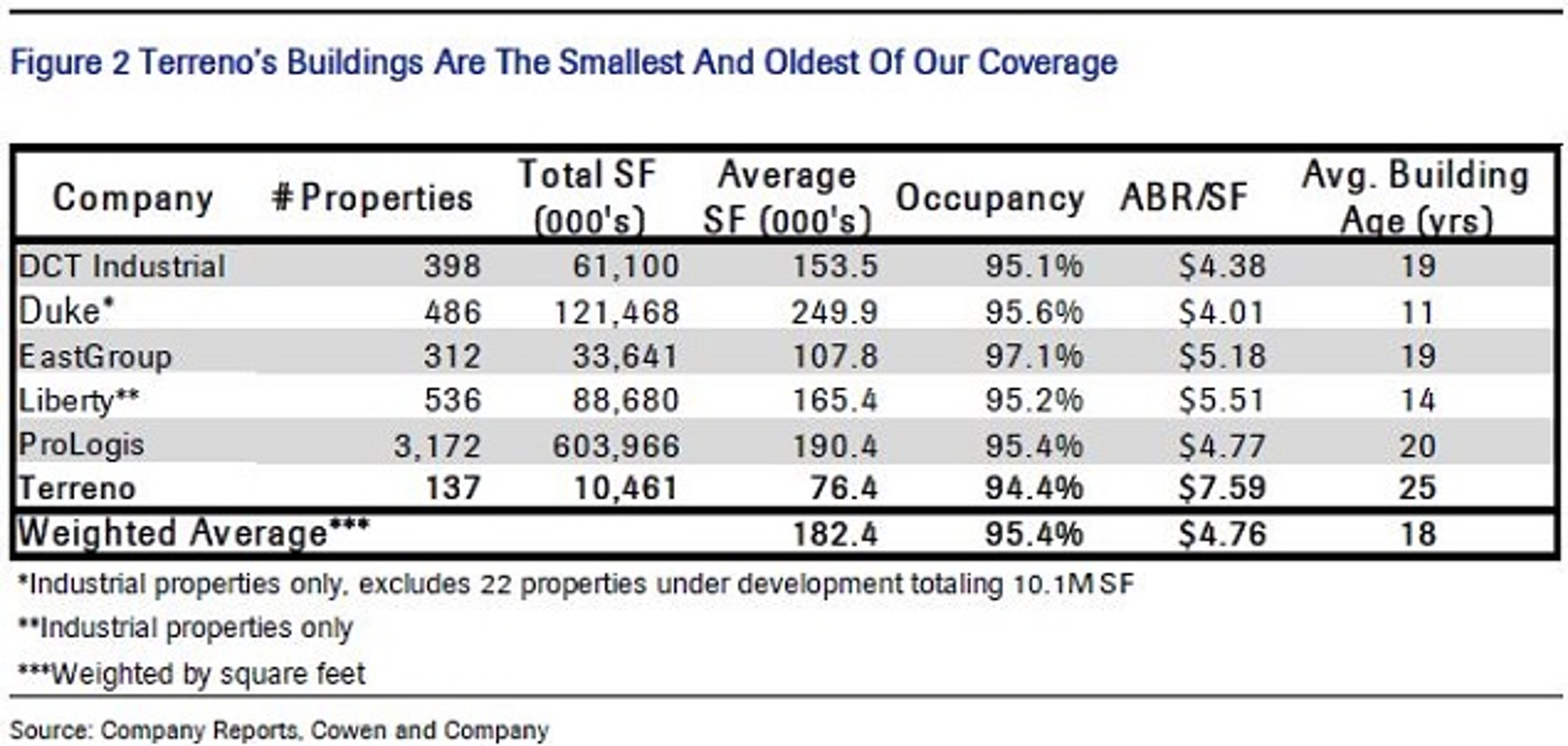

However, the TRNO strategy is further refined by concentrating on acquiring smaller "value-add" industrial properties, averaging just $7 million and ~76,000 square feet.

