As the U.S. stock market trades near record highs, Credit Suisse has boosted its year end price target for the S&P 500 as the bank sees overdone pessimism on tapering fears and better earnings revisions. The bank also posted a price target for the end of 2014 that implies about a 15 percent gain through the end of 2014 for U.S. stocks.

Another 15 Percent Upside

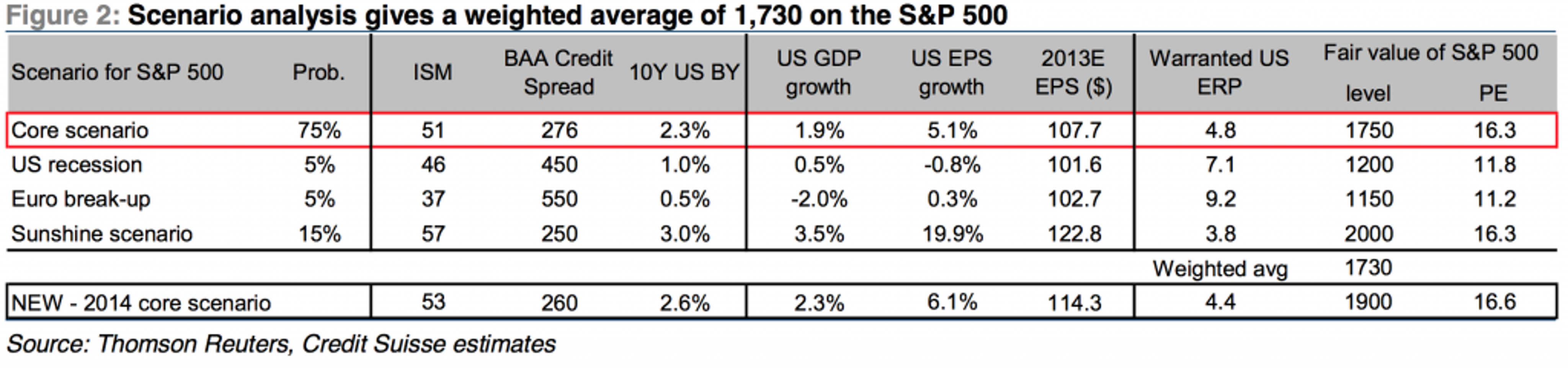

The analyst team, led by legendary strategist Andrew Garthwaite, boosted its 2013 year-end price target for the S&P 500 from 1,640 to 1,730. The move would imply an additional 6 percent upside from Tuesday's close and represent an 11.23 percent return for the year for the index.

The analyst team also published a new price target for year-end 2014. The bank now expects the S&P 500 to rise to 1,900 by the end of 2014, which would equate to a 16.5 percent rise by the end of 2014 and a 9.8 percent return for 2014 alone.

Scenarios

The bank identified five key reasons for boosting its price target. Notably, the bank sees the market rising even as the economy struggles to find solid footing and continues to grow at a very modest pace.

Using its models to derive an equity risk premium to extrapolate a price target, the bank highlights that the risk of a U.S. recession has diminished in recent months. The core scenario also assumes a European recession for most of this year and still yields a price target of 1,750.

However, the 1,730 price target is a weighted-average of the price targets that emerge from different scenarios. The bank gives a 5 percent probability to a U.S. recession now (from 10 percent previously), in which case they see the S&P 500 at 1,200, and a 5 percent probability of a Eurozone breakup when they expect the index to fall to 1,150. They also highlight that should the U.S. economy take off into the "sunshine scenario," the index could rise as high as 2,000 by year end.

As the above chart shows, they expect the economy the S&P 500 to rise to these levels even as the economy barely grows. In the core scenario, in which they anticipate a price target of 1,740, they only see the ISM Composite PMI averaging 51, barely showing expansion or about 2-2.5 percent GDP growth for the year.