Rexford Industrial Realty

REXR follows a similar strategy, but is entirely focused on "sharpshooting" SoCal markets: LA/Long Beach, Orange County, Ventura County, The Inland Empire and San Diego. Rexford sports a $770 million market cap, pays a 3.5 percent yield, and REXR shares are down 11.4 percent YTD.

• http://www.benzinga.com/analyst-ratings/analyst-color/15/07/5685699/is-it-really-time-to-sell-stag-industrial-reit

Notably, Rexford has a slightly older and a bit smaller average building size than Terreno, and is currently not under coverage by Cowen.

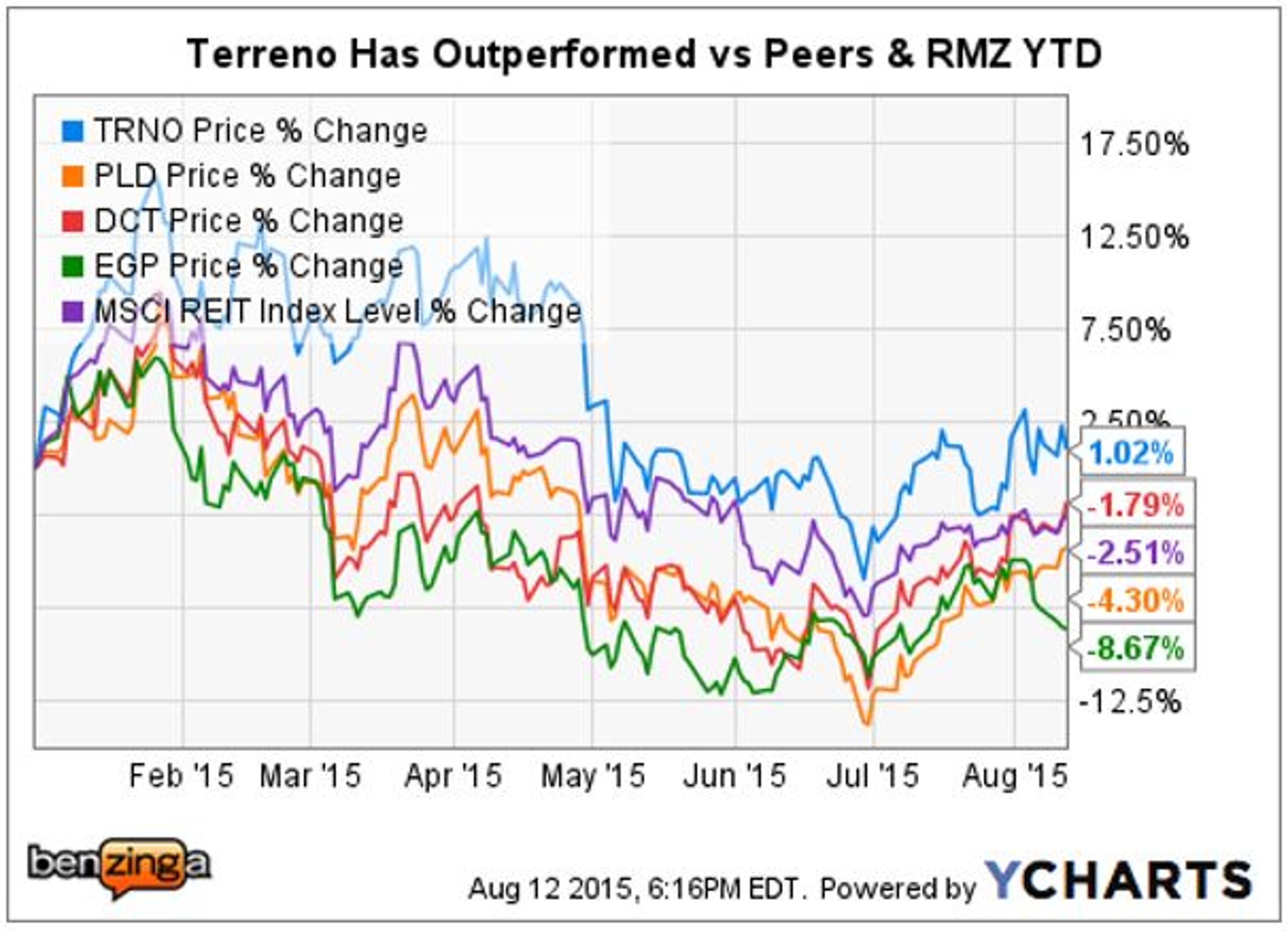

Tale Of The Tape - 2015 YTD

Terreno has a $900 million cap and pays a dividend yield of approximately 3.1 percent.

The MSCI REIT Index (RMZ) is a good proxy for broader REIT sector performance. Terreno has held up better than its industrial peers covered by Cowan.

DCT Industrial Trust

is focused on large single-tenant development and build-to suits in 20 major U.S. markets. DCT has a market cap of $3.1 billion and yields 3.2 percent.

Notably, on August 12, Cowan & Co. analyst Tom Catherwood initiated DCT Industrial at Market Perform with a $37 target price; which represents a potential 7 percent upside from the previous close of $34.59 per share.

Prologis, Inc.

PLD is a global logistics powerhouse with considerable land holdings for future development. PLD dwarfs its peers, sporting a $21.6 billion cap, with a dividend currently yielding 3.9 percent. Cowan currently has an Outperform rating on Prologis.

• http://www.benzinga.com/news/earnings/15/07/5691313/why-logistics-giant-prologis-incs-q2-results-matter

The Terreno management team has a Prologis pedigree, with Chairman and CEO Blake Baird, President Michael Coke, CFO Jamie Cannon and EVP John Meyer all having worked at AMB Property Corp., predecessor to Prologis.

EastGroup Properties

Loading...

Loading...

has a predominantly Sunbelt portfolio of smaller sized multi-tenant and flex-industrial properties, including a large Houston exposure. EGP has a market cap of $1.9 billion, with a well-covered dividend yielding 3.95 percent.

Cowan - Terreno Realty: Initiated Outperform, $24 PT

The TRNO $24 target price represents a potential ~13.75 percent upside, based on its prior close of $21.10; and a 12 month total return of 16.75 percent including the dividend.

Cowen introduced 2015 and 2016 FFO/share estimates for Terreno of $0.93 and $1.13, respectively. The Cowen $24 PT represents 21.2x 2016E FFO per share.

Sullivan noted that since 2012 Terreno has had the highest same-store NOI growth (ssNOI), compared with its industrial peers, averaging 12 percent.

Terreno does not develop and has no land-bank, which is another major differentiator. Therefore, ssNOI growth is an even more critical component of FFO growth for Terreno.