Attractive Relative Valuations

Quantitative Easing and other central bank tools have resulted in abnormally low real bond yields and have made all other asset classes, including equities, look expensive on an absolute basis, the bank writes. However, on a relative basis, the story changes.

The equity risk premium (ERP for short) is a measure of the the additional return over the risk-free rate required to make the NPV of future dividends equate to the current market value. Currently, the bank estimates that the ERP is 6.1 percent based on their forecasts and 7.4 percent based on consensus data (as Credit Suisse's earnings estimates for the S&P 500 are below those of the street).

So where should the ERP be? "We estimate the warranted ERP as a function of the cycle and risk appetite, proxied by lead indicators and credit spreads respectively. The stronger macro momentum and the lower the level of spreads, the lower the warranted ERP. Currently the warranted ERP is 4.8%, according to our model."

"In sum, we think the ERP could easily fall from 6% to 5%. Even assuming that bond yields rise by 50bps (as forecast by our fixed-income strategists by year-end), this would suggest 9% capital gain for equities (giving a total return of c12%) over the next year."

Global Economy Bottoming

The bank also sees a trough in global economic momentum occurring as we head into the summer months. "Global macro momentum has slowed sharply between March and early May, just as it did at the beginning of 2010, 2011 and 2012. In those cases, the slowdown in macro momentum turned out to be quite sharp, leading to significant corrections in the equity market."

"We believe that the slowdown this year is likely to be far milder than has been the case over the past three years. In fact, we can already see the first signs that the deterioration in global macro momentum has come to a halt." The bank notes that its 10-factor U.S. GDP model saw in up-tick in May to a 2.3 percent annualized rate from 1.9 percent in April and that its global-GDP weighted macro surprise index has stabilized near the bottom of the previous three-year's range.

The Old Normal?