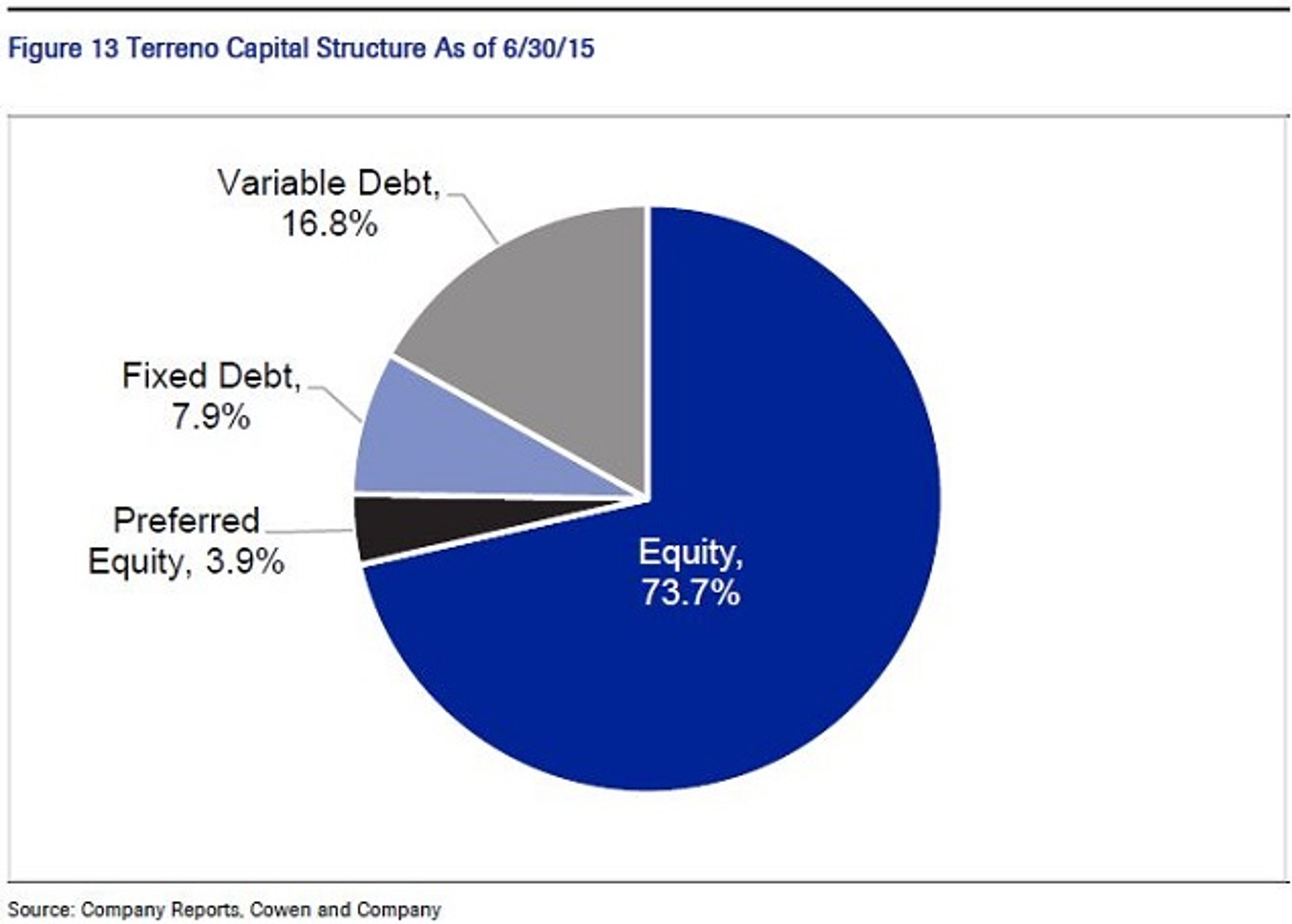

Terreno Strong Balance Sheet

"Terreno's debt to capital ratio is 23.5%, the lowest of our industrial REIT coverage," according to Sullivan. Additionally, on August 5, Terreno announced a repurchase program for up to 2.0 million shares of stock through December 31, 2016.

Terreno does not have any meaningful debt maturities until 2019, and recently received an investment grade rating of BBB- from Fitch.

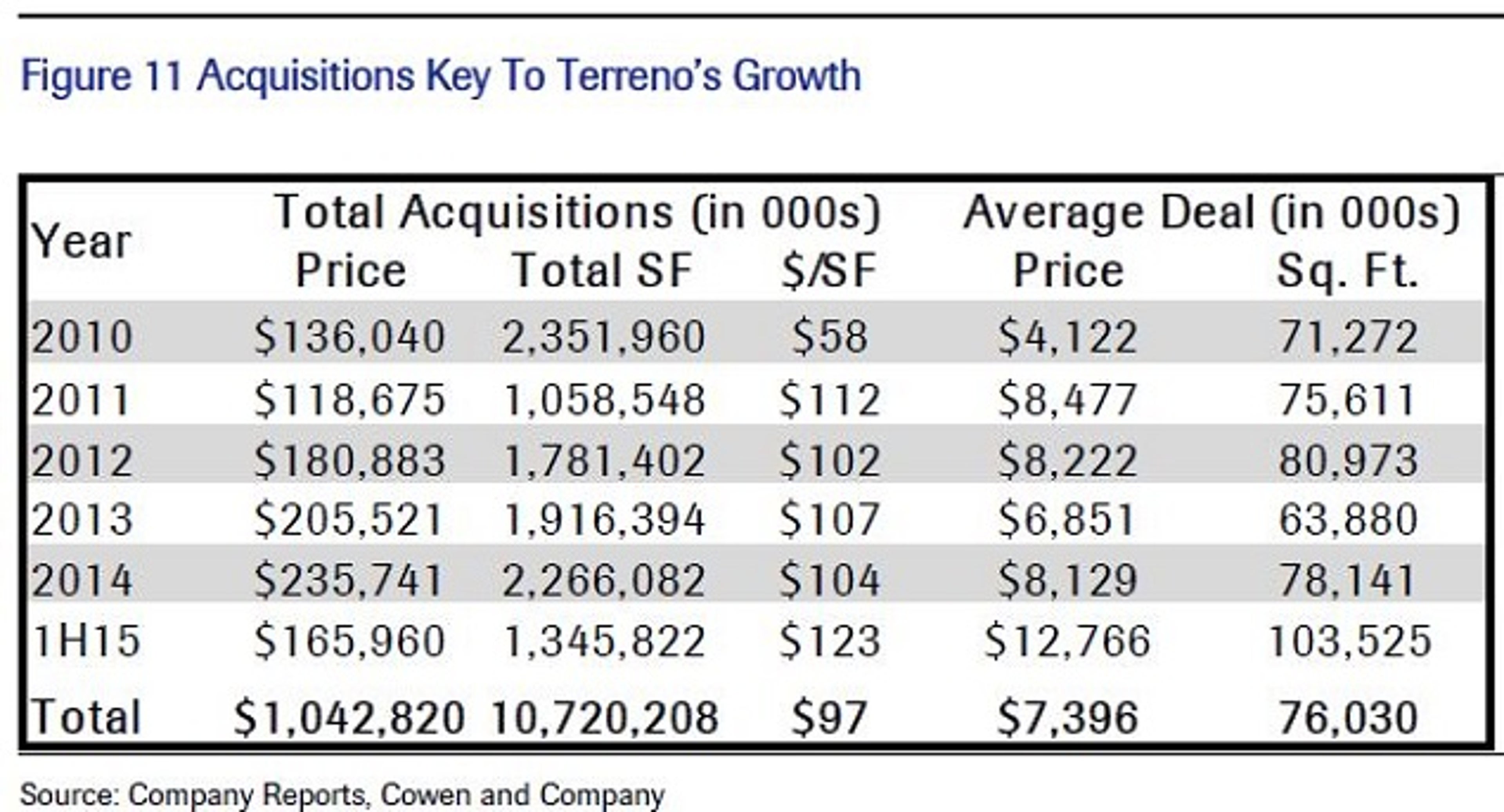

Terreno Acquisition Strategy

Since its IPO in 2010, Terreno has acquired 10.7 million SF of industrial properties at a total cost of $1.0 billion, according to the report.

Cowen estimates that Terreno will acquire $266 million in FY 2015, and $300 million in FY 2016 vs relatively few dispositions.

Older Infill Properties - Glass Half Full?

High barriers to entry in Terreno's core coastal markets contribute to the age of its portfolio. However, this also suggests there could be redevelopment potential imbedded in the TRNO portfolio due to the lack of available new development sites.

These smaller, highly desirable, infill locations generate an average base rent (ABR) of $7.59/SF, the highest ABR of the peer group, by a wide margin.

Cowen believes that the "last mile" for ecommerce delivery, could also be a demand catalyst, helping ssNOI growth moving forward.