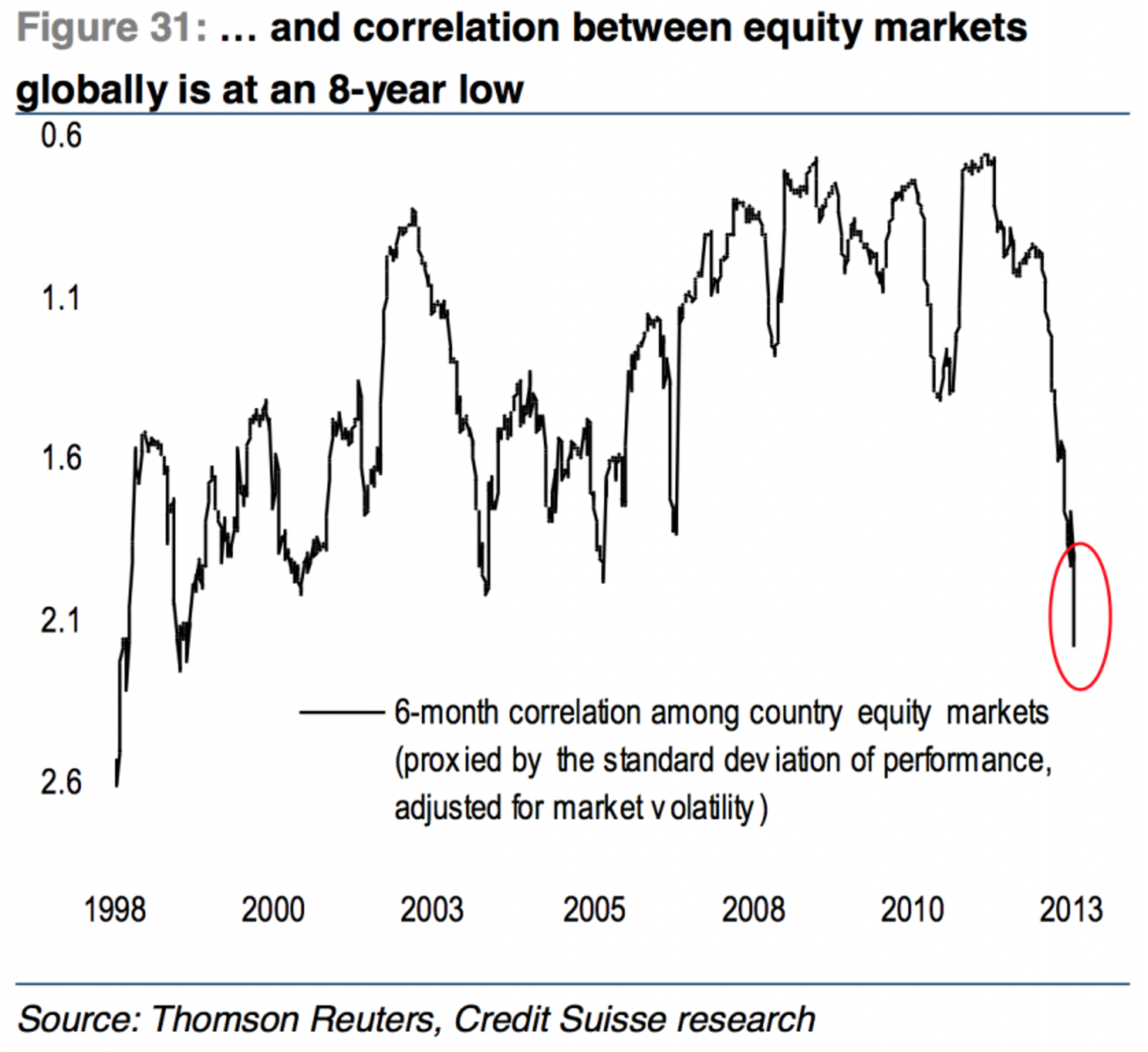

The bank also pointed out a sharp change in markets that has occurred over the previous few months. Investors have become accustomed to high correlations amongst asset classes post-crisis, however the bank sees this phenomenon abating as the world economy normalizes. They note the breakdown in the weak dollar/strong stock correlation as a sign that markets are returning to pre-crisis ways. "This, we believe, points to the underlying strength of the US economy – as well as the cheapness of the dollar."

Tapering Pessimism Overdone

Tapering fears are overdone in their opinion and the bank sees the excess liquidity that the global central banks have pumped into financial markets going nowhere anytime soon. They note that based on historical comparisons, the current level of excess liquidity points to approximately 20 percent upside for global equities over the next 12 months.