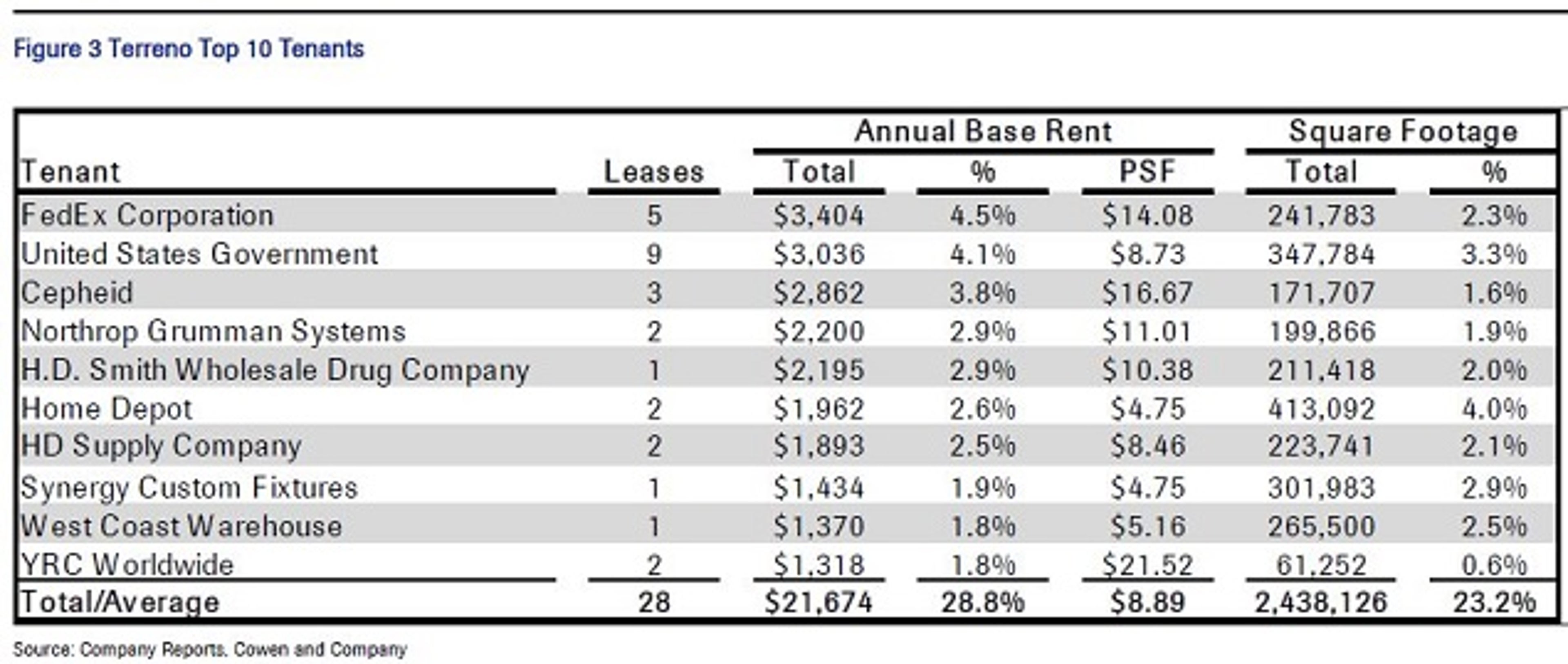

Tenant Concentration

The Top 10 tenants for Terreno comprise 28.8 percent of ABR, the highest concentration of the Cowan peer group, which averages 12.3 percent.

Notably, FedEx at 4.5 percent of ABR is already the top tenant for Terreno.