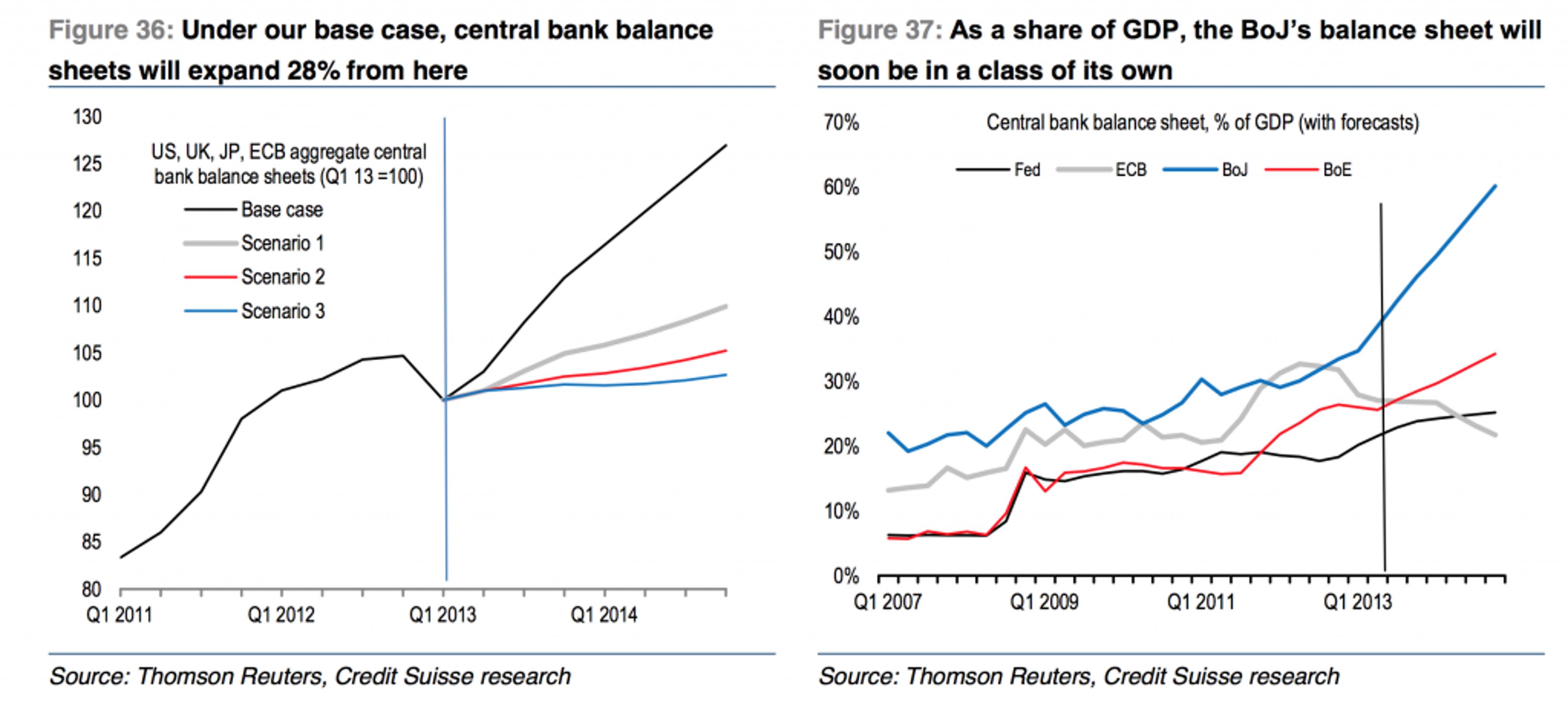

The analysts also expect central bank balance sheets to continue to expand with the Bank of Japan soon to enter a league of its own. "Concerns about the Fed tapering its asset purchases are arguably clouding the bigger picture that globally the major developed market central banks are set to continue expanding their balance sheets, in aggregate, well into 2014. On our base case assumption (from our economists), central bank balance sheets will expand by 27% at current exchange rates between the end of Q1 this year and the end of 2014."

"We think that market expectations of QE ending in Q1 2014 are too pessimistic. Our economists are currently forecasting a reduction in the Fed's asset purchase volume to $65bn a month (from $85bn a month) starting in September – and for QE to end at some point in the second half of 2014. In the case of QE 1 and QE 2, markets did not peak until six to seven weeks after the end of QE. On our economists' current forecasts, this would imply a monetary-policy-related correction in the second half of 2014."

Earnings

"We upgrade our 2013 US EPS forecast from $104.9 to $107.7 (implying EPS growth of 5.1%, up from 1.9%). This is still 2% below the IBES consensus forecast of $109.7 (consensus growth is 7.1%). The gap between our own estimate and IBES consensus has fallen partly because IBES consensus for end 2013 has fallen by 7% since mid-2012." The estimates only assume 1.9 percent GDP growth in the U.S. for 2013, 1.5 percent inflation, and for the dollar to appreciate an additional 5 percent.

"While the rate of global earnings revisions remain flat, US earnings revisions have recently turned positive for the first time since May 2012. We note that the market typically has risen by 4% (and has risen 80% of the time) over the six month following earnings revisions turning positive in the US."

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.