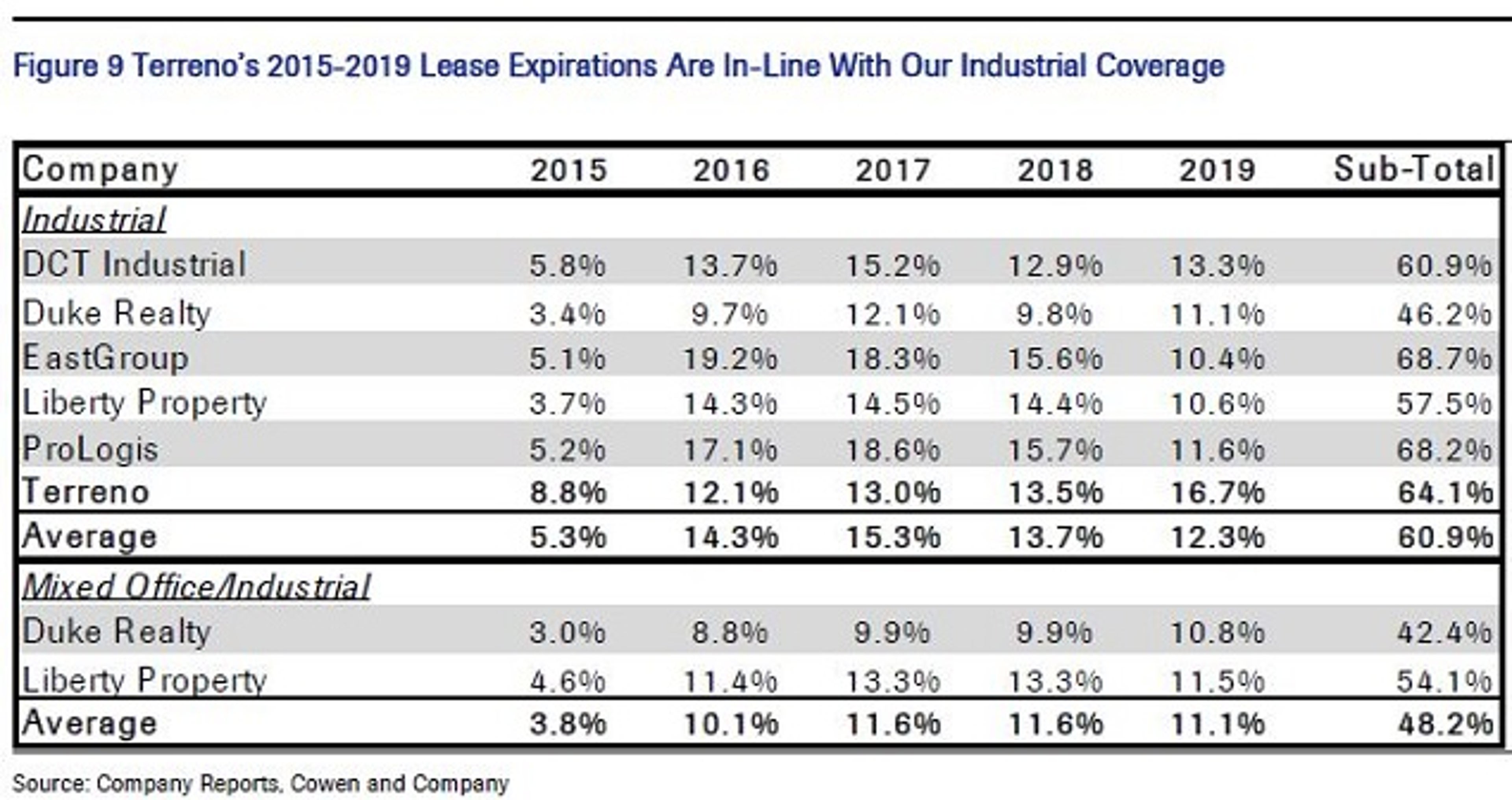

Terreno Lease Expirations vs Peers

Terreno's lease expirations for the next five years are in-line with its peer group.

Cowan expect leasing spreads of 15.0 percent for Terreno in 2015, and 10.0 percent in 2016.

Investor Takeaway

Terreno shares have outperformed Cowen's peer group YTD, for the past 12 months and for the last three years, as well.

Cowen believes,"…Terreno's execution of its value-add investment strategy contributed to higher SSNOI growth and relative outperformance."

Loading...

Loading...

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Posted In: Analyst ColorLong IdeasREITDividendsPrice TargetInitiationAnalyst RatingsTrading IdeasGeneralReal EstateCowen & CompanyecommerceJames SullivanTom CatherwoodWarehouse/Industrial

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in